Analysis

As credit markets become increasingly complex, we examine how loan-level stress testing provides the insight needed to anticipate losses, validate assumptions, and strengthen portfolio resilience.

In today’s volatile financial landscape, the ability to anticipate and navigate potential economic downturns is not just a strategic advantage it’s a necessity for financial institutions. As credit portfolios become increasingly complex and economic uncertainty persists, stakeholders must prioritize the implementation of sophisticated stress testing frameworks that deliver accurate, actionable insights into portfolio vulnerabilities and capital adequacy.

By adopting a loan-level stress testing approach that integrates directly with CECL-based frameworks, institutions can gain invaluable insights into their credit portfolios, enabling them to identify vulnerabilities, optimize capital allocations, and enhance strategic decision-making.

Traditional portfolio-level stress testing approaches often rely on broad approximations and static assumptions that fail to capture the nuanced dynamics of credit risk migration. These methods treat portfolios as homogeneous blocks, applying uniform stress factors across diverse loan types, borrower profiles, and risk characteristics. Such approaches may provide directional guidance but lack the granularity necessary for precise capital planning and robust risk management.

A loan-level stress testing framework addresses these limitations by applying stress directly to individual borrower financial indicators, such as debt service coverage ratios (DSCR), net operating income (NOI), revenue trends, FICO scores, and small business risk indicator (SBRI) scores. This granular approach recognizes that borrower behavior and credit portfolio performance demonstrate heightened sensitivity to hypothetical economic scenarios that are unique to each institution.

By stressing these loan-level variables and predicting subsequent credit rating movements, institutions can forecast the resulting impacts on CECL allowances, provisions, net charge-offs (NCOs), and capital with remarkable accuracy.

One of the most compelling advantages of a sophisticated loan-level stress testing framework is its seamless integration with existing CECL infrastructure. While CECL estimates reflect expected losses under baseline or reasonably supportable forecasts, stress testing extends this analysis to more adverse economic scenarios. The integration of both frameworks enables a comprehensive assessment of portfolio risk and capital adequacy.

By feeding predicted loan-level risk rating changes directly into an institution’s CECL exposure at default (EAD) model, the framework produces accurate impacts on allowances, earnings and capital. This approach leverages the actual CECL-based cash flow model with its detailed payment and risk characteristics—including contractual amortization terms, funded and unfunded amounts, default probabilities, loss given default assumptions, and prepayment rate curves—to deliver period-by-period forecasts over the specified horizon.

This methodology represents a substantial improvement over approximations, particularly because the progression of credit losses is path-dependent and rarely follows a linear pattern. The framework captures the dynamic interplay between portfolio runoff, new loan originations, risk rating migrations, and loss realization timing—factors that static models cannot adequately address.

The technical foundation of modern loan-level stress testing frameworks combines quantitative rigor with qualitative judgment through advanced machine learning techniques. Predictive models, including Decision Tree, Histogram Gradient Boosting, and Random Forest Classifiers, are trained on historical credit data to identify patterns in rating migrations under various stress conditions.

A key methodological innovation involves developing separate upgrade and downgrade models for each portfolio segment to address class imbalance issues where downgrades historically outnumber upgrades. These models utilize sophisticated performance metrics like F1 scores rather than simple accuracy, employ class weights to balance predictions, and incorporate ordinal classifiers with monotonic features to ensure logical stress responses.

This approach ensures that as borrower financial metrics deteriorate under stress, predicted rating downgrades increase proportionally—a critical validation step that enhances model credibility and regulatory acceptance.

The framework typically segments portfolios based on loan characteristics and data availability, for instance, large commercial real estate loans may be modeled using detailed financial statement variables, while consumer loans rely more heavily on credit scores and payment behavior. This segmentation enables each model to leverage the most predictive variables for its respective borrower population.

Perhaps the most significant value proposition of a loan-level stress testing framework is its ability to produce comprehensive multi-period projections rather than single-period snapshots. By incorporating roll-forward functionality with realistic loan growth assumptions, the framework dynamically updates the portfolio composition at each period throughout the forecast horizon, typically on a quarterly basis over one or more years.

This capability enables institutions to assess not only the initial shock from adverse conditions but also the cumulative impacts as stress persists and portfolio composition evolves. The framework produces forecasts of expected losses, provisions, NCOs, and capital ratios across the planning horizon, supporting both risk management and internal strategic planning initiatives. Institutions can evaluate their degree of compliance with relevant capital ratio thresholds—such as minimum Common Equity Tier 1, Tier 1, and Total risk-based ratios—while weighing the likelihood of various scenarios.

These frameworks are most effective when supported by fully integrated technology platforms that unify CECL compliance, multi-scenario stress testing, and portfolio analytics within a single auditable infrastructure. Alter Domus’ ALLL+ Platform delivers CECL compliance and credit loss estimation with integrated scenario management, real-time attribution analysis, and governance capabilities ensuring full audit traceability, while the Analytics Platform (formerly Risk Modeler) extends this into strategic portfolio management through macroeconomic default regression, loan-level risk classification, and real-time portfolio monitoring.

When these capabilities share a common data infrastructure, institutions gain a materially clearer view of embedded portfolio risk. Advanced machine learning further enhances this visibility by surfacing complex patterns that traditional approaches overlook, translating analytical rigor into more informed decisions around capital allocation, underwriting, and strategic planning.

The risks associated with credit portfolios are multifaceted and can vary significantly across institutions, influenced by factors such as borrower behavior, market conditions, and organizational objectives. Credit portfolio compositions differ across financial institutions based on strategic objectives, risk appetite, expertise, geographic presence, and organizational mission. Consequently, both borrower behavior and portfolio performance may demonstrate unique sensitivities to economic scenarios, making tailored stress testing essential, a necessity further reinforced by OCC guidance.

Regular and rigorous stress testing through a sophisticated loan-level framework serves as a cornerstone of sound risk management. It helps institutions identify vulnerabilities within portfolios—particularly those arising from excessive concentrations in specific borrowers, industries, geographic regions, or product types. This proactive approach not only safeguards against potential losses but also positions institutions to make informed strategic decisions regarding underwriting standards, credit policy refinements, and capital allocation optimization.

In an uncertain economic environment, institutions that embrace advanced loan-level stress testing frameworks will be better positioned to navigate challenges and thrive.

To learn more about AlterDomus’ integrated risk management solutions, contact [email protected].

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

In the first part of its Real State of Real Estate series, Alter Domus explored why specialist real estate investment strategies are supplanting traditional, generalist models.

In the second instalment in the series, Alter Domus examines the practical implications of what the trend towards specialization means for real estate managers, and how firms are evolving their operational models to keep pace with the growing complexity inherent in managing multi-strategy real estate platforms.

Michael Gregori

Head of Real Estate, North America

Melanie Collett

Head of Real Estate, EMEA

The real estate investment model is in a period of significant transformation. To remain competitive and effective, managers must evolve their operational models in step with the demands of an increasingly complex landscape.

Twenty years ago, real estate portfolio construction was a relatively simple exercise. Office assets accounted for the bulk of portfolio composition, topped up with a mix of other familiar real estate categories, such as retail and residential.

Pandemic lockdowns and the recent cycle of rising interest rates have changed that. Office share of real estate portfolios is around a third of what it used to be in 2008, according to Blackrock. McKinsey, meanwhile, notes that deliberate asset selection has replaced broad-based real estate exposure as the primary driver of returns performance.

The traditional real estate asset verticals of office and retail still have a role to play, but data centers, life sciences, storage, senior living, and myriad other real estate sub-sectors are now essential for driving real estate returns. Investor preference isn’t only specializing by type of asset, but also investment strategy. Core and core-plus investment strategies target IRRs in the mid-single digits to low teens. Value-add and opportunistic strategies carry greater risk, but target higher returns in the upper teens.

Investors are also broadening allocations beyond real estate equity plays into real estate credit and real estate asset-based finance (ABF) to fine-tune portfolios in line with specific risk-adjusted returns targets.

Today’s institutional platforms routinely span multiple specialist sectors and jurisdictions, and the portfolios they manage demand fund structures that are equally sophisticated and fit for purpose.

McKinsey notes that creative capital structuring at the asset and fund level can serve as drivers of real estate outperformance. NAV loans, continuation vehicles, structured secondaries and hybrid capital structures offer the flexibility to extend hold periods, bridge liquidity gaps and reposition portfolios.

Private real estate is also tracking the wider trend across private markets of managers running a broader spread of fund structures.

GPs are offering a wider range of fund structures, separately managed accounts, co-investment funds and evergreen investment vehicles. These structures address the specific requirements of institutional investors, and facilitate access for non-institutional investors to private real estate strategies.

The transition toward specialist investment strategies in real estate, and the structural flexibility required to support it, is adding meaningful layers of operational complexity for firms across the industry.

Fund accounting teams are under mounting pressure to manage a growing number of fund structures, investment strategies and global jurisdictions. As portfolio breadth increases, maintaining consistency across multiple strategies and structures becomes considerably more challenging, and the consequences of reporting errors and delays grow more significant.

