Analysis

Navigating Credit Vulnerabilities in the U.S. Auto Loan Sector

We explore how financial institutions can move beyond backward-looking risk management by adopting forward-looking CECL frameworks, multi scenario stress testing, and portfolio analytics to proactively identify emerging credit risks.

The U.S. auto loan market has undergone structural shifts that are reshaping credit risk. Post-COVID vehicle price increases have driven loan balances significantly higher, while extended terms—increasingly exceeding 72 months—mask affordability challenges. Simultaneously, widespread negative equity from trade-ins has pushed loan-to-value ratios above 100% at origination, with monthly payments frequently surpassing $1,000.

These compounding dynamics intensify credit risk in recent loan vintages, requiring financial institutions to move beyond backward-looking risk management toward forward-looking analytical frameworks consistent with CECL assumptions that identify vulnerabilities before losses materialize. Alter Domus’ integrated platform combines CECL compliance, multi-scenario stress testing, and real-time portfolio analytics to enable institutions to proactively identify and monitor loans exhibiting multiple risk characteristics.

Quantifying the Risk: Key Market Vulnerabilities

The auto loan market has evolved during the post-COVID period in ways that compound several key credit risk factors, leaving lender’s portfolios vulnerable to potential economic downturns.

- New vehicle prices have increased more than 30% since 2019, reaching an average of almost $49,000 in 2025.

- Average loan repayment terms have lengthened, with a growing percentage exceeding 72 months or more to cope with payment shock.

- Monthly loan payment amounts have increased, averaging $773, while payments exceeding $1,000 have reached an all-time high of 20.3% of the market.

- Around 30% of trade-ins now carry negative equity, averaging $7,214, a byproduct of slower equity buildup due to extended loan terms.

- This has led to LTV ratios often exceeding 100% at origination, leaving borrowers vulnerable to declining used vehicle values or deteriorating personal finances.

