Analysis

Loan-Level Stress Testing: A Strategic Imperative for Modern Credit Risk Management

As credit markets become increasingly complex, we examine how loan-level stress testing provides the insight needed to anticipate losses, validate assumptions, and strengthen portfolio resilience.

In today’s volatile financial landscape, the ability to anticipate and navigate potential economic downturns is not just a strategic advantage it’s a necessity for financial institutions. As credit portfolios become increasingly complex and economic uncertainty persists, stakeholders must prioritize the implementation of sophisticated stress testing frameworks that deliver accurate, actionable insights into portfolio vulnerabilities and capital adequacy.

By adopting a loan-level stress testing approach that integrates directly with CECL-based frameworks, institutions can gain invaluable insights into their credit portfolios, enabling them to identify vulnerabilities, optimize capital allocations, and enhance strategic decision-making.

The Case for Loan-Level Precision

Traditional portfolio-level stress testing approaches often rely on broad approximations and static assumptions that fail to capture the nuanced dynamics of credit risk migration. These methods treat portfolios as homogeneous blocks, applying uniform stress factors across diverse loan types, borrower profiles, and risk characteristics. Such approaches may provide directional guidance but lack the granularity necessary for precise capital planning and robust risk management.

A loan-level stress testing framework addresses these limitations by applying stress directly to individual borrower financial indicators, such as debt service coverage ratios (DSCR), net operating income (NOI), revenue trends, FICO scores, and small business risk indicator (SBRI) scores. This granular approach recognizes that borrower behavior and credit portfolio performance demonstrate heightened sensitivity to hypothetical economic scenarios that are unique to each institution.

By stressing these loan-level variables and predicting subsequent credit rating movements, institutions can forecast the resulting impacts on CECL allowances, provisions, net charge-offs (NCOs), and capital with remarkable accuracy.

Integration with CECL: A Natural Synergy

One of the most compelling advantages of a sophisticated loan-level stress testing framework is its seamless integration with existing CECL infrastructure. While CECL estimates reflect expected losses under baseline or reasonably supportable forecasts, stress testing extends this analysis to more adverse economic scenarios. The integration of both frameworks enables a comprehensive assessment of portfolio risk and capital adequacy.

By feeding predicted loan-level risk rating changes directly into an institution’s CECL exposure at default (EAD) model, the framework produces accurate impacts on allowances, earnings and capital. This approach leverages the actual CECL-based cash flow model with its detailed payment and risk characteristics—including contractual amortization terms, funded and unfunded amounts, default probabilities, loss given default assumptions, and prepayment rate curves—to deliver period-by-period forecasts over the specified horizon.

This methodology represents a substantial improvement over approximations, particularly because the progression of credit losses is path-dependent and rarely follows a linear pattern. The framework captures the dynamic interplay between portfolio runoff, new loan originations, risk rating migrations, and loss realization timing—factors that static models cannot adequately address.

Machine Learning for Predictive Power

The technical foundation of modern loan-level stress testing frameworks combines quantitative rigor with qualitative judgment through advanced machine learning techniques. Predictive models, including Decision Tree, Histogram Gradient Boosting, and Random Forest Classifiers, are trained on historical credit data to identify patterns in rating migrations under various stress conditions.

A key methodological innovation involves developing separate upgrade and downgrade models for each portfolio segment to address class imbalance issues where downgrades historically outnumber upgrades. These models utilize sophisticated performance metrics like F1 scores rather than simple accuracy, employ class weights to balance predictions, and incorporate ordinal classifiers with monotonic features to ensure logical stress responses.

This approach ensures that as borrower financial metrics deteriorate under stress, predicted rating downgrades increase proportionally—a critical validation step that enhances model credibility and regulatory acceptance.

The framework typically segments portfolios based on loan characteristics and data availability, for instance, large commercial real estate loans may be modeled using detailed financial statement variables, while consumer loans rely more heavily on credit scores and payment behavior. This segmentation enables each model to leverage the most predictive variables for its respective borrower population.

Comprehensive Multi-Period Forecasting

Perhaps the most significant value proposition of a loan-level stress testing framework is its ability to produce comprehensive multi-period projections rather than single-period snapshots. By incorporating roll-forward functionality with realistic loan growth assumptions, the framework dynamically updates the portfolio composition at each period throughout the forecast horizon, typically on a quarterly basis over one or more years.

This capability enables institutions to assess not only the initial shock from adverse conditions but also the cumulative impacts as stress persists and portfolio composition evolves. The framework produces forecasts of expected losses, provisions, NCOs, and capital ratios across the planning horizon, supporting both risk management and internal strategic planning initiatives. Institutions can evaluate their degree of compliance with relevant capital ratio thresholds—such as minimum Common Equity Tier 1, Tier 1, and Total risk-based ratios—while weighing the likelihood of various scenarios.

Technology-Enabled Solutions

These frameworks are most effective when supported by fully integrated technology platforms that unify CECL compliance, multi-scenario stress testing, and portfolio analytics within a single auditable infrastructure. Alter Domus’ ALLL+ Platform delivers CECL compliance and credit loss estimation with integrated scenario management, real-time attribution analysis, and governance capabilities ensuring full audit traceability, while the Analytics Platform (formerly Risk Modeler) extends this into strategic portfolio management through macroeconomic default regression, loan-level risk classification, and real-time portfolio monitoring.

When these capabilities share a common data infrastructure, institutions gain a materially clearer view of embedded portfolio risk. Advanced machine learning further enhances this visibility by surfacing complex patterns that traditional approaches overlook, translating analytical rigor into more informed decisions around capital allocation, underwriting, and strategic planning.

A Foundation for Prudent Risk Management

The risks associated with credit portfolios are multifaceted and can vary significantly across institutions, influenced by factors such as borrower behavior, market conditions, and organizational objectives. Credit portfolio compositions differ across financial institutions based on strategic objectives, risk appetite, expertise, geographic presence, and organizational mission. Consequently, both borrower behavior and portfolio performance may demonstrate unique sensitivities to economic scenarios, making tailored stress testing essential, a necessity further reinforced by OCC guidance.

Regular and rigorous stress testing through a sophisticated loan-level framework serves as a cornerstone of sound risk management. It helps institutions identify vulnerabilities within portfolios—particularly those arising from excessive concentrations in specific borrowers, industries, geographic regions, or product types. This proactive approach not only safeguards against potential losses but also positions institutions to make informed strategic decisions regarding underwriting standards, credit policy refinements, and capital allocation optimization.

In an uncertain economic environment, institutions that embrace advanced loan-level stress testing frameworks will be better positioned to navigate challenges and thrive.

To learn more about AlterDomus’ integrated risk management solutions, contact [email protected].

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

Navigating Credit Vulnerabilities in the U.S. Auto Loan Sector

We explore how financial institutions can move beyond backward-looking risk management by adopting forward-looking CECL frameworks, multi scenario stress testing, and portfolio analytics to proactively identify emerging credit risks.

The U.S. auto loan market has undergone structural shifts that are reshaping credit risk. Post-COVID vehicle price increases have driven loan balances significantly higher, while extended terms—increasingly exceeding 72 months—mask affordability challenges. Simultaneously, widespread negative equity from trade-ins has pushed loan-to-value ratios above 100% at origination, with monthly payments frequently surpassing $1,000.

These compounding dynamics intensify credit risk in recent loan vintages, requiring financial institutions to move beyond backward-looking risk management toward forward-looking analytical frameworks consistent with CECL assumptions that identify vulnerabilities before losses materialize. Alter Domus’ integrated platform combines CECL compliance, multi-scenario stress testing, and real-time portfolio analytics to enable institutions to proactively identify and monitor loans exhibiting multiple risk characteristics.

Quantifying the Risk: Key Market Vulnerabilities

The auto loan market has evolved during the post-COVID period in ways that compound several key credit risk factors, leaving lender’s portfolios vulnerable to potential economic downturns.

- New vehicle prices have increased more than 30% since 2019, reaching an average of almost $49,000 in 2025.

- Average loan repayment terms have lengthened, with a growing percentage exceeding 72 months or more to cope with payment shock.

- Monthly loan payment amounts have increased, averaging $773, while payments exceeding $1,000 have reached an all-time high of 20.3% of the market.

- Around 30% of trade-ins now carry negative equity, averaging $7,214, a byproduct of slower equity buildup due to extended loan terms.

- This has led to LTV ratios often exceeding 100% at origination, leaving borrowers vulnerable to declining used vehicle values or deteriorating personal finances.