Investment strategy complexity is adding operational burden for real estate back-office teams. This compounds when combined with increasing demands for LP reporting and transparency.

In all private market strategies, asset-level transparency and portfolio aggregation are becoming table stakes. LPs want to see granular, real-time data on asset performance that facilitates forward-looking decision-making, rather than retrospective, reactive portfolio management.

For a time, real estate managers were able to absorb increasing workloads by stretching legacy systems and processes, but that approach has reached its limits. As fund structures continue to proliferate, manual reconciliations become unmanageable, and the risks of reporting errors and data fragmentation escalate, making a fundamental step change in operational models not just desirable, but necessary.

Upgrading real estate models is essential. Data has to be standardized, and automation and AI leveraged to manage operational complexity.

LPs, across all private markets strategies, are adapting manager selection decisions accordingly. Reporting and accounting teams are no longer simply cost centers, but key enablers of competent portfolio stewardship and headline returns.

Managers with the capability to track valuations at both the asset and portfolio level, and to benchmark performance consistently across real estate strategies, hold a meaningful competitive advantage. Operational capability is far more than a compliance requirement; it is a reliable predictor of long-term performance success.

Building up real estate investment platforms to scale is one of the ways managers are addressing the complexity challenge. When firms reach a certain size, investment in technology, data and AI can be spread more evenly across multiple strategies and funds, unlocking economies of scale.

For mid-market players, however, ramping up platform size is not the only pathway to achieving the back-office economies of scale available to larger counterparts.

Specialization is valued in today’s market, and managers operating in lucrative industry niches will not want to trade off distinctive front office capability for back-office scale.

Partnering with a specialist third-party fund administrator allows independent real estate firms to access the geographic reach and technological capabilities of a large-scale platform, without the burden of significant upfront capital expenditure, or the need to relinquish independence by merging into a larger manager.

Alter Domus serves more than 400 real estate clients worldwide, administering US$380 billion in real estate assets across 1,250 real estate funds and separate accounts.

With a deep real estate client base and a global presence in 24 jurisdictions, Alter Domus brings both the geographic reach and asset-specific technical expertise that modern real estate managers demand. Our Integrated Global Real Estate Solution (IGRES) brings this together, layering advanced technology across a fully integrated, end-to-end administration service, from the asset level through to investors.

Integrated operating environments like IGRES are designed to consolidate property-level and fund-level accounting, consolidation, investor reporting, debt administration and data integration into one reporting architecture.

This unified operating environment marks a significant departure from the back-office models that have historically definedreal estate administration. Where property managers and fund accountants once operated across disconnected systems, SPVs were tracked in isolation, and investor reporting was produced manually, a more integrated and efficient approach is now possible.

Fragmented back-office services can handle smaller, simpler portfolios, but begin to fracture as portfolios become larger and more specialized.

An integrated stack addresses this risk and empowers managers to handle higher workloads and complexity without data splitting and operational burden escalating.

The real estate asset class is specializing rapidly, and operational infrastructure is emerging as a defining competitive advantage.

Specialization introduces layers of structural complexity that legacy operating models are simply not equipped to support and technology stacks assembled informally over time cannot deliver at scale.

The firms best positioned to succeed will be those that pair deep sector expertise with integrated operating models capable of delivering centralized reporting and institutional-grade transparency across even the most complex portfolios.

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

We explore how financial institutions can move beyond backward-looking risk management by adopting forward-looking CECL frameworks, multi scenario stress testing, and portfolio analytics to proactively identify emerging credit risks.

The U.S. auto loan market has undergone structural shifts that are reshaping credit risk. Post-COVID vehicle price increases have driven loan balances significantly higher, while extended terms—increasingly exceeding 72 months—mask affordability challenges. Simultaneously, widespread negative equity from trade-ins has pushed loan-to-value ratios above 100% at origination, with monthly payments frequently surpassing $1,000.

These compounding dynamics intensify credit risk in recent loan vintages, requiring financial institutions to move beyond backward-looking risk management toward forward-looking analytical frameworks consistent with CECL assumptions that identify vulnerabilities before losses materialize. Alter Domus’ integrated platform combines CECL compliance, multi-scenario stress testing, and real-time portfolio analytics to enable institutions to proactively identify and monitor loans exhibiting multiple risk characteristics.

The auto loan market has evolved during the post-COVID period in ways that compound several key credit risk factors, leaving lender’s portfolios vulnerable to potential economic downturns.

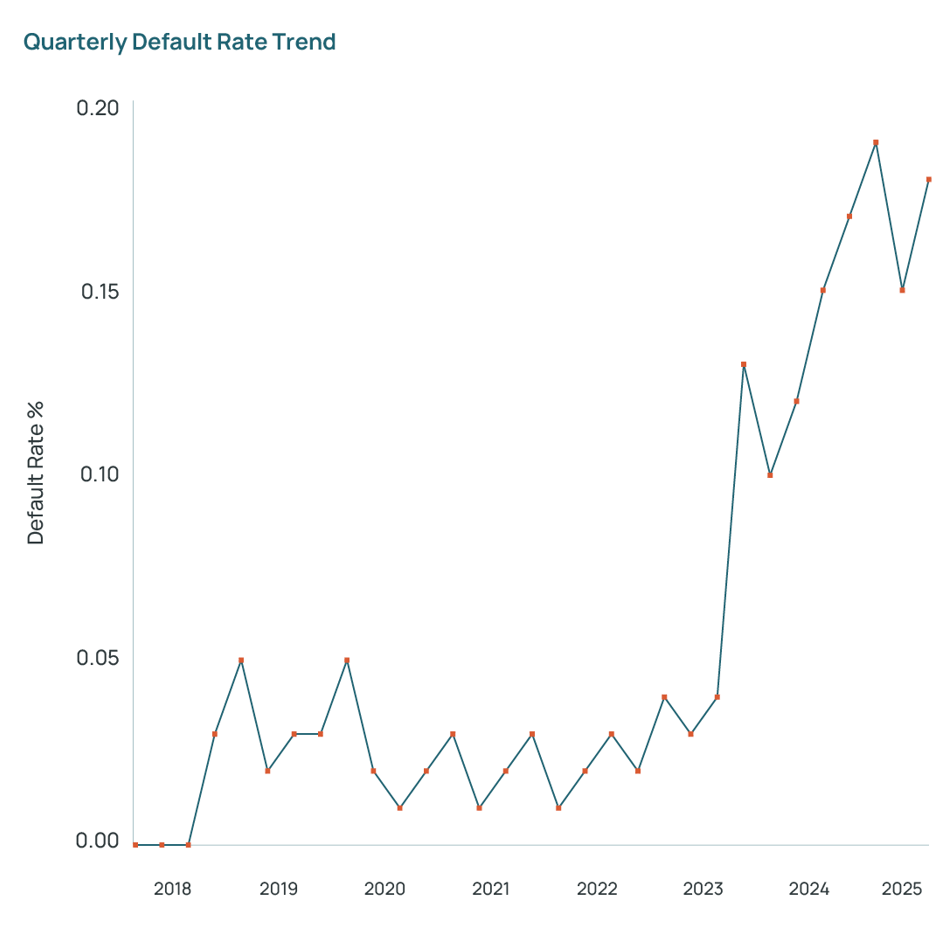

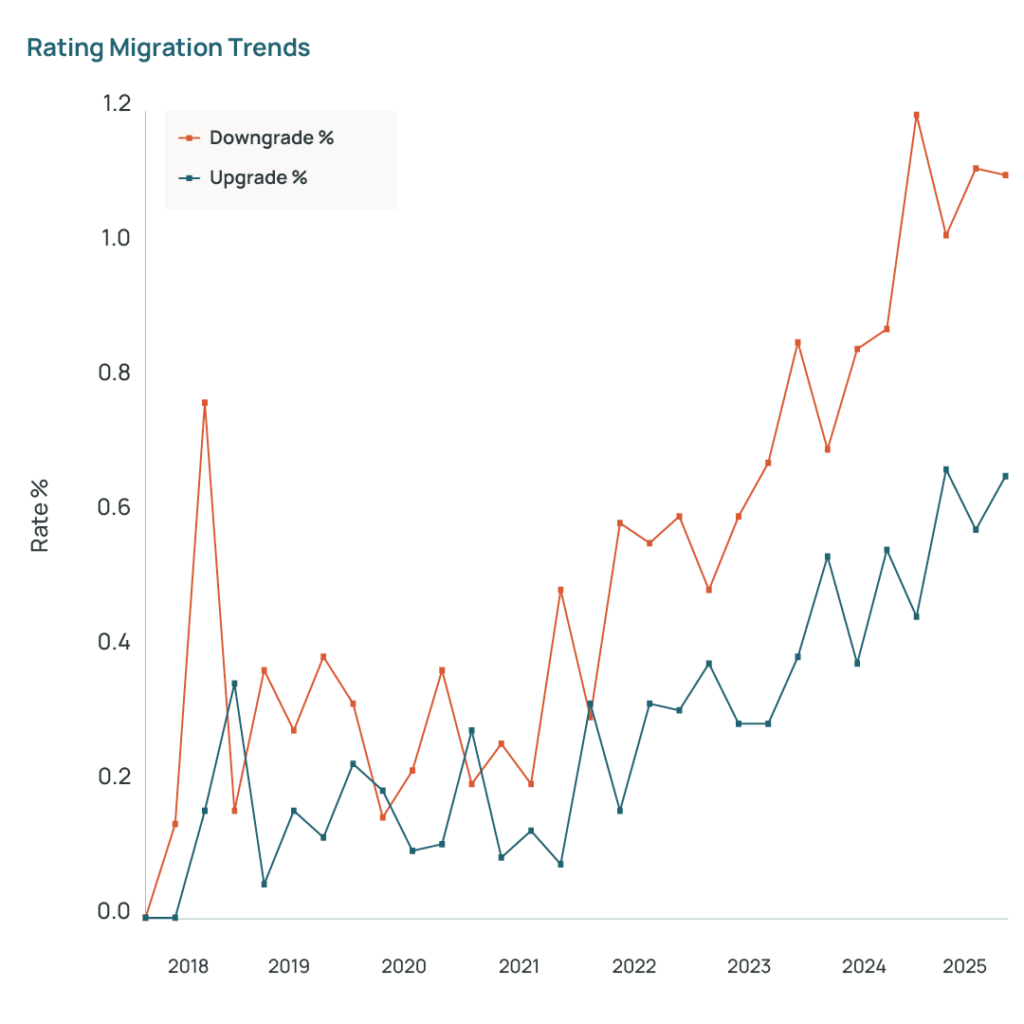

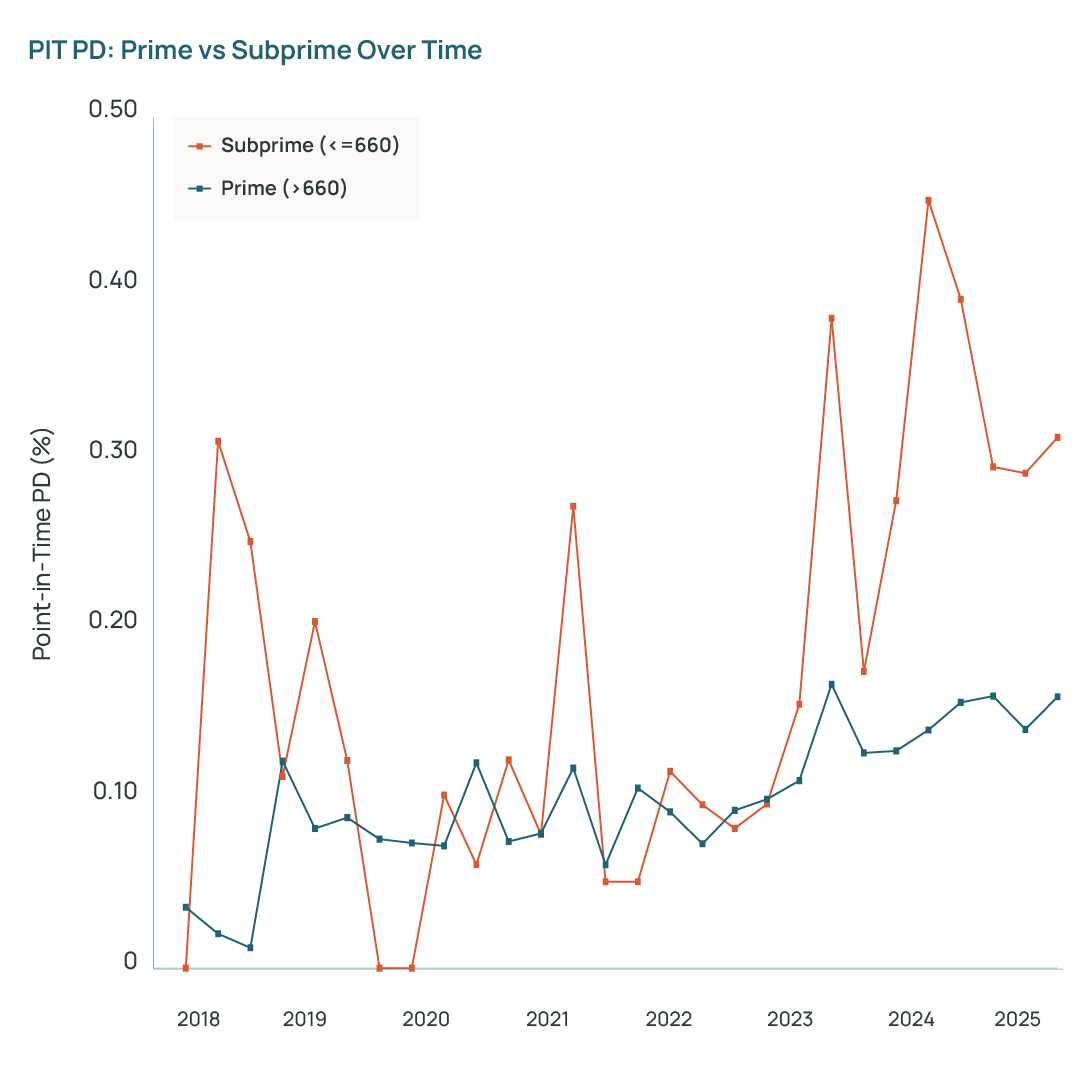

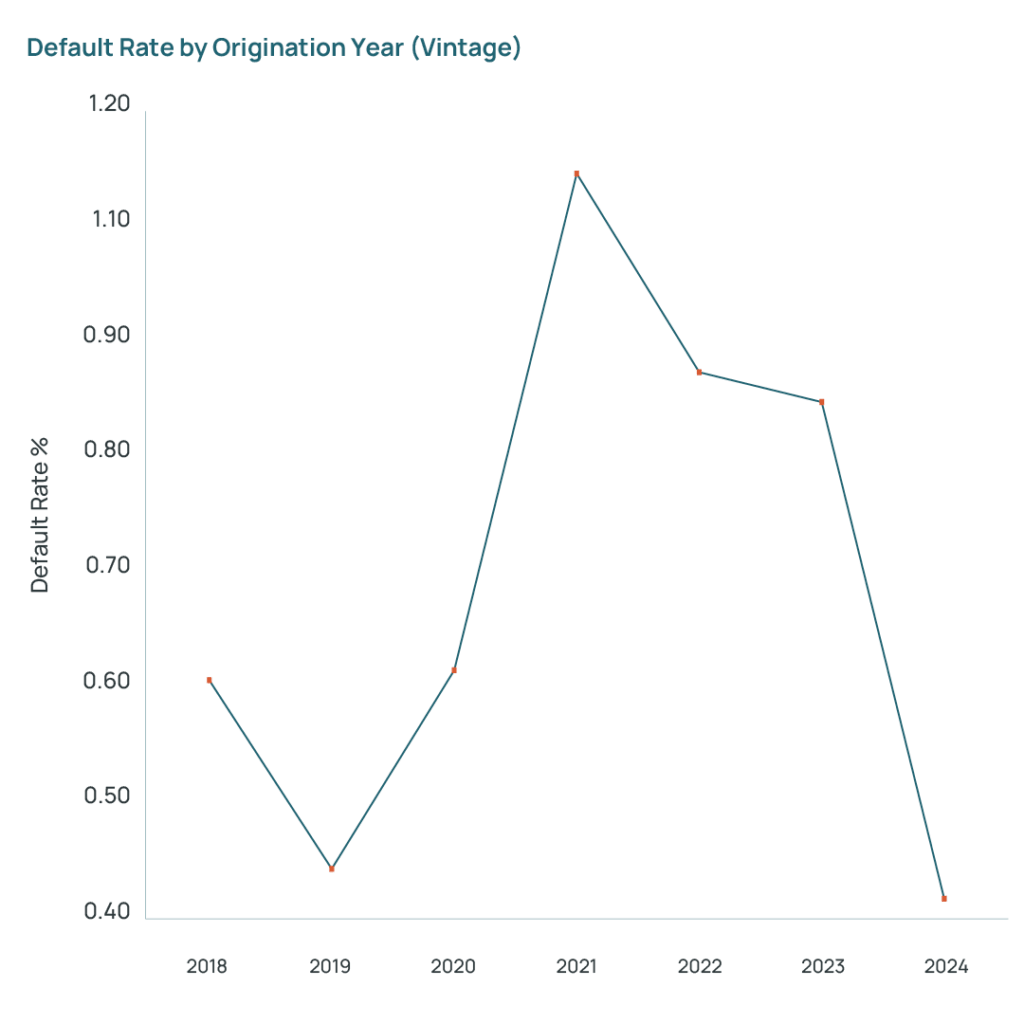

Credit risk indicators from 2021-2024 loan vintages are beginning to show stress patterns compared to pre-pandemic performance. Analysis of auto loan portfolios from AD’s consortium database reveals additional evidence of these stress indicators as demonstrated in the accompanying exhibits, yielding several key observations.

Financial institutions need to be alert to these warning signs and adopt a proactive risk management posture before losses materialize.

Financial institutions should leverage high-quality CECL-compliant loan-level data that captures borrower payment behavior, underlying collateral values, and unique borrower and loan characteristics to discover unrealized, embedded risk in their portfolios. Using CECL-grade data and assumptions also represents an aligned view of credit risk across the organization.

The value of using CECL-grade data is its forecasting power for analyzing correlations between delinquency patterns and key macroeconomic variables.

Granular Portfolio Segmentation

Auto loan portfolios with granular, layered segmentation – rather than relying primarily on delinquency bands and credit scores – lead to more effective risk management.

Applying CECL-based PD models using granular segmentation enables financial institutions to identify loans that are more likely to correlate with future defaults under adverse economic conditions.

Scenario Analysis

Stress testing is an important risk management tool and should be incorporated in active portfolio management.

A CECL-based approach to stress testing reveals portfolio segments exposed to loans with risk factor combinations that exhibit much higher default probabilities in certain recession scenarios.

Data-Driven Strategic Adjustments

Forward-looking analytics inform both portfolio management, underwriting and pricing strategy.

Financial institutions that use consortium or peer loan performance data to benchmark against their own history can validate assumptions and gauge performance against industry peers.

Fully integrated technology platforms that seamlessly combine CECL compliance, multi-scenario stress testing, portfolio analytics, and real-time monitoring in a single auditable framework are essential for effective risk management at scale.

When CECL compliance, stress testing, and portfolio analytics share a common data infrastructure, financial institutions gain insight into embedded risk throughout any portfolio.

Post-COVID structural shifts in the U.S. auto loan market—elevated balances, extended terms, and negative equity, demand forward-looking risk management that anticipates vulnerabilities before losses occur. Granular segmentation that looks at vintage, loan term, payment amount and equity status, combined with integrated CECL and portfolio stress testing gives banks a forward-looking view of risk by revealing how specific collateral layers perform under changing economic conditions.

AlterDomus’ CECL-integrated ALLL+ and Analytics Platforms transform compliance infrastructure into strategic advantage through multi-scenario stress testing and real-time portfolio analytics. Financial institutions that deploy these capabilities will identify emerging risks early and respond with precision in an evolving credit risk landscape.

To learn more about Alter Domus’ integrated risk management solutions, contact [email protected].

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

As the first half of 2026 comes to a close, private markets continue to navigate a complex landscape shaped by shifting macroeconomic conditions, evolving investor priorities, and growing demand for operational efficiency. This review examines the key trends that defined private equity, infrastructure, real estate, and private debt during H1 2026.

Private equity H1 highlights

Elliott Brown

Global Head of Private Equity

Private equity firms started 2026 hoping to accelerate distributions and kick-start fundraising. Six months on, private equity firms are hoping to accelerate distributions and reignite fundraising.

This is not where private equity firms expected to find themselves halfway through another year.

Dealmakers began 2026 in a positive frame of mind. Global deal value hit US$4.5 trillion in 2025, the second-best year on record, according to figures from the London Stock Exchange Group. Inflation had peaked and interest rates were coming down. After years of tepid M&A and false starts, there was every reason for optimism that 2026 would finally be the year that the PE industry shifted back into gear.

But in a pattern that has become all too familiar for GPs, geopolitical shocks and macro-economic disruption put a long-awaited revival on hold. Again.

In February, the release of a new AI tool wiped US$300 billion of the value of software stocks amid fears that AI agents would replace traditional software-as-a-service (SaaS) tools.

The “SaaS-pocalypse” knocked private equity confidence hard.

Software has been a sector favorite for buyout firms, accounting for around 14% of US PE deal value during the last decade, according to Pitchbook. In 2025, almost one in every five dollars GPs invested was in a software company. At the end of March, private equity software valuations were down 8%, according to MSCI figures analyzed by Bain & Co. The drop was less pronounced than in public markets, but enough to sting.

Just a few weeks later, GPs had another macro-economic jolt to deal with, as conflict in the Middle East led to the closure of the Strait of Hormuz, a shipping lane used to transport around a fifth of global oil and natural gas energy supply. The conflict saw a subsequent rise in oil prices of 60%, bringing fears of inflation and interest rate hikes back into the frame.

These market tremors undermined confidence just as dealmakers were beginning to anticipate a recovery, and the succession of disruptive events had a direct impact on exits, distributions and fundraising.

Global exit value dropped to US$96 billion in Q1 2026, 34% down on Q4 2025 and the lowest quarter on record for exits since Q1 2024.

A stuttering exit market meant little improvement to distributions, which remained at near record lows, according to Bain & Co. Distributions as a percentage of NAV currently sit at 13.4 %. This compares to an average of 25% between 2010 and 2025.

Stalled distributions have meant ongoing tepid fundraising. Global PE fundraising fell to US$373 billion in Q1 2026, according to KPMG analysis. On a 12-month rolling basis, this marked the lowest level for fundraising since Q1 2017.

With the “new dawn” for deals and distributions once again deferred, GPs have become highly selective and flexible.

High-quality companies have continued to trade at good prices (according to MSCI analysis, 75% of portfolio companies have exited at premiums to NAV marks), despite macro mayhem.

The businesses that have been sold, however, represent a very select group of companies.

Companies with hard assets that provide essential services are a case in point, and have exited successfully to buyers seeking deals that offer protection against AI disruption. Platinum Equity, for example, sold waste management infrastructure company Urbaser to Blackstone and EQT in a US $6.6 billion deal.

The pool of assets that GPs can be sure will sell in M&A processes, however, is a small one, and firms have had to plough other furrows to sustain distribution flow in the absence of clean exits.

GP-led secondary deals, where managers transfer select assets from existing funds into new vehicles, reached a record US$108 billion in 2025, up from US$77 billion in 2024, according to Coller Capital. Momentum has carried into this year, even though LP scrutiny of continuation vehicle (CV) terms and potential conflicts of interest has intensified.

CVs, the predominant GP-led deal structure, are now a proven liquidity mechanism for private equity firms, and have, on the whole, generated decent returns for LPs too. StepStone research shows that 60 percent of assets moved into CVs between 2020 and 2024 generated gross returns in excess of 3x. Only 28 percent of assets in the wider buyout market did the same. Debt markets have also provided liquidity optionality. In 2025, buyout firms in the US borrowed US$94 billion from loan and bond markets to fund payouts. In the absence of exits, dividend recapitalizations continued to generate distributions through the first half of this year, with a number of sponsors executing recaps through the first half, according to Bloomberg reports.

There is no doubt LPs would prefer to see an increase in “clean” exits via IPO or M&A, but in a choppy market where listings and deal processes can be hostage to market gyrations, some liquidity has been better than none.

After a very challenging first half of the year, there are at least some signs of respite for firms as they move into H2 2026.

The software sell-off has run its course, and software stocks have recovered to roughly the same “pre-SaaS-pocalypse” levels.

Software companies still face some disruption to pricing models and will have to switch from subscription fees based on headcounts to charges linked to usage and outcomes, but in the long-term, AI could actually prove a tailwind for software companies.

For software-focused GPs, this has come as a welcome relief, especially for those that have backed industry-focused software that has integrated years of proprietary data and is very difficult to pull out and replace.

The conflict in Iran has also simmered down. Oil prices have receded to levels seen before the conflict escalated, and inflationary pressures have subsided although risks remain.

So, as the macro-economic picture stabilizes, is this the moment when the “wave” of delayed dealmaking finally manifests? GPs have seen this movie before and won’t be banking on it.

What firms will be focusing on is playing to their strengths, priming prized assets for exit, running hard at select assets where they have genuine conviction, and taking opportunities to execute CVs and dividend recaps to return capital to investors.

Firms that execute well in these areas will stand out from the crowd and continue to deliver. A period of stability that extends beyond a quarter or two, however, will not go amiss.

Private credit H1 highlights

Jessica Mead

Global Head of Private Credit

The first half of 2026 has been challenging for all alternative asset classes, but none more so than private credit.

For more than a decade private credit has enjoyed an almost uninterrupted growth surge. Private credit assets under management (AUM) reached US$3.5 trillion at the end of 2025, growing more than 10-fold in around 15 years.

Rapid asset growth has been matched by strong returns. According to Hamilton Lane private credit has been a stellar performer for private markets, with private credit 10-year annualized time-weighted returns handily outperforming leveraged loans and bonds.

Private credit’s momentum, however, was firmly checked in the first half of 2026 as the industry encountered a series of concurrent challenges. The year began with investors increasingly anxious about the quality of private credit underwriting after the high-profile defaults of auto-sector lender Tricolor and car parts business First Brands. Senior bankers warned that private debt’s exposure to these defaults was a red flag, with more distressed credits likely to emerge the year ahead.

Credit quality fears were exacerbated early in 2026 when US$300 billion was wiped off the value of technology stocks following the release of agentic AI tools with the potential to disrupt software-as-a-service (SaaS) business models.

Given that software accounts for more than a fifth of private credit portfolios, according to JP Morgan (rising to around 40% when including broader tech and business services companies), the software valuation reset hit investor confidence in private credit especially hard.

This dip in confidence manifested most prominently in a surge of redemption requests from investors in private credit business development companies (BDCs), publicly traded investment vehicles that allow institutions and individual investors to invest in private credit assets.

Managers operating some of the biggest private credit BDCs faced huge redemption requests – ranging from 20% to 41% – forcing managers to either sell assets to meet surging redemption requests, or gate funds and cap quarterly redemption requests. According to the FT, wealthy investors put in requests to withdraw more than US$20 billion from the biggest private credit funds in Q1 2026.

More sizeable withdrawal requests are expected in the second quarter too, as fears about AI disruption and portfolio credit quality persist. The persistent negative mood around BDCs has seen the S&P BDC post negative one-year returns of 22.94%.

Faced with multi-billion-dollar redemption requests, doubts around underwriting quality, and exposure to AI disruption, private credit has been under severe pressure so far in 2026.

Constant bleak headlines about the asset class’s prospects, however, have obscured the reality of its resilience. Private credit has undoubtedly frayed at the edges in recent months, but it hasn’t cracked, even though the prevailing narrative around asset class has suggested otherwise.

Trailing twelve-month default rates for direct lending, for example, only registered 1.5% at the end of January, superior to leveraged loans (3.7%) and high yield bonds (2%), according to KBRA. Direct lending implied recovery rates and average loss given defaults also outperformed leveraged loans and bonds. KBRA analysis also highlighted the quality of existing portfolios, with median interest coverage ratios (a measure for how easily borrowers can pay debt interest) improving from 1.5% to 1.6% in Q1 2026.

These datapoints indicated that general assumptions about poor underwriting across all private debt portfolios have been overblown. Pockets of risk and distress have been uncovered in some segments of the market, but on the whole private credit has held up well.

Further evidence for the quality of private credit portfolios has been highlighted (of all places) in the BDC market, where managers have sold loans to meet redemptions without having to swallow discounts to trade the assets.

For example, direct lending assets that were sold by managers to meet redemption requests in early 2026 generally traded at or close to par value, indicating that institutional buyers retained confidence in the underlying quality of the loans. These transactions suggest that concerns about widespread underwriting weakness may be overstated, as sophisticated investors have continued to acquire private credit assets at only modest discounts.

The gap between redemption requests and the liquidity managers are able to unlock to meet those requests is more a reflection of private credit’s inherent illiquidity rather than the underlying credit quality.

Hightower Advisers highlights that unwinding illiquid private loans involves time and cost, leaving managers having to find a delicate balance between meeting redemption requests and maintaining portfolio integrity for existing investors.

There is no value in selling down large portions of portfolios at a low point in the cycle, and the expectation is that managers will move to spread redemptions out over time to balance investor requests for liquidity with taking time to hold assets through a volatile cycle and protect portfolio value.

This could see redemption requests remain a feature of the market for several quarters as they work through the system.

Looking ahead to the rest of the year and into 2027, private credit not nearly as stressed as press coverage has suggested.

Portfolios are holding up impressively in a highly challenging and complex market. Private credit also continues to outshine other fixed income asset classes. Yields to maturity for newly issued direct lending deals are sitting at around 9.3% according to JP Morgan figures, versus 7.7% for syndicated loans and 6.9% for high yield bonds.

Private credit also remains well capitalized. Inflows into publicly traded private credit BDCs are expected to slow as first-half market disruption washes through the system, but institutional appetite for private credit funds is as strong as ever, with first quarter closed-end private credit fundraising reaching a record high of close to US$100 billion, according to Private Debt Investor.

Private credit has had more than its fair share of challenges in 2026, but even through this tough period the asset class has shown that resilience across cycles remains is defining feature.

Real estate H1 highlights

Maximilian Dambax

Global Head of Real Assets

Real estate investors began 2026 in an optimistic mood, expecting to build on momentum from the second half of 2025 when select markets showed encouraging signs of recovery.

The Iran conflict cast a shadow over building optimism, as rising oil prices increased the chances of inflation and interest rate hikes, with potentially negative impacts on property valuations.

Real estate investors and dealmakers, however, have responded to another round of geopolitical dislocation with relative calm.

Direct real estate deal value reached US$216 billion in Q1 2026, up 18% year-on-year, according to JLL figures. Cross-border deal activity accounted for US$55 billion of this total, the best quarter for international real estate transaction volumes since 2022, highlighting the resilience of real estate deal flow.

Real estate fundraising proved more challenging, falling 50% year-on-year in Q1 2026 to US$43.96 billion, according to PERE figures.

First quarter numbers for 2026, however, were up against tough Q1 2025 comparables, when two mega-fundraises by Blackstone and Brookfield alone contributed US$35.5 billion of the Q1 2025 total. When figures are adjusted to take account of these outlier closes, the drop in Q1 2026 fundraising narrows. The first three months of 2026 have also surpassed 2023 and 2024 Q1 totals, signaling an improving market, despite recent macro disruption.

Steady deal activity and relatively stable fundraising, however, do not signal a broad-based real estate rally.

The recovery is real, and the asset class is enjoying more stability after navigating compounding headwinds, including the post-pandemic office vacancies, the ongoing displacement of physical retail by e-commerce, geopolitical tariff pressures, and a persistently elevated interest rate environment.

But the rebound is also uneven, and this is fundamentally changing the way investors and managers generate their returns.

Real estate has come through a benign cycle where low interest rates and sustained capital rate compression boosted returns, UBS notes. These tailwinds have now faded, and in the current cycle, performance will be determined by skilled asset selection, informed underwriting, and operational capability.

In today’s evolving market environment, investors and managers can no longer assume that superior asset quality in a prime location will be sufficient to drive long-term returns.

Successful dealmakers will be the ones who can anticipate whether assets can meet the needs of future tenants and adapt to reconfiguring supply chains that prioritize domestic manufacturing, according to UBS.

The importance of evidencing genuine operational real estate capability is already influencing fundraising trends. Value-add strategies (where managers buy underperforming properties and increase value through renovations and operating improvements) accounted for 56% of capital raised in Q1 2026, more than triple the amount raised by the next largest strategy by value, according to PERE. This represents the highest share of value-add fundraising since 2021.

The importance of operational real estate expertise is further underscored by the effect of AI on the real estate sector, both directly, in areas like digital infrastructure, and indirectly in real estate categories like warehousing, logistics and offices.

The most visible impact of AI on real estate is the construction of data centers to run AI technology. JLL estimates that data center capacity will have to double by 2030 to generate the computing power required to meet AI usage demand. This will require investment of up to US$3 trillion.

The forecast demand for compute capacity has been a key driver of real estate M&A and fundraising, with data center strategies accounting for a quarter of real estate fundraising in Q1 2026, according to PERE.

Investors are deploying capital towards strategies where operational improvement, not asset appreciation or market momentum, is the primary driver of performance, reflecting a recognition that future returns will derive from active management, not market conditions.

Indeed, AI’s influence on real estate extends well beyond data centers.

Office sector investors, for example, have been monitoring the impact of AI on office vacancy rates closely.

If AI does lead to significant productivity gains and headcount reductions, there will be an impact on an office sector that is still adjusting to post-Covid working practices.

According to Moody’s figures reported by Axios, employees in the US are spending around a quarter of their working hours working from home, up from just 7% pre-pandemic. Even though companies have pushed staff to return to the office, office vacancies climbed to a record high of 21% in the US in Q1 2026. AI’s potential impact on the workforce is another factor that is holding back demand for office space, although in some cities demand from AI-led companies is boosting office demand. According to CBRE, AI companies have taken up around 1.5m square feet of traditional office space in central London, most of it since 2022. AI now accounts for more than a third (34%) of technology industry office demand – up from just a 4% share in 2015.

Understanding the impact of AI and changing working patterns on office real estate will demand operational insight, as investors aim to protect portfolios against downside risk, but also take advantage of upside opportunities as office dynamics shift.

An operational lens will be equally essential in logistics and warehousing. Vacancy rates for logistics assets are stabilizing across all regions, according to JLL, and higher value manufacturing, increasing defense spending and ongoing e-commerce growth are all positive drivers of long-term logistics demand. Asset selection will be crucial to tap into these specific growth drivers.

The definition of an attractive asset is being fundamentally redefined by occupier demand. Tenants are no longer evaluating real estate on the basis oflocation alone. Tenants increasingly want to customize sites and are looking for assets that can accommodate future requirements, such as automation and robotics, and have the necessary grid connections to power these technologies. For owners and investors, meeting this evolving occupier mandate will be central to sustaining asset relevance and long-term performance.

Looking ahead to the second half of 2026, the geopolitical picture is improving following progress in negotiations to end the war in Iran. Oil prices have come down as an end to the conflict has come into view, reducing inflationary pressures and improving the interest rate outlook.

These are meaningful and timely developments for a real estate sector that will be aiming to rebuild momentum and confidence after stepping back from deals and investment when the Iran conflict first escalated.

But while a stabilizing macroeconomic backdrop may ease decision-making for real estate dealmakers, it will not determine success in a sector that is still in a phase of long-term structural transformation. Operational expertise and disciplined asset selection, rather than low interest rates and rising asset valuations, are now the main drivers of performance in a sector that has fundamentally changed following the pandemic and will continue to evolve as AI changes the way people work,live, and ultimately consume space.

Infrastructure H1 highlights

Maximilian Dambax

Global Head of Real Assets

In a volatile first half of 2026 infrastructure assets distinguished themselves as a source of resilient performance and a buffer against downside risk in turbulent markets.

Over three, five, and ten-year time horizons private infrastructure has posted gross returns in the 10% to 13% range, outperforming listed infrastructure and global bonds, according to CBRE figures.

The asset class has delivered these mid-teen returns with minimal downside risk. Since 2011, there has not been a single five-year period where private infrastructure has lost money, according to Hamilton Lane.

Investors have taken note and allocated capital accordingly. Private infrastructure fundraising reached an all-time annual high of US$289 billion in 2026, according to Infrastructure Investor.

Fundraising did slow in Q1 2026, coming in at US$26.4 billion, down from US$67.5 billion in Q1 2025 and US$39.2 billion in Q1 2024, but private infrastructure assets under management (AUM) remain close to record highs of US$1.6 trillion, and steady inflows into infrastructure funds are anticipated through the second half of the year.

Soaring demand for computing capacity to power the artificial intelligence (AI) boom remains the single biggest driver of overall infrastructure performance.

Consumption of tokens (the fundamental units of data large language models use to process and generate text) is expected to increase 24-fold by 2030 as use of agentic AI tools, which perform tasks autonomously, ramps up, according to Goldman Sachs.

This will underpin ongoing demand for investment in data centers and associated digital infrastructure, including 5G towers and fiber networks. BlackRock’s base case forecasts predict that data center load capacity will nearly double by 2030 from 2025 levels to meet demand.

Private infrastructure capital is emerging as an essential financing force behind the accelerating build-out of the AI infrastructure, and the sector is unlocking substantial pipelines of data center investment opportunities for managers to pursue.

In the US, for example, private capital investment in data centers has more than tripled from previous highs to reach US$45.70 billion, and now accounts for 72% of overall US data center investment, according to S&P.

The AI buildout is also spurring investment in power and electricity infrastructure. Data centers require large amounts of power to run and electricity demand from AI-focused data centers climbed by 50% in 2025, according to the International Energy Agency (IEA).

Advances in AI data center architecture and chip technology have delivered significant gains in AI energy efficiency, but this has been offset by ever more sophisticated – and energy consumptive – AI applications. The IEA forecasts that this will see data center electricity demand double between 2025 and 2030, reaching 950 TWh.

Data center buildouts are not the only factor driving up demand for electricity. Advanced manufacturing, the accelerating adoption of electric vehicles and climate-controlled systems are also pushing up electricity consumption.

This is not only driving up demand for power generation capacity, but also for grid investment. The IEA estimates that annual grid investment will have to increase by 50% by 2030 to meet forecast electricity demand.

Geopolitical conflict and energy security concerns are also contributing to investment opportunities in energy infrastructure. Countries importing hydrocarbons are home to around 70% of the global population, according to BlackRock, and are boosting investment into assets that diversify the energy mix and secure “home-grown” supply, such as renewables and nuclear.

Momentum behind private infrastructure fundraising and dealmaking is building, but the asset class also faces challenges.

As has been the case across all private markets asset classes, liquidity bottlenecks have disrupted the cadence and volume of distributions to private infrastructure investors. Infrastructure investments do typically have longer investment timelines than other alternative assets, such as buyouts and growth capital, but even when this is taken into account, private infrastructure hold periods are extending well beyond what investors anticipated.

According to Hamilton Lane, the number of years it takes to liquidate private infrastructure assets came in at around 10 years in 2025, the longest period on record since 2000.

The slow pace of distributions is reconfiguring investor priorities, forcing managers to adapt their strategies to deliver what investors want.

Liquidity is the priority, and investors are favoring infrastructure categories that offer clearer and more credible pathways to liquidity against an uncertain market backdrop.

Mid-market infrastructure has attracted growing investor attention, as smaller assets, are easier to exit in downcycles.

Signs of growth in investor appetite for exposure to infrastructure debt and infrastructure secondaries further underscore the premium placed on liquidity. Fundraising for infrastructure debt nearly doubled from Q1 2025 levels in Q1 2026, according to Infrastructure Investor. Infrastructure secondaries fundraising, meanwhile, used to make a fractional contribution to overall infrastructure fundraising, but now accounts for around 8% of total takings.

The long-term fundamentals underlying the investment case for private infrastructure remain largely intact and compelling, but the strategies investors are implementing to build exposure to the asset class are evolving.

The performance and resilience of private infrastructure through a volatile cycle are changing the way investors view the asset class.

Traditionally positioned as a defensive asset class designed to generate yield, infrastructure is evolving into an allocation that can also generate growth.

Core infrastructure categories, including transport, roads, ports and utilities, continue to give investors stability and predictable cash flows. This stability has been complemented by upside opportunity, as demand for data centers, and the electricity to power them, soars.

In an uncertain world, private infrastructure has become an essential component of a well-constructed institutional portfolio, rather than a niche add-on.

Analysis

Luxembourg has cemented its position as Europe’s premier fund domicile, commanding 42% of worldwide cross-border public market assets. We explore what makes it the jurisdiction of choice and what it takes to make it work for your fund.

Conor O’Callaghan

Director, Client &

Industry Solutions

Bruno Bagnouls

Global Partner Director

For global asset managers, fund domicile is a strategic priority defining long-term growth and institutional credibility. As Europe’s primary gateway for alternative investments, Luxembourg offers a sophisticated regulatory environment that enables managers to scale, secure institutional capital, and build trust through cross-border distribution depth.

Luxembourg remains central to European capital access. On 31 March 2026, Luxembourg undertakings for collective investment held total net assets of EUR 6,207.82bn, according to the Commission de Surveillance du Secteur Financier (CSSF). The same CSSF update recorded 288 authorized investment fund managers as of 30 April 2026.

Industry data from the Association of the Luxembourg Fund Industry (ALFI) also shows the scale of the wider market. Luxembourg-domiciled Alternative Investment Funds (AIFs) account for more than €3.1 trillion, representing a massive expansion in the private market space.

For managers in private equity, venture capital, private debt, real estate, and infrastructure, the advantage of Luxembourg lies in what it simplifies. Beyond initial recognition, success depends on robust governance, reporting, and fund service provider arrangements that manage the complexities of the fund lifecycle.

Luxembourg’s position is built on scale, familiarity, and cross-border distribution. PwC Luxembourg’s 2024 global fund distribution data cited Luxembourg as the first domicile for 72% of the top 51 firms and noted that it handled 52.3% of true cross-border investment funds globally.

The latest ALFI Broadridge cross-border distribution study found that cross-border fund assets reached EUR 8.5 trillion in 2025, with Luxembourg accounting for 42% of worldwide cross-border public market assets..4 For cross-border strategies, broader AIFM services may also be relevant to management, oversight, and reporting needs.

Those figures are significant because institutional investors do not assess domicile in the abstract. They look for structures that their internal teams, consultants, custodians, counsel, and investment committees already understand. Funds domiciled in Luxembourg benefit from that market familiarity.

The benefits of Luxembourg investment funds, therefore, start with recognition. Investors, advisers, administrators, depositaries, auditors, directors, and regulators are familiar with the market’s main fund regimes. That familiarity can reduce friction during fundraising, onboarding, reporting, and ongoing fund operations.

Luxembourg hosts a dense network of administrators, depositaries, auditors, and legal advisers who manage complex operations—from accounting and capital activity to governance and regulatory filings. This ecosystem provides essential regulatory credibility and operational scale for international managers.

The local workforce’s expertise in EU regulatory expectations reduces the need for GPs to build internal teams prematurely. Consequently, Luxembourg-domiciled funds are supported from formation and launch through to reporting and asset exits.

The appeal for alternative managers lies in the range of legal forms and regulatory regimes that can be matched to investor eligibility, asset class, governance needs, and distribution plans. Common options include reserved alternative investment funds, specialized investment funds, investment companies in risk capital, special limited partnerships, and Part II funds. The broader point is straightforward: Luxembourg gives managers several ways to separate the fund vehicle, management company, general partner, and asset holding arrangements.

That flexibility comes with operating demands. A private equity or infrastructure fund may require capital calls, distributions, financial statements, audit support, investor reporting, regulatory filings, board materials, tax data, and document control. These workstreams need clear ownership, agreed timelines, reliable data, and review processes. Limited partners expect accurate reporting, regulators expect evidence of compliance, and boards need materials that support proper oversight. For managers without a local Luxembourg operating team, those requirements can quickly become difficult to manage internally.

This is where third-party support becomes part of the domicile decision. An administrator can help turn the legal structure into an operating model after the fund has been established. Outsourced fund administration services are one example of how managers may support Luxembourg operations without building every function internally. For managers comparing models, the discussion on in house vs third party fund administration is directly relevant.

The phrase “golden passport” is often used informally to describe one of Luxembourg’s main attractions: The ability to use a European framework for managing and marketing funds across the European Union and European Economic Area.

The CSSF explains that the Alternative Investment Fund Managers Directive (AIFMD) provides an Alternative Investment Fund Manager (AIFM) passport allowing an authorized AIFM approved in an EU or European Economic Area member state to manage alternative investment funds in another member state. It also confirms that the AIFM marketing passport may allow an authorized AIFM to market the AIFs it manages to professional investors across the EU and European Economic Area, subject to the relevant AIFMD conditions.

For managers without an in-house European AIFM, a third-party management company, often referred to as a third-party ManCo, can provide the regulated management company platform required to support a Luxembourg fund. This can be relevant where a non-European GP wants to access European professional investors through an established AIFM structure while keeping investment management, governance, risk, and reporting responsibilities clearly allocated.

This also helps explain why so many funds are domiciled in Luxembourg. The jurisdiction combines European Union market access, a deep alternatives service market, and fund regimes that institutional investors and advisers already know. For a non-European GP, that combination can make Luxembourg easier to explain to investment committees than a less familiar domicile.

AIFM services should still be viewed as an operating and regulatory function, not a distribution shortcut. The AIFM sits within a control framework covering risk management, valuation, delegation oversight, reporting, and investor disclosures.

Luxembourg’s strength is not that regulation is light. It is that the regulatory framework is established, widely understood, and supported by a regulator with deep experience in investment funds.

CSSF regulation is a central part of Luxembourg’s credibility with European institutional investors. Under AIFMD Luxembourg requirements, managers and service providers need governance, risk, valuation, reporting, and disclosure processes that can stand up to review.

The framework is also changing. In March 2026, the CSSF confirmed that Luxembourg had adopted the Law of 3 March 2026 to transpose Directive (EU) 2024/927, known as AIFMD II into Luxembourg law. The update introduced additional liquidity management requirements for Luxembourg-domiciled UCITS and, where relevant, authorized AIFMs managing open-ended AIFs, with effect from 16 April 2026.

For closed-end private equity, private debt, real estate, and infrastructure funds, the direct impact will depend on the fund’s structure and redemption terms. The broader lesson applies across strategies: A domicile decision creates ongoing regulatory work. Managers need processes that can absorb rule changes, update documents, collect data, and produce evidence.

At a high level, Luxembourg investment funds often operate under specific fund tax regimes rather than ordinary corporate taxation, though this is not uniform across all vehicles. Guichet.lu explains that subscription tax, known as taxe d’abonnement, applies to negotiable securities issued by undertakings for collective investment, specialized investment funds, reserved alternative investment funds, and family wealth management companies, with quarterly declaration and payment obligations.

PwC’s 2026 summary adds that rates are based on total net assets, generally 0.01% for institutional or monetary funds and 0.05% for others, with some exemptions. While tax is a draw, managers must also evaluate treaty access, withholding tax, VAT, substance requirements, and anti-abuse rules alongside regulatory needs.

Alternative funds often have lives of ten years or more. Infrastructure and real assets structures may run longer. Luxembourg’s State Treasury reports that major rating agencies assign Luxembourg the highest sovereign rating, AAA or equivalent, with stable outlooks. Its latest update lists stable top-tier ratings from Moody’s, S&P Global Ratings, Fitch Ratings, Morningstar, DBRS, and Scope Ratings. For fund managers, this stability supports long-term planning for regulated vehicles, local service relationships, financing arrangements, and investor governance.

Luxembourg’s position inside the European Union also has implications. It gives managers a domicile inside the EU legal and regulatory system, with access to European fund rules and a professional market built around cross-border capital. That is one reason the country is often described as an EU fund hub and a Luxembourg financial hub.

For international GPs, the value of a Luxembourg domicile extends far beyond initial regulatory and distribution advantages. It provides a mature, reliable foundation for the entire fund lifecycle. Successfully managing a European fund platform requires continuous operational rigor—from the complexities of structuring, compliance, and reporting to the nuances of corporate governance and eventual fund wind-down.

Luxembourg’s distinct advantage lies in its comprehensive service ecosystem, where experienced providers act as an extension of the manager’s team. This infrastructure allows GPs to maintain high operational standards and meet evolving regulatory and investor expectations without the burden of building full-scale local operations from scratch.

By leveraging this sophisticated network, managers can focus on their core investment strategy, secure in the knowledge that every stage of the fund’s life—from launch and day-to-day administration to strategic restructuring—is supported by deep, local expertise.

Through its Luxembourg fund services, Alter Domus provides this critical support, ensuring that operational resilience remains a constant throughout the fund’s journey.

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

For international asset managers, the path to European institutional capital runs through Luxembourg. In this article, learn how the AIFMD passport, the right fund vehicle, and an integrated third-party operating model can remove the barriers to successful European market entry.

Conor O’Callaghan

Director, Client &

Industry Solutions

Bruno Bagnouls

Global Partner Director

For non-European asset managers, Europe offers a clear opportunity but a harder route to market. Managers seeking allocations from European pension funds, insurers, sovereign wealth funds, and other institutional LPs need more than investor demand. They need a fund structure that LPs recognize, regulators understand, and operating teams can support across multiple jurisdictions.

Luxembourg is often where the strategy comes together. As Europe’s leading domicile for cross-border fund distribution, Luxembourg gives US, Asian, and other non-EU managers a credible route to European capital through familiar fund vehicles, access to the AIFMD marketing passport, and an established ecosystem of AIFMs, administrators, depositaries, auditors, legal counsel, and other specialist providers.

Global cross-border fund assets reached EUR 8.5 trillion in 2025, with Luxembourg representing 42% of worldwide cross-border assets under management. But Luxembourg’s appeal is not based on scale alone. For managers raising capital in Europe, it also offers investor familiarity, regulatory credibility, LP confidence, and a distribution model designed for cross-border fundraising.

For many non-European managers, the central question is how to access European capital through Luxembourg without building a full in-house operating platform. Luxembourg’s mature fund services market offers a more practical route. By working with experienced third-party fund administration, non-European GPs can reduce operational lift, meet local requirements, and focus more time on investment performance and investor relationships.

Scale is only part of Luxembourg’s appeal. Managers choose Luxembourg because European institutional investors are familiar with its structures, advisers, service providers, and regulatory framework. That familiarity can reduce friction during fundraising, support LP due diligence, and give investors confidence that the fund is being operated within a credible European environment.

For non-EU GPs, a Luxembourg platform can also demonstrate operational maturity before the first close. It gives finance, legal, investor relations, and operations teams a clearer framework for onboarding investors, coordinating capital activity, managing service providers, and meeting ongoing European obligations.

For CFOs and COOs, the AIFM relationship is also an operating decision. The right AIFM can accelerate time to market while reducing operational friction through effective governance, delegation oversight, valuation, risk management, and regulatory reporting.

Expanding fundraising into Europe can help global asset managers diversify their investor base and scale their platforms. A Luxembourg structure can help global managers raise capital in Europe while giving LPs a familiar governance and reporting framework.

State Street’s 2025 private markets study found that LPs remain focused on private equity, private credit, real estate, and infrastructure, with developed Europe attracting renewed interest from institutional investors.

As European LPs increase their allocations to alternatives, their operational due diligence expectations have also tightened. They are looking for onshore structures with strong governance, clear reporting, and reliable investor protection. Luxembourg benefits from this shift because its fund structures are familiar to global investors and commonly used for cross-border alternative strategies.3

For a non-EU GP, an onshore Luxembourg platform can answer many investor questions early in the fundraising process. It gives LPs a familiar structure, a recognized jurisdiction, and an operating model built around European requirements.

Historically, many international fund managers relied on reverse solicitation to raise European capital. That approach is becoming harder to defend as a long-term distribution strategy.

NPPRs are well suited to targeted fundraising campaigns but do not provide pan-European market access. Managers seeking to raise capital across multiple jurisdictions must navigate separate local filings, creating additional complexity and administrative burden.

Reverse solicitation is also a narrow exception, not a scalable fundraising plan. Under Luxembourg guidance, reverse solicitation requires that the investor act on its own initiative, without solicitation by the alternative investment fund (AIF), the Alternative Investment Fund Manager (AIFM), or an intermediary.4 For managers running an active European fundraising campaign, relying on reverse solicitation creates compliance risk.

A more durable route is the Alternative Investment Fund Managers Directive (AIFMD) marketing passport. Under AIFMD, authorized AIFMs can market EU AIFs to professional investors across the European Economic Area, subject to the applicable notification process.

For managers focused on EU investor access through Luxembourg, the AIFMD passport offers a more scalable route than country-by-country private placement. A Luxembourg AIF managed by an authorized EU AIFM can use the AIFMD passport to reach professional investors across Europe. The result is a single regulated platform instead of a country-by-country fundraising patchwork.

For managers new to the European regulatory model, understanding what an AIFM does is an important first step. The AIFM is not simply a service provider; it is responsible for key oversight functions, including risk management, valuation, compliance, delegation oversight, and regulatory governance.

This is essential because access to the pan-European marketing passport depends on the fund being managed by an authorized, onshore AIFM. For a non-EU GP, Luxembourg can provide a practical base for European distribution when the fund is supported by an authorized AIFM. It requires regulatory capital, local substance, experienced conducting officers, governance arrangements, and time with the Commission de Surveillance du Secteur Financier (CSSF).

Many global managers appoint a third-party AIFM instead of building the infrastructure in-house. This gives the fund access to an authorized management company while allowing the GP to retain control of portfolio management, deal origination, and investment strategy.

Before the first close, managers need clear ownership of investor onboarding, AML/KYC checks, capital calls, NAV production, financial statements, board materials, regulatory filings, and investor reporting. Weak workflows between the AIFM, administrator, depositary, auditor, and legal counsel can create delays even when the fund structure itself is sound.

The third-party model separates investment decision-making from institutional fund operations. The GP focuses on sourcing, executing, and managing investments. The third-party provider supports the fund’s regulatory, administrative, depositary, corporate, and reporting needs.

Managers weighing operating models may also want to compare in-house vs. third-party fund administration before deciding how much infrastructure to build internally.

Experienced providers such as Alter Domus can support the main operating requirements through one platform:

By using one integrated provider, global managers can avoid coordinating several local vendors. The cost model also becomes more flexible, moving from fixed in-house infrastructure to a fund-level operating expense.

For an international asset manager, launching a passported Luxembourg fund usually depends on getting the right structure, partners, and operating model in place before fundraising gains momentum.

1. Appoint a licensed third-party AIFM

Luxembourg AIFM services give managers the regulatory foundation for pre-marketing, marketing, governance, and ongoing oversight across the European Economic Area. For non-EU GPs, appointing a third-party AIFM can also reduce the time, cost, and complexity of building a regulated European management platform in-house.

2. Select the Right Fund Vehicle

The fund vehicle should match the manager’s strategy, investor base, and speed-to-market requirements. The société en commandite spéciale (SCSp), or special limited partnership, is often attractive to US and UK managers because it offers contractual flexibility and characteristics familiar to common-law partnership structures.

3. Coordinate Fund Partners

The GP should establish clear operating workflows between the AIFM, fund administrator, depositary, legal counsel, auditor, and investor reporting teams. This is where many launches lose time. The structure may be right, but weak coordination can delay onboarding, reporting, capital calls, and first-close readiness.

4. Prepare for evolving AIFMD requirements

AIFMD II introduces additional expectations for areas such as loan-originating funds, liquidity management, delegation, substance, and supervisory reporting. Managers do not need to lead with the technical detail, but they do need to know whether their Luxembourg platform can support these requirements in practice. This will be crucial for private credit strategies or open-ended structures, as regulatory and reporting expectations can directly affect launch planning and ongoing operations.

5. Align with ESG and LP Due Diligence Expectations

European institutional investors increasingly expect managers to provide clear, reliable sustainability and portfolio data. Luxembourg is the leading domicile for European sustainable private market funds, representing 77.0% of total sustainable private market fund assets under management in Europe.

A Luxembourg fund structure is more than a regulatory formality. Used well, it signals operational maturity to European LPs and gives non-European GPs a clearer route to cross-border fundraising.

The AIFMD passport only delivers its full value when the fund is structured, operated, and reported on to institutional standards. That takes local knowledge, strong governance, and dependable day-to-day execution.

Alter Domus supports international GPs through AIFM services, depositary oversight, corporate services, and investor reporting. By combining local Luxembourg expertise with technology-enabled operating support, Alter Domus helps managers reduce operational lift and stay focused on investment performance, investor relationships, and long-term growth.

Ready to accelerate your European fundraising strategy?

Discover how Alter Domus’ AIFM services in Luxembourg can support your European market entry, from fund launch through ongoing oversight.

Get in touch to learn more about our range of services.

Please complete the form and a member of our team will be in touch with you shortly.

"*" indicates required fields

Analysis

Luxembourg offers alternative managers a range of fund structures, each with its own regulatory profile, investor eligibility rules, and operational demands. Read on to learn how to navigate the key differences and identify the vehicle best suited to your strategy.

Conor O’Callaghan

Director, Client &

Industry Solutions

Bruno Bagnouls

Global Partner Director

Luxembourg fund structures are often considered by alternative asset managers seeking a European domicile, particularly where the target investor base includes European institutional or professional investors. The market is large and operationally mature. As of 31 January 2026, undertakings for collective investment in Luxembourg held EUR 6,294.473bn in net assets, across 13,286 active fund units.

That scale does not make structure selection simple. Fund structures in Luxembourg differ by regulatory status, investor eligibility, legal form, tax treatment, time to launch, and reporting. A private equity strategy with a small group of institutional limited partners may raise different questions than a private debt platform seeking a European passport, or a real estate manager assessing access to private wealth investors.

Closed-ended and semi-liquid structures are also playing an increasingly prominent role in the Luxembourg fund landscape. Closed-ended vehicles remain well suited to strategies with long investment horizons, such as private equity, infrastructure, and private credit, where fund duration aligns with the illiquidity of underlying assets.

Semi-liquid structures, meanwhile, are gaining ground as a way to extend access to private markets for wealth and semi-professional investors, offering periodic redemption windows or evergreen designs without departing from a longer-term investment strategy. This added flexibility introduces greater operational complexity, particularly around subscription and redemption processing and ongoing valuations, reinforcing the importance of selecting a fund administrator equipped to support hybrid liquidity models.

For non-European managers, comparing different fund structures in Luxembourg usually starts with practical questions: who can invest, how the fund can be marketed, what level of regulatory oversight applies, and what operating obligations follow after launch.

While Luxembourg offers several well-established fund structures, including the RAIF, SIF, SICAR, and ELTIF, these aren’t the only options available. Depending on strategy, investor base and regulatory requirements, ans SCSp (Special Limited Partnership) can also operate as an unregulated Alternative Investment Fund (AIF). The structures below highlight four of the most commonly used regulatory frameworks:

The Reserved Alternative Investment Fund (RAIF) is commonly used where time to market is a major consideration and has become one of the most widely adopted structures for alternative investment managers establishing funds in Luxembourg. A RAIF qualifies as an alternative investment fund (AIF), can invest in all asset types, and is not itself subject to product approval by the Commission de Surveillance du Secteur Financier (CSSF).

It must appoint an authorized external Alternative Investment Fund Manager (AIFM). Where the AIFM is domiciled in the European Union (EU), the RAIF can use a passport to market shares, units, or partnership interests to well-informed investors across the EU.

This indirect supervision model is the main feature that separates the RAIF from directly regulated structures. The fund is not approved as a product before launch, but the AIFM is regulated and must meet AIFM obligations.

A RAIF may be relevant where a manager is targeting well-informed investors and needs an AIFMD structure supported by AIFM services in Luxembourg and European marketing capability through the appointed AIFM. RAIFs can be structured in several legal forms, including a corporate vehicle, a common contractual fund, or a partnership. In private markets, a RAIF is often paired with an SCSp.

The operating model for a RAIF typically includes AIFM oversight, depositary arrangements, valuation, net asset value (NAV) production, investor reporting, regulatory reporting, and audit support. While the structure can accelerate time-to-market compared with some directly regulated alternatives, managers must still establish the governance and operational framework required to support ongoing compliance and investor expectations.

The Specialised Investment Fund (SIF) is a directly regulated Luxembourg fund structure for well-informed investors. It is governed by the Luxembourg Law of 13 February 2007, as amended, and most SIFs qualify as AIFs because of the broad definition of an AIF. SIFs that qualify as AIFs are generally required to appoint an AIFM, unless a limited exemption applies. A SIF managed by an authorized EU AIFM can use a passport for marketing to professional investors in the EU.

The main difference between a SIF and a RAIF is fund-level supervision. A SIF is subject to direct CSSF oversight, while a RAIF is supervised indirectly through its AIFM. Some institutional investors may prefer, or require, a directly regulated product. That preference can affect fund legal structure in Luxembourg, especially for managers raising from pension funds, insurers, sovereign wealth funds, or other regulated investors.

A SIF may invest across asset classes and can be established as an FCP, SICAV, SICAF, or another permitted form. Its net assets must reach EUR 1.25m within 24 months after authorization.

Direct product supervision can affect the setup process, but it can also support investor comfort where the target limited partner base places weight on regulated fund status. This does not make the SIF a default choice. It means the SIF may form part of the discussion where fund-level authorization, ongoing CSSF oversight, and a recognized regulated framework are relevant to the distribution plan.

The Investment Company in Risk Capital (SICAR) was designed for investment in risk capital. It is most often associated with private equity and venture capital strategies, where the investment policy centers on capital at risk rather than diversified asset allocation.

A SICAR that qualifies as an AIF must appoint an AIFM unless a limited exception applies. A SICAR managed by an authorized EU AIFM can use a passport for marketing to professional investors in the EU.

Unlike other fund types that may be set up in contractual form, a SICAR must be constituted as a corporate entity with fixed or variable share capital. The subscribed share capital, including share premiums, must reach EUR 1m within 24 months after authorization.