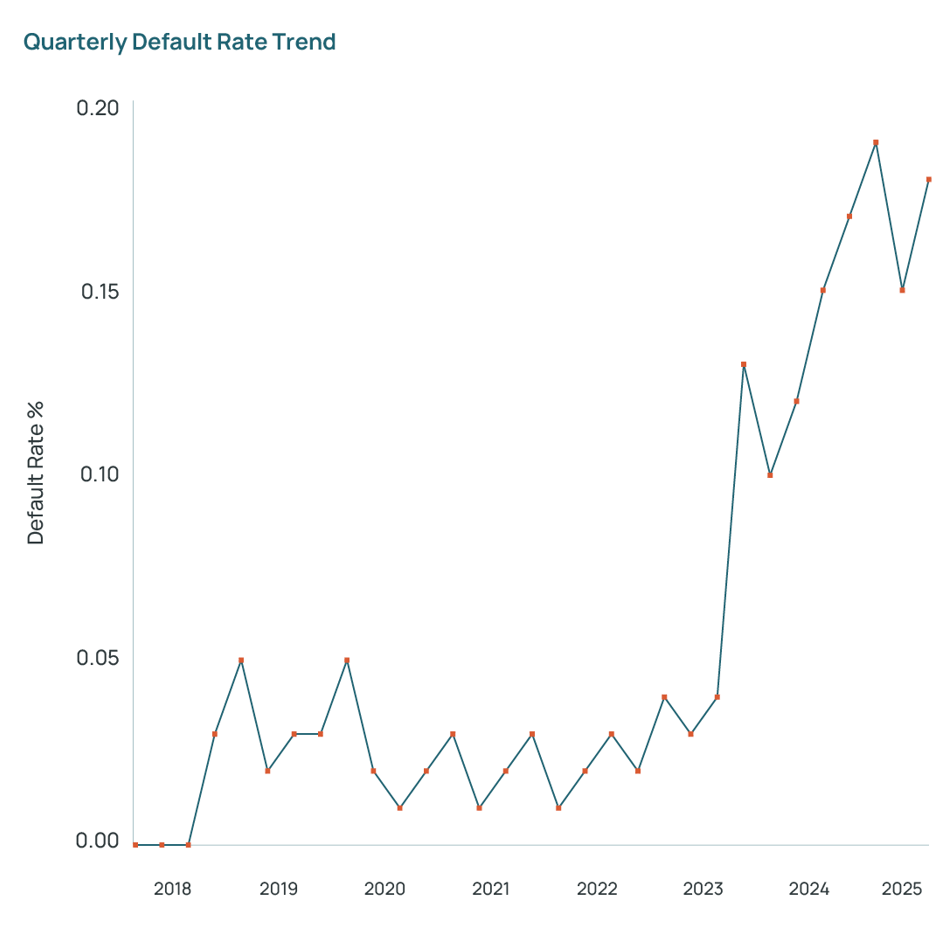

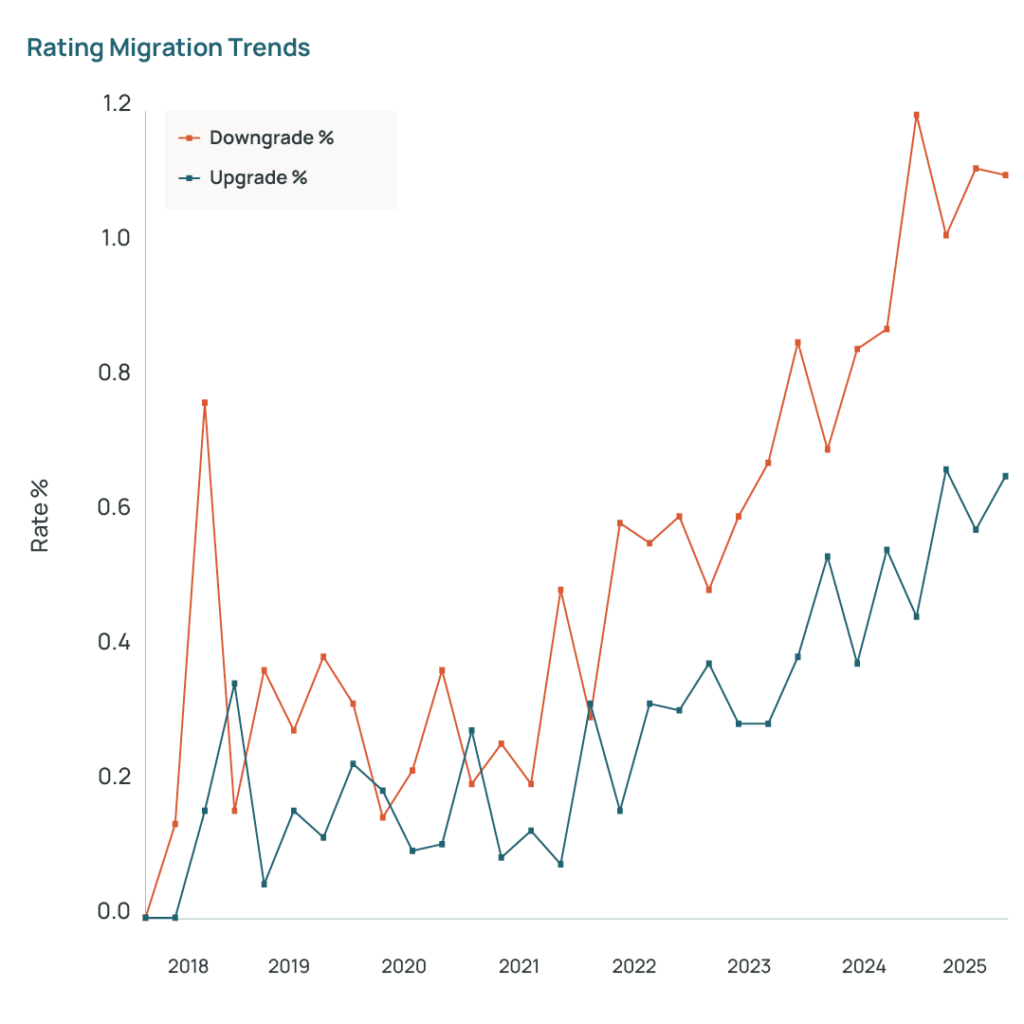

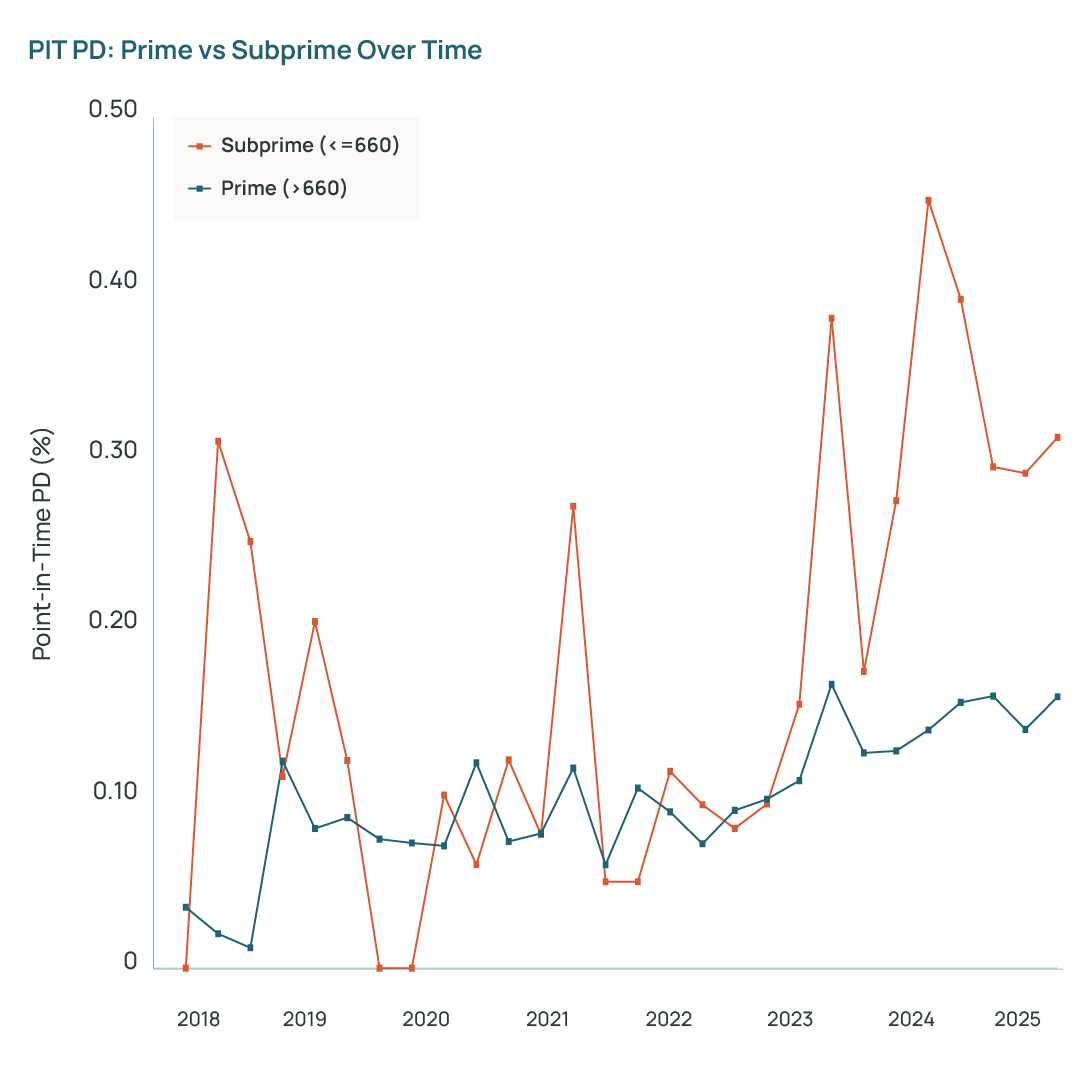

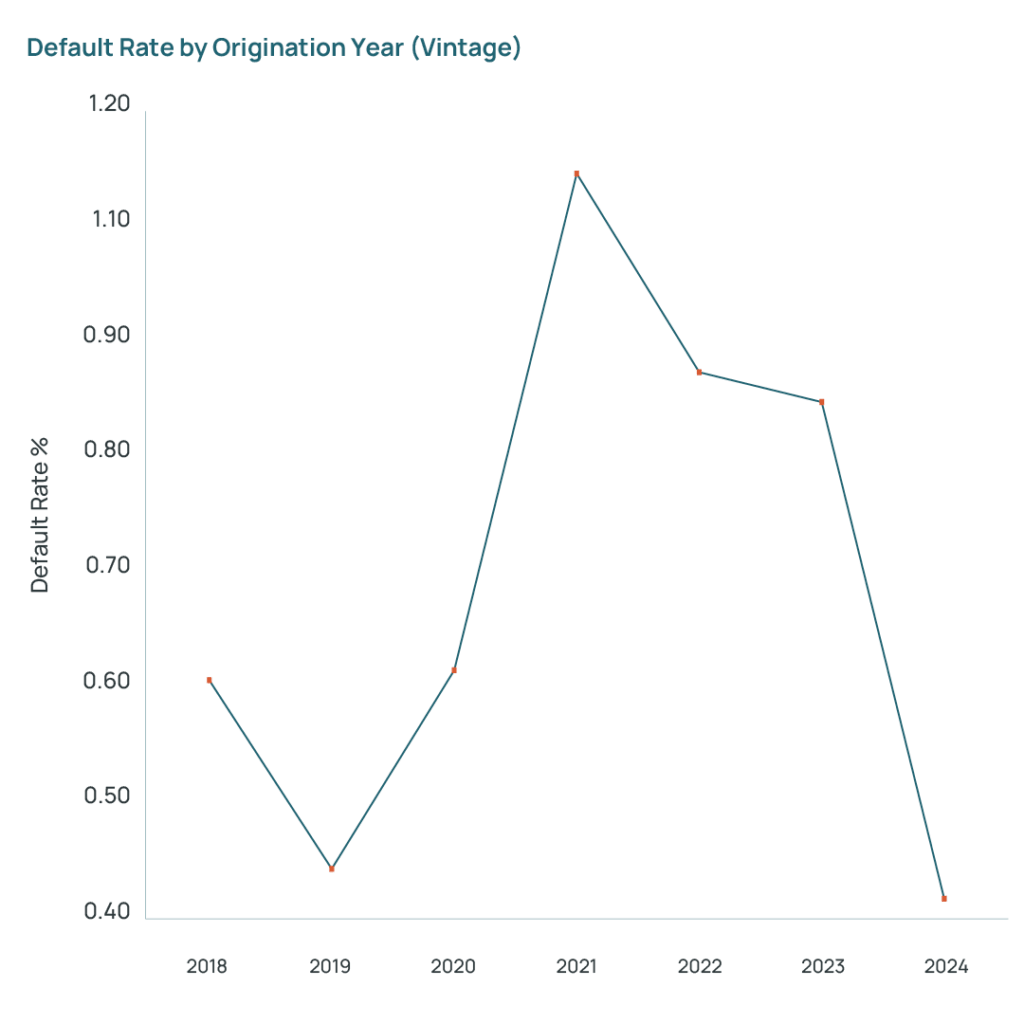

Credit risk indicators from 2021-2024 loan vintages are beginning to show stress patterns compared to pre-pandemic performance. Analysis of auto loan portfolios from AD’s consortium database reveals additional evidence of these stress indicators as demonstrated in the accompanying exhibits, yielding several key observations.

- Exhibit 1 demonstrates an upward trajectory in default rates during recent years, while Exhibit 2 reveals an increasing ratio of credit quality deterioration relative to improvement through delinquency rate migration patterns, indicating heightened underlying credit risk.

- Exhibit 3 reveals a pronounced differentiation in performance between prime and subprime borrower segments.

- Exhibit 4 illustrates a significant increase in default rates for the 2021 vintage, whereas the performance trajectory of the 2024 vintage remains to be determined over time.

- Loans that turn delinquent often do not experience their first delinquency until years two or three.

- Although delinquency rates remain low relative to the GFC, the elevated risk factors above suggest that these cohorts may underperform relative to historical norms.

Financial institutions need to be alert to these warning signs and adopt a proactive risk management posture before losses materialize.