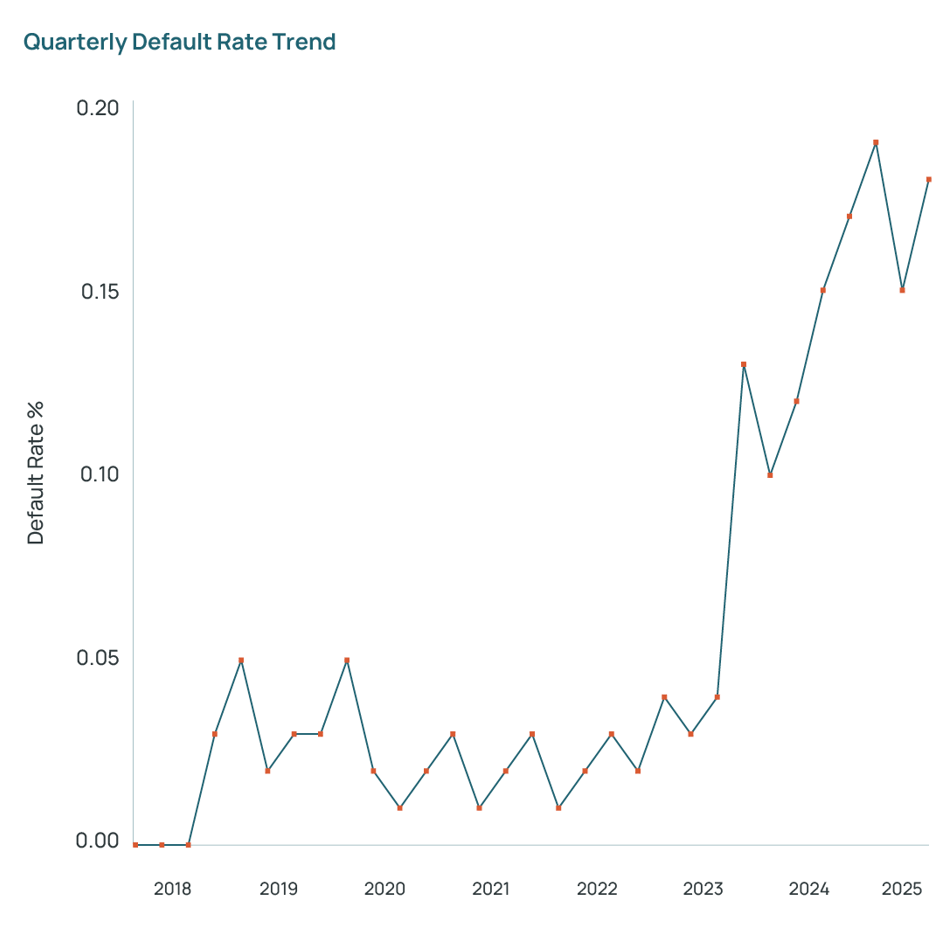

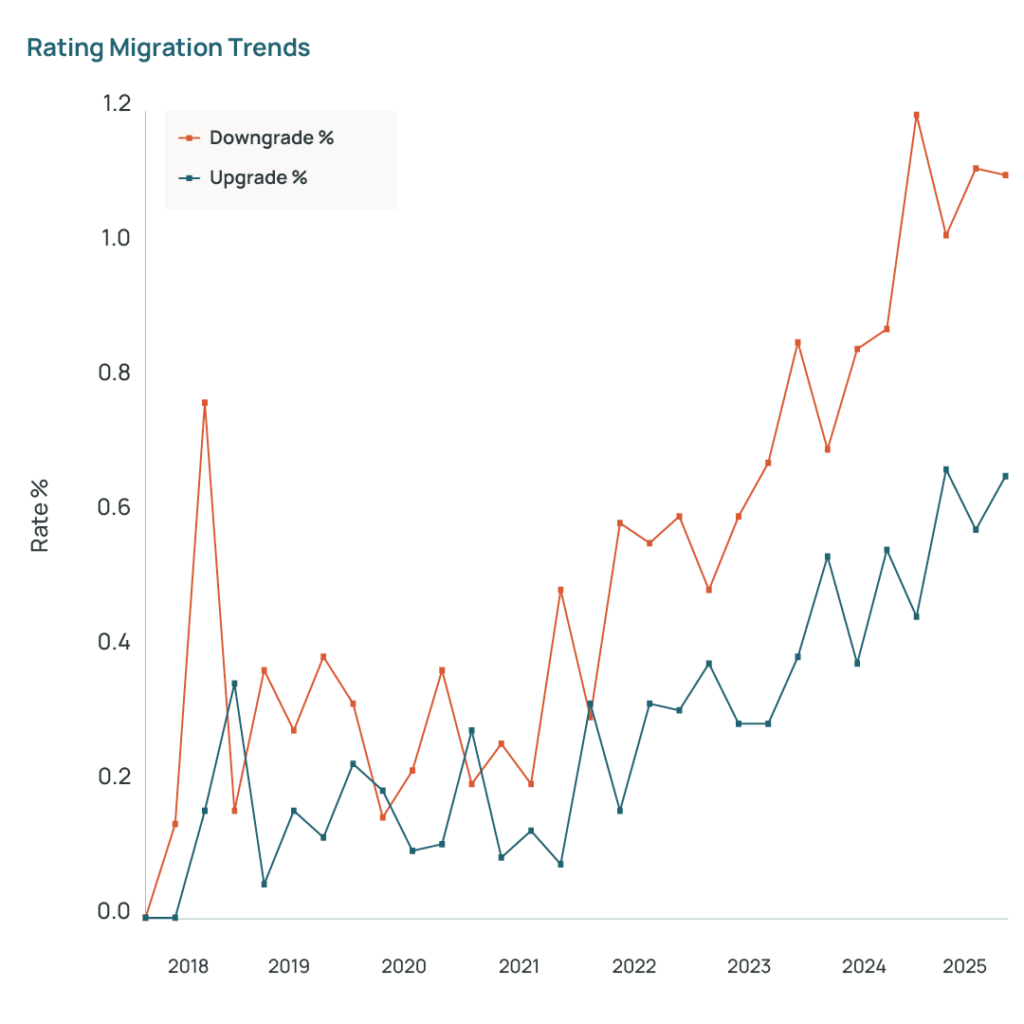

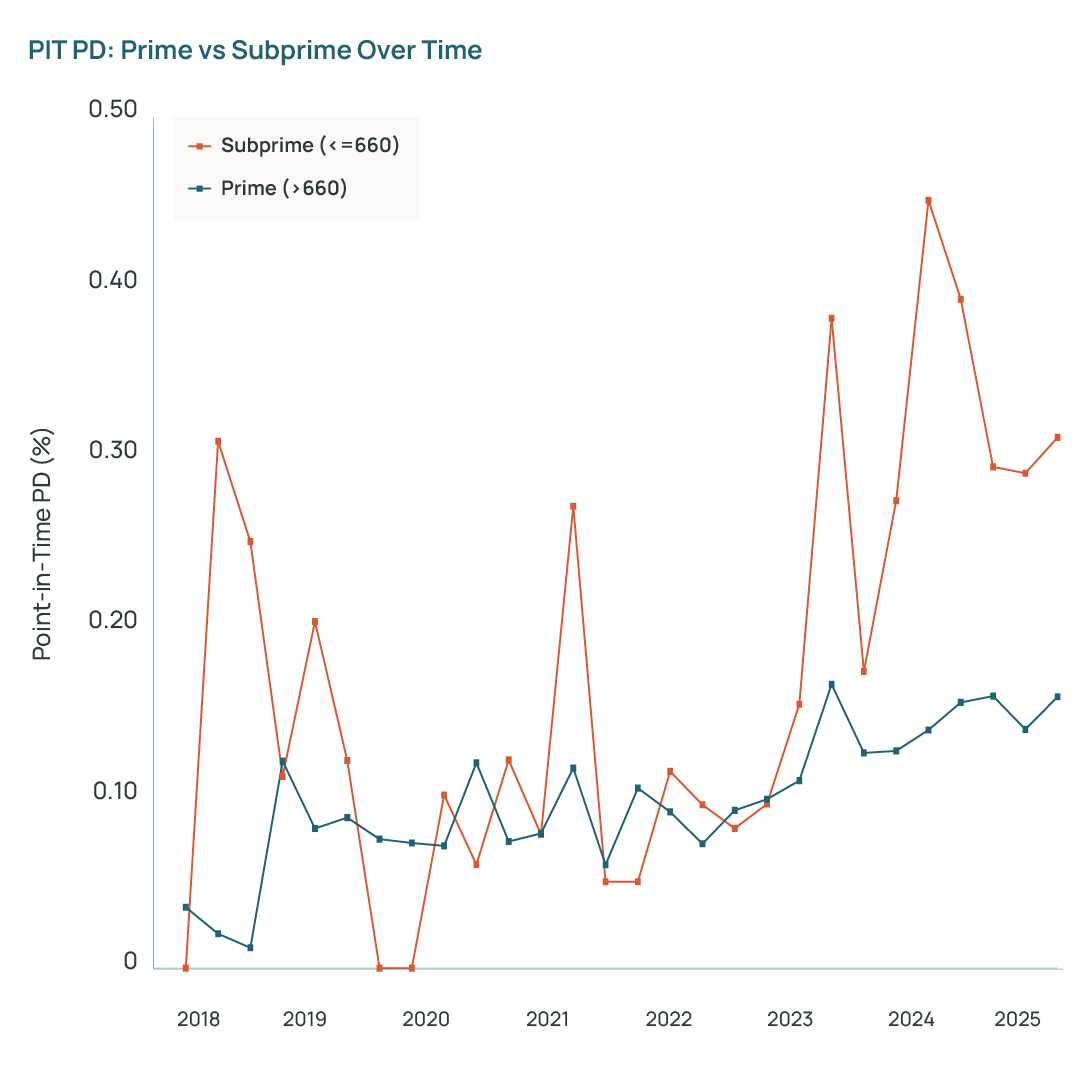

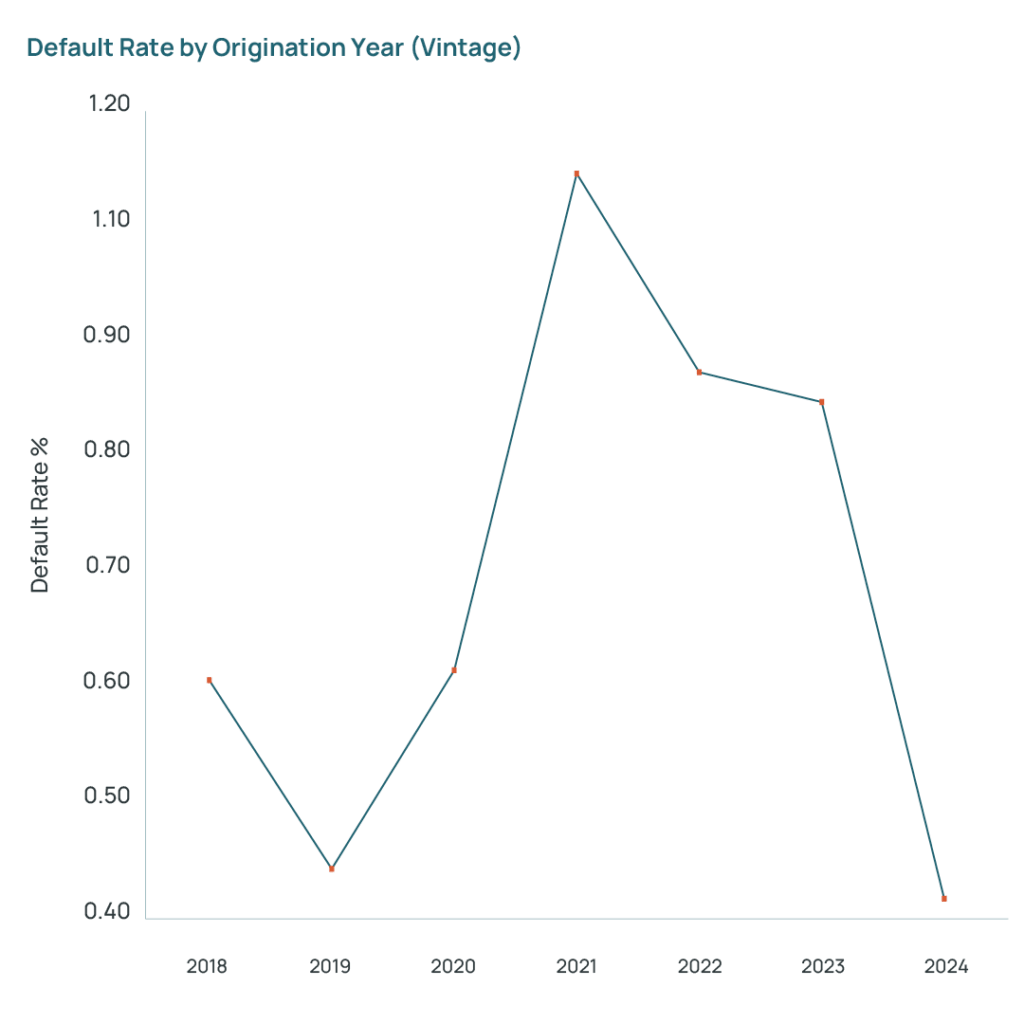

Credit risk indicators from 2021-2024 loan vintages are beginning to show stress patterns compared to pre-pandemic performance. Analysis of auto loan portfolios from AD’s consortium database reveals additional evidence of these stress indicators as demonstrated in the accompanying exhibits, yielding several key observations.

- Exhibit 1 demonstrates an upward trajectory in default rates during recent years, while Exhibit 2 reveals an increasing ratio of credit quality deterioration relative to improvement through delinquency rate migration patterns, indicating heightened underlying credit risk.

- Exhibit 3 reveals a pronounced differentiation in performance between prime and subprime borrower segments.

- Exhibit 4 illustrates a significant increase in default rates for the 2021 vintage, whereas the performance trajectory of the 2024 vintage remains to be determined over time.

- Loans that turn delinquent often do not experience their first delinquency until years two or three.

- Although delinquency rates remain low relative to the GFC, the elevated risk factors above suggest that these cohorts may underperform relative to historical norms.

Financial institutions need to be alert to these warning signs and adopt a proactive risk management posture before losses materialize.

Leveraging Forward-Looking CECL-based Data

Financial institutions should leverage high-quality CECL-compliant loan-level data that captures borrower payment behavior, underlying collateral values, and unique borrower and loan characteristics to discover unrealized, embedded risk in their portfolios. Using CECL-grade data and assumptions also represents an aligned view of credit risk across the organization.

The value of using CECL-grade data is its forecasting power for analyzing correlations between delinquency patterns and key macroeconomic variables.

- A dynamic CECL-based stress testing approach can identify portfolio vulnerabilities sensitive due to recessionary macroeconomic scenarios, collateral value declines, and volatile delinquency migration rates.

- These insights enable proactive risk management rather than reactive loss mitigation.

Methods for Proactive Risk Management

Granular Portfolio Segmentation

Auto loan portfolios with granular, layered segmentation – rather than relying primarily on delinquency bands and credit scores – lead to more effective risk management.

- Portfolios should be further sub-segmented by vintage, loan term length, negative equity status, payment amount, geographic concentration, or borrower debt-to-income ratios.

- This multi-layered view reveals concentration risks and identifies cohorts that are currently performing but carry higher embedded risks.

Applying CECL-based PD models using granular segmentation enables financial institutions to identify loans that are more likely to correlate with future defaults under adverse economic conditions.

Scenario Analysis

Stress testing is an important risk management tool and should be incorporated in active portfolio management.

- By running loan-level PD models across baseline, moderate stress, and severe economic scenarios and looking for payment shock and borrower elasticity, potential defaults and losses can be quantified across segments, identifying areas requiring enhanced surveillance.

- Stress test results can guide adjustments to underwriting criteria during counter-cyclical periods including LTV caps, term restrictions for higher-risk segments or adjusting pricing to reflect true risk-adjusted returns under various economic scenarios.

A CECL-based approach to stress testing reveals portfolio segments exposed to loans with risk factor combinations that exhibit much higher default probabilities in certain recession scenarios.

Data-Driven Strategic Adjustments

Forward-looking analytics inform both portfolio management, underwriting and pricing strategy.

Financial institutions that use consortium or peer loan performance data to benchmark against their own history can validate assumptions and gauge performance against industry peers.

- This insight enables proactive management of segments with delinquency rates significantly exceeding industry benchmarks, which may indicate underwriting weakness.

Technology-Enabled Solutions

Fully integrated technology platforms that seamlessly combine CECL compliance, multi-scenario stress testing, portfolio analytics, and real-time monitoring in a single auditable framework are essential for effective risk management at scale.

- The ALLL+ Platform provides the foundation for CECL compliance and credit loss estimation, featuring integrated scenario management that enables financial institutions to assess portfolio impact under multiple economic forecasts.

- Real-time attribution analysis identifies the specific drivers of allowance changes, while strong governance frameworks ensure full traceability for audit and regulatory examination.

- The Analytics Platform (formerly Risk Modeler) extends these capabilities into strategic portfolio management.

- Its Financial Resilience Assessment combines macro-economic default regression with loan-level risk classifications, while the Model Repository Hub ensures consistency and version control across all analytical frameworks.

- The Portfolio Monitoring Dashboard provides real-time visibility into key metrics, enabling rapid response to emerging trends.

- Advanced modeling capabilities incorporating machine learning can identify complex patterns and correlations that traditional approaches might miss.

When CECL compliance, stress testing, and portfolio analytics share a common data infrastructure, financial institutions gain insight into embedded risk throughout any portfolio.

Conclusion

Post-COVID structural shifts in the U.S. auto loan market—elevated balances, extended terms, and negative equity, demand forward-looking risk management that anticipates vulnerabilities before losses occur. Granular segmentation that looks at vintage, loan term, payment amount and equity status, combined with integrated CECL and portfolio stress testing gives banks a forward-looking view of risk by revealing how specific collateral layers perform under changing economic conditions.

AlterDomus’ CECL-integrated ALLL+ and Analytics Platforms transform compliance infrastructure into strategic advantage through multi-scenario stress testing and real-time portfolio analytics. Financial institutions that deploy these capabilities will identify emerging risks early and respond with precision in an evolving credit risk landscape.

To learn more about Alter Domus’ integrated risk management solutions, contact [email protected].

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

Why Luxembourg is Europe’s Premier Fund Domicile

Luxembourg has cemented its position as Europe’s premier fund domicile, commanding 42% of worldwide cross-border public market assets. We explore what makes it the jurisdiction of choice and what it takes to make it work for your fund.

Conor O’Callaghan

Director, Client &

Industry Solutions

Bruno Bagnouls

Global Partner Director

For global asset managers, fund domicile is a strategic priority defining long-term growth and institutional credibility. As Europe’s primary gateway for alternative investments, Luxembourg offers a sophisticated regulatory environment that enables managers to scale, secure institutional capital, and build trust through cross-border distribution depth.

Luxembourg remains central to European capital access. On 31 March 2026, Luxembourg undertakings for collective investment held total net assets of EUR 6,207.82bn, according to the Commission de Surveillance du Secteur Financier (CSSF). The same CSSF update recorded 288 authorized investment fund managers as of 30 April 2026.

Industry data from the Association of the Luxembourg Fund Industry (ALFI) also shows the scale of the wider market. Luxembourg-domiciled Alternative Investment Funds (AIFs) account for more than €3.1 trillion, representing a massive expansion in the private market space.

For managers in private equity, venture capital, private debt, real estate, and infrastructure, the advantage of Luxembourg lies in what it simplifies. Beyond initial recognition, success depends on robust governance, reporting, and fund service provider arrangements that manage the complexities of the fund lifecycle.

Luxembourg by the Numbers

Luxembourg’s position is built on scale, familiarity, and cross-border distribution. PwC Luxembourg’s 2024 global fund distribution data cited Luxembourg as the first domicile for 72% of the top 51 firms and noted that it handled 52.3% of true cross-border investment funds globally.

The latest ALFI Broadridge cross-border distribution study found that cross-border fund assets reached EUR 8.5 trillion in 2025, with Luxembourg accounting for 42% of worldwide cross-border public market assets..4 For cross-border strategies, broader AIFM services may also be relevant to management, oversight, and reporting needs.

Those figures are significant because institutional investors do not assess domicile in the abstract. They look for structures that their internal teams, consultants, custodians, counsel, and investment committees already understand. Funds domiciled in Luxembourg benefit from that market familiarity.

The benefits of Luxembourg investment funds, therefore, start with recognition. Investors, advisers, administrators, depositaries, auditors, directors, and regulators are familiar with the market’s main fund regimes. That familiarity can reduce friction during fundraising, onboarding, reporting, and ongoing fund operations.

Deep Ecosystem Built for Alternatives

Luxembourg hosts a dense network of administrators, depositaries, auditors, and legal advisers who manage complex operations—from accounting and capital activity to governance and regulatory filings. This ecosystem provides essential regulatory credibility and operational scale for international managers.

The local workforce’s expertise in EU regulatory expectations reduces the need for GPs to build internal teams prematurely. Consequently, Luxembourg-domiciled funds are supported from formation and launch through to reporting and asset exits.

A Financial Center Built for Alternative Strategies

The appeal for alternative managers lies in the range of legal forms and regulatory regimes that can be matched to investor eligibility, asset class, governance needs, and distribution plans. Common options include reserved alternative investment funds, specialized investment funds, investment companies in risk capital, special limited partnerships, and Part II funds. The broader point is straightforward: Luxembourg gives managers several ways to separate the fund vehicle, management company, general partner, and asset holding arrangements.

That flexibility comes with operating demands. A private equity or infrastructure fund may require capital calls, distributions, financial statements, audit support, investor reporting, regulatory filings, board materials, tax data, and document control. These workstreams need clear ownership, agreed timelines, reliable data, and review processes. Limited partners expect accurate reporting, regulators expect evidence of compliance, and boards need materials that support proper oversight. For managers without a local Luxembourg operating team, those requirements can quickly become difficult to manage internally.

This is where third-party support becomes part of the domicile decision. An administrator can help turn the legal structure into an operating model after the fund has been established. Outsourced fund administration services are one example of how managers may support Luxembourg operations without building every function internally. For managers comparing models, the discussion on in house vs third party fund administration is directly relevant.

The “Golden Passport” Angle

The phrase “golden passport” is often used informally to describe one of Luxembourg’s main attractions: The ability to use a European framework for managing and marketing funds across the European Union and European Economic Area.

The CSSF explains that the Alternative Investment Fund Managers Directive (AIFMD) provides an Alternative Investment Fund Manager (AIFM) passport allowing an authorized AIFM approved in an EU or European Economic Area member state to manage alternative investment funds in another member state. It also confirms that the AIFM marketing passport may allow an authorized AIFM to market the AIFs it manages to professional investors across the EU and European Economic Area, subject to the relevant AIFMD conditions.

For managers without an in-house European AIFM, a third-party management company, often referred to as a third-party ManCo, can provide the regulated management company platform required to support a Luxembourg fund. This can be relevant where a non-European GP wants to access European professional investors through an established AIFM structure while keeping investment management, governance, risk, and reporting responsibilities clearly allocated.

This also helps explain why so many funds are domiciled in Luxembourg. The jurisdiction combines European Union market access, a deep alternatives service market, and fund regimes that institutional investors and advisers already know. For a non-European GP, that combination can make Luxembourg easier to explain to investment committees than a less familiar domicile.

AIFM services should still be viewed as an operating and regulatory function, not a distribution shortcut. The AIFM sits within a control framework covering risk management, valuation, delegation oversight, reporting, and investor disclosures.

Regulatory Maturity and AIFMD Luxembourg Compliance

Luxembourg’s strength is not that regulation is light. It is that the regulatory framework is established, widely understood, and supported by a regulator with deep experience in investment funds.

CSSF regulation is a central part of Luxembourg’s credibility with European institutional investors. Under AIFMD Luxembourg requirements, managers and service providers need governance, risk, valuation, reporting, and disclosure processes that can stand up to review.

The framework is also changing. In March 2026, the CSSF confirmed that Luxembourg had adopted the Law of 3 March 2026 to transpose Directive (EU) 2024/927, known as AIFMD II into Luxembourg law. The update introduced additional liquidity management requirements for Luxembourg-domiciled UCITS and, where relevant, authorized AIFMs managing open-ended AIFs, with effect from 16 April 2026.

For closed-end private equity, private debt, real estate, and infrastructure funds, the direct impact will depend on the fund’s structure and redemption terms. The broader lesson applies across strategies: A domicile decision creates ongoing regulatory work. Managers need processes that can absorb rule changes, update documents, collect data, and produce evidence.

Tax Framework and Operating Structure

At a high level, Luxembourg investment funds often operate under specific fund tax regimes rather than ordinary corporate taxation, though this is not uniform across all vehicles. Guichet.lu explains that subscription tax, known as taxe d’abonnement, applies to negotiable securities issued by undertakings for collective investment, specialized investment funds, reserved alternative investment funds, and family wealth management companies, with quarterly declaration and payment obligations.

PwC’s 2026 summary adds that rates are based on total net assets, generally 0.01% for institutional or monetary funds and 0.05% for others, with some exemptions. While tax is a draw, managers must also evaluate treaty access, withholding tax, VAT, substance requirements, and anti-abuse rules alongside regulatory needs.

Stability and Operational Friction

Alternative funds often have lives of ten years or more. Infrastructure and real assets structures may run longer. Luxembourg’s State Treasury reports that major rating agencies assign Luxembourg the highest sovereign rating, AAA or equivalent, with stable outlooks. Its latest update lists stable top-tier ratings from Moody’s, S&P Global Ratings, Fitch Ratings, Morningstar, DBRS, and Scope Ratings. For fund managers, this stability supports long-term planning for regulated vehicles, local service relationships, financing arrangements, and investor governance.

Luxembourg’s position inside the European Union also has implications. It gives managers a domicile inside the EU legal and regulatory system, with access to European fund rules and a professional market built around cross-border capital. That is one reason the country is often described as an EU fund hub and a Luxembourg financial hub.

Conclusion

For international GPs, the value of a Luxembourg domicile extends far beyond initial regulatory and distribution advantages. It provides a mature, reliable foundation for the entire fund lifecycle. Successfully managing a European fund platform requires continuous operational rigor—from the complexities of structuring, compliance, and reporting to the nuances of corporate governance and eventual fund wind-down.

Luxembourg’s distinct advantage lies in its comprehensive service ecosystem, where experienced providers act as an extension of the manager’s team. This infrastructure allows GPs to maintain high operational standards and meet evolving regulatory and investor expectations without the burden of building full-scale local operations from scratch.

By leveraging this sophisticated network, managers can focus on their core investment strategy, secure in the knowledge that every stage of the fund’s life—from launch and day-to-day administration to strategic restructuring—is supported by deep, local expertise.

Through its Luxembourg fund services, Alter Domus provides this critical support, ensuring that operational resilience remains a constant throughout the fund’s journey.

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

Accessing European Capital through Luxembourg

For international asset managers, the path to European institutional capital runs through Luxembourg. In this article, learn how the AIFMD passport, the right fund vehicle, and an integrated third-party operating model can remove the barriers to successful European market entry.

Conor O’Callaghan

Director, Client &

Industry Solutions

Bruno Bagnouls

Global Partner Director

For non-European asset managers, Europe offers a clear opportunity but a harder route to market. Managers seeking allocations from European pension funds, insurers, sovereign wealth funds, and other institutional LPs need more than investor demand. They need a fund structure that LPs recognize, regulators understand, and operating teams can support across multiple jurisdictions.

Luxembourg is often where the strategy comes together. As Europe’s leading domicile for cross-border fund distribution, Luxembourg gives US, Asian, and other non-EU managers a credible route to European capital through familiar fund vehicles, access to the AIFMD marketing passport, and an established ecosystem of AIFMs, administrators, depositaries, auditors, legal counsel, and other specialist providers.

Global cross-border fund assets reached EUR 8.5 trillion in 2025, with Luxembourg representing 42% of worldwide cross-border assets under management. But Luxembourg’s appeal is not based on scale alone. For managers raising capital in Europe, it also offers investor familiarity, regulatory credibility, LP confidence, and a distribution model designed for cross-border fundraising.

For many non-European managers, the central question is how to access European capital through Luxembourg without building a full in-house operating platform. Luxembourg’s mature fund services market offers a more practical route. By working with experienced third-party fund administration, non-European GPs can reduce operational lift, meet local requirements, and focus more time on investment performance and investor relationships.

Why Managers Choose Luxembourg

Scale is only part of Luxembourg’s appeal. Managers choose Luxembourg because European institutional investors are familiar with its structures, advisers, service providers, and regulatory framework. That familiarity can reduce friction during fundraising, support LP due diligence, and give investors confidence that the fund is being operated within a credible European environment.

For non-EU GPs, a Luxembourg platform can also demonstrate operational maturity before the first close. It gives finance, legal, investor relations, and operations teams a clearer framework for onboarding investors, coordinating capital activity, managing service providers, and meeting ongoing European obligations.

For CFOs and COOs, the AIFM relationship is also an operating decision. The right AIFM can accelerate time to market while reducing operational friction through effective governance, delegation oversight, valuation, risk management, and regulatory reporting.

Why European Capital Matters Now

Expanding fundraising into Europe can help global asset managers diversify their investor base and scale their platforms. A Luxembourg structure can help global managers raise capital in Europe while giving LPs a familiar governance and reporting framework.

State Street’s 2025 private markets study found that LPs remain focused on private equity, private credit, real estate, and infrastructure, with developed Europe attracting renewed interest from institutional investors.

As European LPs increase their allocations to alternatives, their operational due diligence expectations have also tightened. They are looking for onshore structures with strong governance, clear reporting, and reliable investor protection. Luxembourg benefits from this shift because its fund structures are familiar to global investors and commonly used for cross-border alternative strategies.3

For a non-EU GP, an onshore Luxembourg platform can answer many investor questions early in the fundraising process. It gives LPs a familiar structure, a recognized jurisdiction, and an operating model built around European requirements.

Regulatory Barriers to Ad Hoc Market Entry

Historically, many international fund managers relied on reverse solicitation to raise European capital. That approach is becoming harder to defend as a long-term distribution strategy.

NPPRs are well suited to targeted fundraising campaigns but do not provide pan-European market access. Managers seeking to raise capital across multiple jurisdictions must navigate separate local filings, creating additional complexity and administrative burden.

Reverse solicitation is also a narrow exception, not a scalable fundraising plan. Under Luxembourg guidance, reverse solicitation requires that the investor act on its own initiative, without solicitation by the alternative investment fund (AIF), the Alternative Investment Fund Manager (AIFM), or an intermediary.4 For managers running an active European fundraising campaign, relying on reverse solicitation creates compliance risk.

The Luxembourg Solution: The AIFMD Passport

A more durable route is the Alternative Investment Fund Managers Directive (AIFMD) marketing passport. Under AIFMD, authorized AIFMs can market EU AIFs to professional investors across the European Economic Area, subject to the applicable notification process.

For managers focused on EU investor access through Luxembourg, the AIFMD passport offers a more scalable route than country-by-country private placement. A Luxembourg AIF managed by an authorized EU AIFM can use the AIFMD passport to reach professional investors across Europe. The result is a single regulated platform instead of a country-by-country fundraising patchwork.

Understanding the AIFM Requirement

For managers new to the European regulatory model, understanding what an AIFM does is an important first step. The AIFM is not simply a service provider; it is responsible for key oversight functions, including risk management, valuation, compliance, delegation oversight, and regulatory governance.

This is essential because access to the pan-European marketing passport depends on the fund being managed by an authorized, onshore AIFM. For a non-EU GP, Luxembourg can provide a practical base for European distribution when the fund is supported by an authorized AIFM. It requires regulatory capital, local substance, experienced conducting officers, governance arrangements, and time with the Commission de Surveillance du Secteur Financier (CSSF).

Many global managers appoint a third-party AIFM instead of building the infrastructure in-house. This gives the fund access to an authorized management company while allowing the GP to retain control of portfolio management, deal origination, and investment strategy.

Before the first close, managers need clear ownership of investor onboarding, AML/KYC checks, capital calls, NAV production, financial statements, board materials, regulatory filings, and investor reporting. Weak workflows between the AIFM, administrator, depositary, auditor, and legal counsel can create delays even when the fund structure itself is sound.

The Third-Party Fund Services Model

The third-party model separates investment decision-making from institutional fund operations. The GP focuses on sourcing, executing, and managing investments. The third-party provider supports the fund’s regulatory, administrative, depositary, corporate, and reporting needs.

Managers weighing operating models may also want to compare in-house vs. third-party fund administration before deciding how much infrastructure to build internally.

Experienced providers such as Alter Domus can support the main operating requirements through one platform:

- AIFM services and compliance monitoring: Oversees risk management, compliance monitoring, valuation policies, and regulatory obligations.

- Fund administration: Specialists manage capital calls, investor distributions, financial statement preparation, and net asset value (NAV) calculations.

- Depositary services: AIFMD requires every passported fund to appoint an independent depositary responsible for cash-flow monitoring, asset safekeeping, and ownership verification.

- Corporate secretarial and governance support: Covers board support, domiciliation, entity maintenance, approvals, and governance documentation.

- Investor reporting and onboarding: Includes investor onboarding, Anti-Money Laundering (AML) and Know Your Customer (KYC) checks, data collection, investor communications, and regulatory reporting inputs.

By using one integrated provider, global managers can avoid coordinating several local vendors. The cost model also becomes more flexible, moving from fixed in-house infrastructure to a fund-level operating expense.

Practical Steps for Successful Market Entry

For an international asset manager, launching a passported Luxembourg fund usually depends on getting the right structure, partners, and operating model in place before fundraising gains momentum.

1. Appoint a licensed third-party AIFM

Luxembourg AIFM services give managers the regulatory foundation for pre-marketing, marketing, governance, and ongoing oversight across the European Economic Area. For non-EU GPs, appointing a third-party AIFM can also reduce the time, cost, and complexity of building a regulated European management platform in-house.

2. Select the Right Fund Vehicle

The fund vehicle should match the manager’s strategy, investor base, and speed-to-market requirements. The société en commandite spéciale (SCSp), or special limited partnership, is often attractive to US and UK managers because it offers contractual flexibility and characteristics familiar to common-law partnership structures.

3. Coordinate Fund Partners

The GP should establish clear operating workflows between the AIFM, fund administrator, depositary, legal counsel, auditor, and investor reporting teams. This is where many launches lose time. The structure may be right, but weak coordination can delay onboarding, reporting, capital calls, and first-close readiness.

4. Prepare for evolving AIFMD requirements

AIFMD II introduces additional expectations for areas such as loan-originating funds, liquidity management, delegation, substance, and supervisory reporting. Managers do not need to lead with the technical detail, but they do need to know whether their Luxembourg platform can support these requirements in practice. This will be crucial for private credit strategies or open-ended structures, as regulatory and reporting expectations can directly affect launch planning and ongoing operations.

5. Align with ESG and LP Due Diligence Expectations

European institutional investors increasingly expect managers to provide clear, reliable sustainability and portfolio data. Luxembourg is the leading domicile for European sustainable private market funds, representing 77.0% of total sustainable private market fund assets under management in Europe.

Turn Commercial Intent into Operational Reality

A Luxembourg fund structure is more than a regulatory formality. Used well, it signals operational maturity to European LPs and gives non-European GPs a clearer route to cross-border fundraising.

The AIFMD passport only delivers its full value when the fund is structured, operated, and reported on to institutional standards. That takes local knowledge, strong governance, and dependable day-to-day execution.

Alter Domus supports international GPs through AIFM services, depositary oversight, corporate services, and investor reporting. By combining local Luxembourg expertise with technology-enabled operating support, Alter Domus helps managers reduce operational lift and stay focused on investment performance, investor relationships, and long-term growth.

Ready to accelerate your European fundraising strategy?

Discover how Alter Domus’ AIFM services in Luxembourg can support your European market entry, from fund launch through ongoing oversight.

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

Navigating Luxembourg’s Fund Structures

Luxembourg offers alternative managers a range of fund structures, each with its own regulatory profile, investor eligibility rules, and operational demands. Read on to learn how to navigate the key differences and identify the vehicle best suited to your strategy.

Conor O’Callaghan

Director, Client &

Industry Solutions

Bruno Bagnouls

Global Partner Director

Luxembourg fund structures are often considered by alternative asset managers seeking a European domicile, particularly where the target investor base includes European institutional or professional investors. The market is large and operationally mature. As of 31 January 2026, undertakings for collective investment in Luxembourg held EUR 6,294.473bn in net assets, across 13,286 active fund units.

That scale does not make structure selection simple. Fund structures in Luxembourg differ by regulatory status, investor eligibility, legal form, tax treatment, time to launch, and reporting. A private equity strategy with a small group of institutional limited partners may raise different questions than a private debt platform seeking a European passport, or a real estate manager assessing access to private wealth investors.

Closed-ended and semi-liquid structures are also playing an increasingly prominent role in the Luxembourg fund landscape. Closed-ended vehicles remain well suited to strategies with long investment horizons, such as private equity, infrastructure, and private credit, where fund duration aligns with the illiquidity of underlying assets.

Semi-liquid structures, meanwhile, are gaining ground as a way to extend access to private markets for wealth and semi-professional investors, offering periodic redemption windows or evergreen designs without departing from a longer-term investment strategy. This added flexibility introduces greater operational complexity, particularly around subscription and redemption processing and ongoing valuations, reinforcing the importance of selecting a fund administrator equipped to support hybrid liquidity models.

For non-European managers, comparing different fund structures in Luxembourg usually starts with practical questions: who can invest, how the fund can be marketed, what level of regulatory oversight applies, and what operating obligations follow after launch.

While Luxembourg offers several well-established fund structures, including the RAIF, SIF, SICAR, and ELTIF, these aren’t the only options available. Depending on strategy, investor base and regulatory requirements, ans SCSp (Special Limited Partnership) can also operate as an unregulated Alternative Investment Fund (AIF). The structures below highlight four of the most commonly used regulatory frameworks:

Reserved Alternative Investment Fund (RAIF)

The Reserved Alternative Investment Fund (RAIF) is commonly used where time to market is a major consideration and has become one of the most widely adopted structures for alternative investment managers establishing funds in Luxembourg. A RAIF qualifies as an alternative investment fund (AIF), can invest in all asset types, and is not itself subject to product approval by the Commission de Surveillance du Secteur Financier (CSSF).

It must appoint an authorized external Alternative Investment Fund Manager (AIFM). Where the AIFM is domiciled in the European Union (EU), the RAIF can use a passport to market shares, units, or partnership interests to well-informed investors across the EU.

This indirect supervision model is the main feature that separates the RAIF from directly regulated structures. The fund is not approved as a product before launch, but the AIFM is regulated and must meet AIFM obligations.

A RAIF may be relevant where a manager is targeting well-informed investors and needs an AIFMD structure supported by AIFM services in Luxembourg and European marketing capability through the appointed AIFM. RAIFs can be structured in several legal forms, including a corporate vehicle, a common contractual fund, or a partnership. In private markets, a RAIF is often paired with an SCSp.

The operating model for a RAIF typically includes AIFM oversight, depositary arrangements, valuation, net asset value (NAV) production, investor reporting, regulatory reporting, and audit support. While the structure can accelerate time-to-market compared with some directly regulated alternatives, managers must still establish the governance and operational framework required to support ongoing compliance and investor expectations.

Specialised Investment Fund – SIF

The Specialised Investment Fund (SIF) is a directly regulated Luxembourg fund structure for well-informed investors. It is governed by the Luxembourg Law of 13 February 2007, as amended, and most SIFs qualify as AIFs because of the broad definition of an AIF. SIFs that qualify as AIFs are generally required to appoint an AIFM, unless a limited exemption applies. A SIF managed by an authorized EU AIFM can use a passport for marketing to professional investors in the EU.

The main difference between a SIF and a RAIF is fund-level supervision. A SIF is subject to direct CSSF oversight, while a RAIF is supervised indirectly through its AIFM. Some institutional investors may prefer, or require, a directly regulated product. That preference can affect fund legal structure in Luxembourg, especially for managers raising from pension funds, insurers, sovereign wealth funds, or other regulated investors.

A SIF may invest across asset classes and can be established as an FCP, SICAV, SICAF, or another permitted form. Its net assets must reach EUR 1.25m within 24 months after authorization.

Direct product supervision can affect the setup process, but it can also support investor comfort where the target limited partner base places weight on regulated fund status. This does not make the SIF a default choice. It means the SIF may form part of the discussion where fund-level authorization, ongoing CSSF oversight, and a recognized regulated framework are relevant to the distribution plan.

Investment Company in Risk Capital (SICAR)

The Investment Company in Risk Capital (SICAR) was designed for investment in risk capital. It is most often associated with private equity and venture capital strategies, where the investment policy centers on capital at risk rather than diversified asset allocation.

A SICAR that qualifies as an AIF must appoint an AIFM unless a limited exception applies. A SICAR managed by an authorized EU AIFM can use a passport for marketing to professional investors in the EU.

Unlike other fund types that may be set up in contractual form, a SICAR must be constituted as a corporate entity with fixed or variable share capital. The subscribed share capital, including share premiums, must reach EUR 1m within 24 months after authorization.

The SICAR’s focus on risk capital makes it narrower than a general alternative fund vehicle. Its use case is tied to investments where capital is placed at risk with the aim of developing, launching, or growing companies or projects. That focus can make the SICAR relevant in private equity and venture capital contexts but less relevant for strategies that need broader asset flexibility or diversification features.

European Long-Term Investment Fund (ELTIF 2.0)

The European Long-Term Investment Fund (ELTIF) is a European framework for AIFs investing in long-term assets. The revised ELTIF rules, often called ELTIF 2.0, have applied since 10 January 2024. Under CSSF guidance, an AIF must be managed by an authorized EU AIFM and comply with the ELTIF Regulation to be authorized as an ELTIF.5

Luxembourg has become a major domicile for ELTIFs. As of July 2025, the European Securities and Markets Authority register listed 211 ELTIFs in the EU, with 124 domiciled in Luxembourg, or nearly 60% of the total.

ELTIFs are often discussed by managers considering private wealth distribution, but the structure is not a retail shortcut. It brings product rules, eligible asset requirements, portfolio composition requirements, liquidity design questions, investor disclosures, valuation frequency, reporting, and distribution controls. These requirements can become more demanding where a vehicle is designed for a wider audience than a traditional institutional fund.

| Structure | Common Use Case | Regulatory Profile | Time-to-Market Considerations | Distribution & Compliance Considerations |

|---|---|---|---|---|

| RAIF | Often used for alternative strategies targeting well-informed investors | Not directly approved by the CSSF as a fund product, but managed through an authorized AIFM | Often considered where launch timing is a priority | Can support European marketing through the appointed AIFM where passporting conditions are met |

| SIF | Used where the investor base prefers a regulated fund product | Directly regulated by the CSSF | Authorization can add time to setup | May suit investors who place weight on direct fund-level supervision |

| SICAR | Often associated with private equity and venture capital risk capital strategies | Directly regulated and focused on risk capital | Authorization and structure requirements need to be built into setup planning. | More focused use case than broader alternative fund vehicles |

| ELTIF | Used for long-term asset strategies, including some private wealth distribution models | Requires authorization under the European Long-Term Investment Fund framework | Product rules and authorization requirements can affect setup timing | Brings rules on eligible assets, portfolio composition, liquidity, disclosures, valuation, and distribution controls |

Key Decision Factors

Structure selection often starts with the investors. A vehicle for a small group of professional investors may look different from a vehicle intended for multiple European markets or private wealth channels. Investor eligibility, onboarding standards, local distribution rules, reporting expectations, and tax reporting can all affect the workable options.

For managers reviewing fund structuring Luxembourg options, these factors help narrow the discussion without treating any single vehicle as the default answer. Searches for Luxembourg fund structures tax advantages often focus on headline tax treatment, but the more useful analysis is specific to the fund, investors, asset location, and distribution plan. Tax outcomes can vary by legal form, regime, and cross-border facts, so they should be assessed alongside regulatory and operational requirements.

Time to market is another practical consideration. A RAIF can avoid direct CSSF product approval, while a SIF, SICAR, or ELTIF authorization involves regulator review. That does not make one route better than another. It means setup timing, governance, and investor expectations need to be matched.

Distribution strategy also matters. Managers comparing different fund structures in Luxembourg need to consider whether the vehicle is intended for one market, several European markets, or a broader investor channel. Where an AIFMD passport is relevant, the role of the authorized AIFM becomes central to the operating model.

Conclusion

Once the fund’s legal structure in Luxembourg is decided, the work shifts from structure selection to operational execution. Managers need to translate the chosen vehicle into a working model that covers service provider onboarding, governance processes, accounting, net asset value (NAV) production, investor services, regulatory reporting, data flows, and audit support.

That execution work can be different for each structure. A RAIF may place more emphasis on coordination with the appointed AIFM, while a directly regulated SIF, SICAR, or ELTIF may require additional focus on authorization, reporting, and ongoing product obligations. Distribution plans can also affect the operating model, particularly where the fund is intended for several European markets or a wider investor channel.

Alter Domus supports these operational requirements in Luxembourg through AIFM and fund administration services. Its role is focused on administration, governance, reporting, data management, and implementation support after the legal, tax, and regulatory framework has been established.

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

Why Successor Agency Matters in Distressed Debt and Restructuring Transactions

As credit agreements enter distress, the demands on administrative agents change rapidly. Successor agency has become a critical tool for ensuring continuity, independence, and effective coordination when transactions are under pressure.

Emily Ergang Pappas

Group Head of Legal, Alter Domus

When a credit agreement enters a distressed situation, the focus of the transaction naturally shifts to what the next best steps are for all parties, including the borrower and the lenders, and any potential restructuring strategy. It’s at this point that some of the most significant challenges in the life of the loan emerge.

In a distressed situation, communication becomes more complex; creditor groups expand and change; and timelines compress. Decisions that once took days need to be made in hours. The administrative framework supporting the transaction is suddenly placed under intense pressure, and not all administrative agents are ready, able, or willing to take on the additional burdens presented in a distressed debt situation. This is where a potential successor agency transaction can become part of the solution.

This article explores why successor agency has become an increasingly important consideration in distressed debt transactions, restructurings, bankruptcies, and other challenging credit events. It examines the factors driving transitions away from traditional lending institutions, the value of independence during complex situations, and why experience can make a meaningful difference when transactions come under pressure.

Distressed Debt Changes the Role of the Agent

In agenting a loan facility, the responsibilities of an administrative agent or collateral agent are generally straightforward. Information flows predictably, stakeholder interests are broadly aligned, and the focus remains on efficient administration.

Distress changes that dynamic entirely.

Whether the situation involves a potential bankruptcy filing, a liability management exercise, a liquidation, a debt-for-equity transaction, or a collateral enforcement process, the agent quickly becomes a central point of coordination across lenders, restructuring counsel, financial advisers, borrowers, investors, and other stakeholders.

The role moves beyond administration.

New lender groups emerge. Advisers change. Negotiations become more complex. Information needs to move quickly and accurately between parties that do not always share the same objectives.

Every restructuring develops its own characteristics. No two situations unfold in exactly the same way, and no two stakeholder groups approach challenges in the same manner. That is why distressed agency requires a different skill set than traditional loan administration and why bringing in a successor agent is often the next best step in mitigating the risk behind a distressed debt situation.

Why Institutions Often Seek an Independent Successor Agent

Many distressed successor agency appointments begin when the original administrative agent determines it is no longer the right party to continue in the role.

This is rarely a reflection of capability. More often, it reflects the realities of operating within a regulated banking environment.

As transactions become more complex, institutions may face governance requirements, balance sheet considerations, internal policies, or conflict-management concerns that make continued involvement increasingly challenging. Holding collateral, overseeing enforcement actions, managing creditor communications, or remaining involved through lengthy restructuring proceedings may no longer align with the institution’s objectives.

As a result, lenders, and sometimes the agent itself, often look for an independent successor agent capable of stepping into the transaction without disrupting progress.

The challenge is that distressed transitions are rarely routine. Stakeholders need confidence that the successor agent can quickly understand the transaction, assume the mantle of agent in a truncated timeline, and help keep a complicated process moving forward.

Not Every Successor Agency Appointment Is the Same

Successor agency appointments exist on a spectrum.

At one end are routine transitions where the transaction remains healthy and stakeholder alignment is largely intact.

At the other are distressed situations where the successor agent is stepping into an environment characterized by heightened scrutiny, competing interests, often within the lender group itself, let alone borrower v. lenders, and rapidly changing circumstances.

These appointments demand more than operational competence; they require experience managing sometimes difficult lender communications during enforcement actions, coordinating parties through court-supervised processes, working alongside restructuring and bankruptcy counsel, and maintaining continuity while negotiations continue around them.

The transaction documents provide the framework.

Experience often determines how effectively stakeholders operate within it.

Why Independence Matters

For law firms advising lender groups, independence is often one of the most important factors when selecting a successor agent, particularly in a distressed debt situation.

An independent successor agent is not a lender. It does not hold an economic position in the transaction, nor does it have competing interests that may influence decision-making.

That neutrality becomes particularly valuable when lender groups become fragmented or when difficult decisions need to be made.

Whether coordinating communications among creditors, facilitating lender instructions, supporting enforcement strategies, or administering a transaction through a restructuring process, an independent successor agent provides a trusted framework that allows stakeholders to focus on resolving the issues in front of them.

In distressed situations, trust and transparency are often just as important as technical expertise.

Experience Matters When Transactions Become Difficult

Restructuring documents, court filings, and legal processes create the framework for a loan transaction.

What determines how smoothly that transaction progresses is often the quality of communication between the people involved and the strict adherence to the legal documentation that exists.

The most challenging situations rarely arise because documentation is inadequate. More often, they emerge because stakeholders have different priorities, circumstances change quickly, and decisions need to be made under pressure.

Success depends on the ability to bring together lenders, law firms, restructuring advisers, consultants, and borrowers while maintaining clear communication throughout the process.

This is where experience becomes particularly valuable.

Teams that have worked through bankruptcies, liquidations, enforcement actions, liability management exercises, and complex restructurings understand that technical expertise alone is not enough. Judgement, responsiveness, and stakeholder management are often what keep a transaction moving when circumstances become more challenging.

The best successor agents understand both the legal framework and the practical realities of navigating difficult situations, and know the appropriate contacts in the space that can be utilized on short notice to help smooth the process out.

Experience Matters Most When Complexity Increases

Private credit has grown significantly over the last decade. Capital structures have become more complex, stakeholder groups are often larger, and expectations around transparency and execution continue to rise.

For law firms advising clients through restructurings, bankruptcies, and other challenging credit events, successor agency is no longer simply about replacing an incumbent.

It is about putting the right experience, independence, and expertise around the transaction at the moment it matters most and in a way that helps navigate the challenges ahead.

Alter Domus has extensive experience acting as successor agent in distressed and complex credit situations, supporting lender groups, law firms, and restructuring advisers through transitions that require far more than administrative expertise. Whether it is a borrower filing bankruptcy in a short window of time, or a quick turnaround on enforcement actions, Alter Domus is ready and able to step in and help guide the process using its valuable and varied experience in the distressed debt space.

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

AIFMD Annex IV: A Guide to Reporting Obligations

Stay ahead of AIFMD Annex IV reporting demands, no matter how complex your fund structure or marketing footprint. Explore practical solutions that reduce effort, cut risk, and ensure your filings stand up to regulatory scrutiny.

Alain Delobbe

Head of AIFM, Alter Domus

Alternative Investment Fund Managers Directive (AIFMD) Annex IV reporting is one of the most technical recurring obligations facing alternative managers with EU funds or marketing activity in Europe.

For CFOs, COOs, and compliance leaders, the pressure is not just legal. It is operational. Firms need to collect consistent data across managers, funds, service providers, and systems, then convert it into a filing that can stand up to regulator scrutiny.

That is hard enough in one jurisdiction. It gets harder when the structure spans multiple funds, multiple markets, or non-EU marketing routes.

While the complexity is high, the reporting framework is established, the core filing logic is clear, and practical solutions exist to reduce both effort and risk.

What is AIFMD Annex IV Reporting?

Annex IV is the reporting framework that provides regulators with periodic transparency on Alternative Investment Funds (AIFs) and the Alternative Investment Fund Manager (AIFM) manages or markets.

Its core purpose is oversight, monitoring exposures, leverage, liquidity, concentrations, and wider financial stability risks. That is why the framework sits under Article 24 of AIFMD and why the broader supervisory discussion now focuses on data quality, consistency, and overlap across reporting regimes.1, 3

Recent ECB and ESRB work shows how leverage can amplify gains and losses, create margin and collateral pressure, and transmit stress through counterparties and markets, making Annex IV a critical part of the supervisory toolkit.

The scope is broad, applying to authorized EU AIFMs, smaller registered managers in some cases, and non-EU AIFMs marketing into Europe under national private placement regimes. The exact obligation depends on the manager’s status, the funds involved, leverage, assets under management, and where marketing takes place.

The ESMA states that transparency information covers the AIFM and the AIFs it manages and, where relevant, markets. CSSF guidance also confirms that non-EU AIFMs can have Article 24 reporting obligations when they market AIFs to professional investors in Luxembourg. 5

Post‑Brexit, the FCA has implemented a reporting framework broadly equivalent to the Annex IV regime, which is, in practice, largely aligned with the requirements previously defined by ESMA. UK AIFMs are therefore required to submit Annex IV reports to the FCA covering both UK and non‑UK AIFs they manage.

In addition, EU AIFMs marketing AIFs in the UK under the National Private Placement Regime are also required to submit UK Annex IV reports to the FCA in addition to the reports submitted to their EU National Competent Authorities under the ESMA framework.

What does Annex IV reporting include?

At the fund level, Annex IV requires information on the AIF, including identifiers, net asset value, investment strategy, geographical focus, top exposures, principal markets, instruments traded, portfolio concentrations, and leverage.

The reporting guidelines also require rankings such as top principal exposures and top portfolio concentrations, which means firms need more than raw holdings data. They need data that is classified, aggregated, and mapped to the reporting taxonomy. 5

Annex IV requires manager level information, including assets under management and other data under Article 24(1) of the AIFMD. This creates a distinction between AIFM level and AIF level information, which is reflected in the separate reporting sections under the EU Annex IV transparency framework.

Firms therefore need a clear ownership model for both sets of data, ensuring consistency between manager level reporting (e.g. aggregate exposures, leverage, risk profile) and fund level disclosures collected by EU National Competent Authorities and subsequently shared with ESMA on an ongoing basis.

Risk reporting is a key focus of Annex IV, covering leverage, liquidity, exposures, and concentrations to help supervisors identify potential financial stability risks. ECB analysis confirms AIFMD data is used to assess these risks. ESMA’s 2025 annual assessment adds that substantially leveraged funds increased their median leverage ratio from 450% in 2022 to 530% in 2023. 2, 3

The reporting itself is structured. The legal template sits in Annex IV to the Level 2 Regulation, and ESMA’s technical guidance sets the filing logic and validations used in practice. Revision 6 introduced stricter validation rules and made more fields mandatory to improve data quality.

Annex IV Reporting Frequency and Deadlines

Reporting deadlines vary by size and jurisdiction, necessitating strict adherence to specific timelines.

- Reporting frequency thresholds: Frequencies—annual, half-yearly, or quarterly—depending on the AUM managed by the manager. ESMA guidelines define these cycles and the rules for transitioning between them.

- Submission timelines and regulators: Reports are generally due within 30 days following the end of the reporting period, with an additional 15‑day extension for fund‑of‑funds structures. Reporting periods typically align with the quarter‑end dates (i.e. the last business days of March, June, September, and December).

The initial report is due from the inception of the AIF, covering the first full reporting period. Regulators expect a report to be submitted in all cases, even where the fund has not yet started deploying capital; in such cases, a nil report must be filed. - Differences across jurisdictions: European legal frameworks exist, but submission practices vary. ESMA identifies over 100 distinct EU reporting templates, leading to overlaps and operational burdens for cross-border managers. Market participants therefore expect that the forthcoming technical guidelines under AIFMD II will lead to a more standardized and streamlined reporting framework, reducing fragmentation and improving consistency across the EU.

Key Challenges in Annex IV Reporting

Despite the clarity of the framework, managers frequently encounter several major operational hurdles when preparing their Annex IV submissions.

- Data Fragmentation and Aggregation Issues

The main challenge with Annex IV reporting lies in data aggregation and consistency. The report requires inputs from multiple sources, including accounting, portfolio monitoring, risk management, reference data, and investor data. In many cases, a significant portion of this information is provided by external service providers, which adds further complexity in terms of data quality, timeliness, and reconciliation.

ESMA’s 2025 discussion paper says the diversity of reporting templates contributes significantly to operational inefficiencies and higher compliance costs, especially for firms overseeing different fund types across multiple Member States. 1 - Complexity of Calculations and Definitions

Even when the source data exists, the calculations are not always straightforward. Leverage, principal exposures, geographical focus, portfolio concentration, and instrument classification depend on specific definitions and reporting logic. If teams apply different definitions in different systems, the filing may be internally inconsistent before it ever reaches the regulator.

In addition, the evolution of regulatory requirements over the past recent years reflects a clear trend toward enhanced expectations—not only regarding the accuracy of quantitative data, but also the inclusion of qualitative disclosures, notably in relation to the AIFM’s risk management framework. - Manual Processes and Operational Inefficiencies

Manual work remains a weak point. Re-keying data, stitching together spreadsheets, and checking outputs line by line might get a report filed, but it does not scale. It also makes deadline pressure worse.

ESMA’s current push toward integrated data collection reflects the same issue from the regulator’s side: too many fragmented templates, too much duplication, and too much room for inconsistency. 1, 5 - Regulatory Scrutiny and Risk of Non-Compliance

Annex IV is not a box-ticking exercise. Regulators use the information for supervision, which means late, incomplete, or inconsistent submissions create real risk. The ESMA states that regulatory reporting is an integral part of its supervision strategy and that receiving accurate information on time helps it focus supervisory work.

Addressing these issues requires a proactive and systematic approach to data management and workflow design.

Best Practices for Efficient Annex IV Reporting

To overcome the common challenges, firms can adopt several best practices to streamline their Annex IV processes and improve data integrity.

- Centralizing and Standardizing Data

The first step is to build one reporting data set, not numerous partial versions. That means common definitions, mapped source systems, and clear ownership for manager-level and fund-level data. Without that foundation, every filing period turns into a fresh reconciliation cycle. - Automating Reporting Workflows

Automation matters because Annex IV is repeatable work with fixed deadlines. Data extraction, mapping, validation, and output generation should happen through a controlled workflow wherever possible. The point is not to remove judgment. It is to remove avoidable manual handling. - Implementing Strong Validation and Controls

Validation should happen before submission, not after a rejection. ESMA’s stricter Revision 6 rules make that even more important. Firms need pre-submission checks, exception management, documented sign-offs, and a clear audit trail that shows how each key figure was produced. 5 - Leveraging External Expertise

External support can make sense when a firm lacks scale, operates across jurisdictions, or is entering a new market. The value is not just extra capacity. It is access to people who understand the regulation, the reporting logic, and the local filing mechanics at the same time.

By following these practices, firms can transform a challenging regulatory obligation into an optimized, low-risk process.

How AIFM Providers Support Annex IV Compliance

End-to-End Reporting Support

A strong AIFM provider can support the full process: data collection, interpretation, production, validation, and submission support. This helps managers transition from fragmented reporting processes to a more controlled and structured operating model, while ensuring access to the latest regulatory developments and industry best practices.

Reducing Operational and Regulator Risk

The real gain is risk reduction. A better process cuts manual handling, improves consistency, and makes deadlines easier to meet. It also gives senior stakeholders better visibility into what is being reported and why.

Support Growth and Market Entry

Annex IV gets harder as firms grow. New funds, new investor channels, and new jurisdictions all add reporting complexity. A provider that already has the infrastructure and jurisdictional knowledge can help managers expand without rebuilding the reporting model each time.

Turning Annex IV Reporting into a Strategic Advantage

Most managers will never describe Annex IV as strategic work. That is fair. It is a regulatory obligation. But the firms that handle it well usually get more than a compliant filing out of the process. They end up with better control over fund data, clearer ownership across teams, and a more reliable picture of exposures, leverage, and operating risk.

Simplifying AIFMD Annex IV Reporting with the Right Partner

Annex IV reporting is technical, recurring, and exposed to regulatory scrutiny. It touches legal interpretation, data quality, workflow design, and local filing practice all at once.

Firms that rely on manual work and fragmented data can still get reports out the door, but they pay for it in time, risk, and rework. Firms that centralize data, automate where it makes sense, and use experienced support are in a stronger position to file accurately, scale across jurisdictions, and keep compliance pressure under control.

Simplify Your AIFMD Reporting. Ready to reduce your operational burden and compliance risk? Explore how Alter Domus’ AIFM Services can help you file accurately and scale across jurisdictions.

References

- European Securities and Markets Authority. (2025, June 23). Discussion paper on the integrated collection of funds’ data. https://www.esma.europa.eu/sites/default/files/2025-06/ESMA12-2121844265-4904_DP_on_integrated_reporting.pdf

- European Securities and Markets Authority. (2025, April 24). Annual risk assessment of leveraged AIFs in the EU – 2024. https://www.esma.europa.eu/sites/default/files/2025-04/ESMA50-524821-3642_Annual_risk_assessment_of_leveraged_AIFs_in_the_EU_-_2024.pdf

- Bouveret, A., Ferrari, M., Grill, M., Molestina Vivar, L., Schmidt, D. J., & Weistroffer, C. (2025, January 15). Leveraged investment funds: A framework for assessing risks and designing policies. European Central Bank, Macroprudential Bulletin, 26. https://www.ecb.europa.eu/press/financial-stability-publications/macroprudential-bulletin/html/ecb.mpbu202501_02~1955080e3a.en.html

- Bouveret, A. (2025). Containing risks posed by leverage in alternative investment funds (Occasional Paper Series No. 28). European Systemic Risk Board. https://www.esrb.europa.eu/pub/pdf/occasional/esrb.op28~496399501a.en.pdf

- European Securities and Markets Authority. (2025). AIFMD reporting IT technical guidance (rev 6) [updated]. https://www.esma.europa.eu/document/aifmd-reporting-it-technical-guidance-rev-6-updated

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

Scaling Private Credit Without Scaling Risk: The Role of Institutional-Grade Agency

As private credit platforms scale, operational complexity increases across lender coordination, governance, reporting, and execution. Institutional-grade agency infrastructure helps managers maintain consistency, control, and operational resilience as platforms expand.

Joanna Anderson

Managing Director, Agency Services, Alter Domus

Scale changes the operational equation

Private credit platforms are operating at materially greater scale than they were just a few years ago.