Leveraging Forward-Looking CECL-based Data

Financial institutions should leverage high-quality CECL-compliant loan-level data that captures borrower payment behavior, underlying collateral values, and unique borrower and loan characteristics to discover unrealized, embedded risk in their portfolios. Using CECL-grade data and assumptions also represents an aligned view of credit risk across the organization.

The value of using CECL-grade data is its forecasting power for analyzing correlations between delinquency patterns and key macroeconomic variables.

- A dynamic CECL-based stress testing approach can identify portfolio vulnerabilities sensitive due to recessionary macroeconomic scenarios, collateral value declines, and volatile delinquency migration rates.

- These insights enable proactive risk management rather than reactive loss mitigation.

Methods for Proactive Risk Management

Granular Portfolio Segmentation

Auto loan portfolios with granular, layered segmentation – rather than relying primarily on delinquency bands and credit scores – lead to more effective risk management.

- Portfolios should be further sub-segmented by vintage, loan term length, negative equity status, payment amount, geographic concentration, or borrower debt-to-income ratios.

- This multi-layered view reveals concentration risks and identifies cohorts that are currently performing but carry higher embedded risks.

Applying CECL-based PD models using granular segmentation enables financial institutions to identify loans that are more likely to correlate with future defaults under adverse economic conditions.

Scenario Analysis

Stress testing is an important risk management tool and should be incorporated in active portfolio management.

- By running loan-level PD models across baseline, moderate stress, and severe economic scenarios and looking for payment shock and borrower elasticity, potential defaults and losses can be quantified across segments, identifying areas requiring enhanced surveillance.

- Stress test results can guide adjustments to underwriting criteria during counter-cyclical periods including LTV caps, term restrictions for higher-risk segments or adjusting pricing to reflect true risk-adjusted returns under various economic scenarios.

A CECL-based approach to stress testing reveals portfolio segments exposed to loans with risk factor combinations that exhibit much higher default probabilities in certain recession scenarios.

Data-Driven Strategic Adjustments

Forward-looking analytics inform both portfolio management, underwriting and pricing strategy.

Financial institutions that use consortium or peer loan performance data to benchmark against their own history can validate assumptions and gauge performance against industry peers.

- This insight enables proactive management of segments with delinquency rates significantly exceeding industry benchmarks, which may indicate underwriting weakness.

Technology-Enabled Solutions

Fully integrated technology platforms that seamlessly combine CECL compliance, multi-scenario stress testing, portfolio analytics, and real-time monitoring in a single auditable framework are essential for effective risk management at scale.

- The ALLL+ Platform provides the foundation for CECL compliance and credit loss estimation, featuring integrated scenario management that enables financial institutions to assess portfolio impact under multiple economic forecasts.

- Real-time attribution analysis identifies the specific drivers of allowance changes, while strong governance frameworks ensure full traceability for audit and regulatory examination.

- The Analytics Platform (formerly Risk Modeler) extends these capabilities into strategic portfolio management.

- Its Financial Resilience Assessment combines macro-economic default regression with loan-level risk classifications, while the Model Repository Hub ensures consistency and version control across all analytical frameworks.

- The Portfolio Monitoring Dashboard provides real-time visibility into key metrics, enabling rapid response to emerging trends.

- Advanced modeling capabilities incorporating machine learning can identify complex patterns and correlations that traditional approaches might miss.

When CECL compliance, stress testing, and portfolio analytics share a common data infrastructure, financial institutions gain insight into embedded risk throughout any portfolio.

Conclusion

Post-COVID structural shifts in the U.S. auto loan market—elevated balances, extended terms, and negative equity, demand forward-looking risk management that anticipates vulnerabilities before losses occur. Granular segmentation that looks at vintage, loan term, payment amount and equity status, combined with integrated CECL and portfolio stress testing gives banks a forward-looking view of risk by revealing how specific collateral layers perform under changing economic conditions.

AlterDomus’ CECL-integrated ALLL+ and Analytics Platforms transform compliance infrastructure into strategic advantage through multi-scenario stress testing and real-time portfolio analytics. Financial institutions that deploy these capabilities will identify emerging risks early and respond with precision in an evolving credit risk landscape.

To learn more about Alter Domus’ integrated risk management solutions, contact [email protected].

Get in touch with our team today

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields