Once again, Alter Domus is proudly sponsoring IMN’s Winter Forum on Real Estate Opportunity and Private Fund Investing from 17-19 January in Laguna Beach, California.

Join our very own Stuart Wood, Stephanie Golden, Rachel Roth, Michael Gregori, and Michael Dombai at the conference and gain insights into the geopolitical, tax, and regulatory factors transforming the commercial real estate industry. Stuart Wood will also be moderating the panel, “Getting the Most Out of Your Fund Administrator” on the 18th at 11:30AM PST.

Click here for the full agenda. We look forward to seeing you there!

Don’t miss your chance to connect with our team beforehand and schedule a meeting.

Managing Director, Sales and Relationship Management, Private Equity

More events

No related content found.

News

Alter Domus leads global growth in assets under management

In Funds Europe’s most recent Private Markets Administration Survey, Alter Domus topped the charts for the highest net AuM growth globally amongst its peers.

Sandra Legrand

Regional Executive, Europe & Asia Pacific

On the global stage, the narrative of AuM growth amongst administrators presents a landscape of rapid expansion and strategic realignment. Alter Domus tops the list with a net growth of $54.1 billion. Compared with its third rank in Europe, this global standing points to its expansion strategies and successful global positioning, surpassing regional limitations to claim a more prominent role on the world stage.”

Funds Europe Private Markets Administration Survey 2023

Sandra Legrand explained how Alter Domus has continuously adapted to emerging developments in the private markets sector.

As investment franchises grow, so do investments and the attention needed for middle- and back-office operations: expertise, technology platforms and trained resources. Add diversification in investor groups, targeted investment markets or asset classes, and fund operations can choke development and innovation. Alter Domus has responded by developing digital and operational solutions, allowing asset managers and owners access to expertise, technology and resources. Our approach is flexible, adapted to their strategic objectives, and focused on removing the burden of day-to-day production and stakeholder management while allowing them to focus on investors, investments and risk management while retaining data oversight and control.”

Sandra Legrand, Regional Executive Europe & Asia Pacific

The introduction of hybrid funds and regulatory enhancements like ELTIF 2.0 have enabled the retailization of alternative funds, opening up new distribution channels for GPs and managers, and providing diversification and better returns for pension and retail savings funds.

Antonis Anastasiou

Head of Product Development

How demand for diversification and returns is reshaping private market capital raising

2022 has been a difficult year for capital raising for PE funds showing a decline of 11% in comparison to the 2021 all-time high, according to Preqin data. This has been due to the decrease of LP commitments and Institutional investors reducing their exposure by approximately 3%. Interestingly, a new market has been forming by private individuals and wealth managers demand for diversification and higher returns. As such, GPs and Managers have been forced to seek fresh means of accessing capital to support new vintages.

Mix into this dynamic new regulatory enhancements which have enabled the creation of “Hybrid Funds”. These are effectively the traditional alternative fund strategies we know however incorporating open-ended features and accepting retail investors. This ‘retailisation’ of alternative funds is a term now widely utilized within the industry.

These favorable regulatory adaptations can be a game-changer. For instance, the European Long Term Investment Fund 2 regulation (“ELTIF 2.0”) has been met with positive reactions from both investors and managers.

ELTIF 2.0 and the evolving retail investor landscape

The adoption of the new regime in Europe was completed in April 2023 and comes into force in January 2024. This will replace the existing ELTIF regulation, which has struggled to find its place within the structuring toolbox of Fund Managers as a viable solution. Similar adoptions can also be seen in the rest of the world with the Financial Conduct Authority (FCA) developing the open ended LTAF funds, and in the US defining “accredited investors” which enables certain investors with a level of sophistication warranting a reduced need for protection to invest in alternative products.

The original regime however failed to obtain significant traction with only 83 funds launched. This was predominantly driven by the high level of restrictions which reduced the flexibility that alternative strategies need to flourish.

The much-anticipated ELTIF 2.0 regime has taken a step in the right direction by making it a more attractive vehicle for addressing the “retail market” for alternative asset managers. Key impacts on the PE world include:

Funds can now be structured as open-ended Funds with a minimum annual subscription and redemption opportunity

The removal of the 10 million minimum value threshold for eligible real assets; opening up investment opportunities

The minimum threshold for investments into eligible assets has also been reduced from 70% to 55%

It’s now possible to invest into other EU AIFs and not just other ELTIFs hence liquidity management can also be addressed through AIFs with similar strategies to manage the liquidity requirements

Rules on distribution have enabled the use of a marketing passport across the EU and now allow for retail investors (additional restrictions apply if purely marketed to retail investors)

How hybrid funds change the game for service providers and asset managers

For Administrators this will require a variety of tools that are able to manage funds with open ended features which were primarily associated to the UCITS world. Additionally, there is a need for systems that can handle portfolio accounting for both illiquid and liquid assets.

For Depositories, the retail regime is geared towards optimal protection of the investors, insofar that only Banks can operate as Depositary for the ELTIF 2.0. This will open the road for specialized banks who will need to blend liquid and illiquid setups together to manage these hybrid funds.

For asset managers there will also be a steep learning curve in managing investors with liquidity requirements that PE firms are unfamiliar with. This could lead to the need for restricted redemptions, highlighting the complexity of incorporating such liquidity measures into their portfolio.

With these challenges comes the added value that such structures benefit:

GPs/Managers by paving the road to new distribution channels reaching both Private and Professional investors and

Pension and retail savings funds seeking diversification and better returns in an asset class which initially could have been out of scope.

The looming AIFMD 2.0 could however incorporate new limitations, but as of now the ELTIF 2.0 has been branded by many as the new UCITS for Alternative Funds.

Why Luxembourg leads as the Top Domicile for ELTIF 2.0 Funds

Luxembourg has become one of the world’s leading fund domiciles over the past 30 years, driven initially by UCITS and later strengthened by the 2013 adoption of AIFMD. This opened the door for alternative managers to scale strategies for professional and institutional investors. Today, Luxembourg’s regulatory stability, deep service provider ecosystem, and history of fund innovation position it as a natural home for Hybrid ELTIF 2.0 Funds.

Its structuring options—such as UCI Part II Funds—offer broad asset eligibility and, in theory, could admit retail investors. Combined with its proven track record and readiness to support hybrid models, Luxembourg stands out as the ideal hub for the growth of ELTIF 2.0 and the retailization of alternative investments.

Unlocking the Next Era of Private Markets

The retailization of private funds—driven by hybrid structures, regulatory shifts like ELTIF 2.0, and investor demand for broader access—marks a pivotal evolution in the alternatives space. As the line between institutional and retail capital continues to blur, fund managers and service providers must adapt to a new operational reality that prioritizes flexibility, transparency, and liquidity.

With its established infrastructure, regulatory foresight, and legacy of fund innovation, Luxembourg is uniquely positioned to lead this next chapter. For firms ready to embrace this shift, the opportunity is clear: tap into a broader investor base, diversify distribution channels, and help redefine what access to private markets looks like.

From chaos to harmony: How Alter Domus’ data science team extracts value from corporate financial statements

Alter Domus’ financial data spreading service leverages Machine Learning, automation, and in-house domain expertise to rapidly deliver digitized borrower-level financial statements for the alternative investment industry. Amy Wu of our data science team explains the process and why partnering with Alter Domus is a difference maker.

Amy Wu

Head of Data Operations

How do we define financial spreading?

Financial spreading is the process of taking bespoke financial statements and representing the data in a standard, structured format. The key thing to note is that since private market financial statements have variable reporting formats, financials must be standardized first before undergoing credit analysis. This requires an analyst to manually populate a structured template with the information from the tables within a financial statement which can take a huge amount of time to complete.

Can this manual work be outsourced?

Yes, private debt managers will often outsource this work to save on costs. However, we’ve spoken to many chief operating officers and chief risk officers in the last couple of years and the message we’ve heard is that turnaround times are not generally improved via outsourcing; they’ve also highlighted how credit analysts often need to manually review and correct errors in outsourced work to ensure that the spreading has been done correctly.

How is partnering with Alter Domus to perform data extraction different?

A good question. Alter Domus’ Digitize – Corporate Financials solution uses machine learning and automation to significantly reduce the time to digitize financial information and ensures high-quality, accurate data by leveraging in-house experts for quality checks.

It’s important to emphasize the human element here. Computers may be fast, but they need some human help to ensure that the spreading is performed correctly. At the end of the day, we’re generally dealing with unstructured original documents in non-universal formats, and that’s where our dedicated data science team steps in to work in tandem with our market leading tech.

It’s worth highlighting that unlike general machine learning models, Alter Domus’ machine learning capability is trained on millions of financial statements to identify tables, columns, and fields and extract data from tables.

The client’s raw data is extracted from PDF formats using advanced Deep Learning models. A manual raw data extraction quality check is put in place to verify the extracted results and provide a feedback loop back to the machine in a continuous, supervised learning process. If an Excel file is provided, then the data does not need to be processed by this initial step as the raw data is already digitized.

So, the data is ingested and digitized. What happens then?

After the extraction process, the data is normalized, aggregated, and checked through automated QA testing, after which it’s then validated by an in-house credit analyst. This as-reported output flows into two views. Firstly, a Management Account View and, secondly, a Universal View. The Management Account View is the aggregated time series data for a single borrower based on the reported line items from the original raw PDF data. This view is different among borrowers. The Universal View is the aggregated time series data in the Alter Domus standardized template, which is the same across borrowers.

The conversion into the Universal View is done by applying Alter Domus’ rule set to automatically map reported line items into corresponding categories. If the client has their own custom template, Alter Domus will work with the client to define their own category definitions to create their own custom mapping rules. Once again, our data science team will always perform a last QA check before delivering the final output.

Ultimately, where other solutions simply provide clients with raw data output, our system and methodology provide users with tailored, customized data that can be seamlessly deployed to whatever downstream systems – from portfolio or asset monitoring platforms to risk modelling and reporting tools. The point is that data is now primed and ready for deeper analysis.

What does this mean for our clients?

Effectively, it means they can import the formatted financials to their downstream systems the day after the source documents have been uploaded instead of waiting up to 3 days for a standard outsourcer to do the same work. That’s a significant difference in time and allows our client and its teams to focus on higher-value tasks.

Digitize – Corporate Financials goes beyond simply providing a digital representation of the borrower financial information, which is where most outsource companies service finishes. To provide consistency for comparing data over time and across borrowers, all values are converted from reported units to actual units during the automated process. In addition, the service automatically processes the data restatement from pro forma reports when available and provides period over period change information to identify reporting outliers.

We think having humans and machines working in lockstep is essential for us to speedily provide our clients with accurate data that’s been honed and harmonized to meet the exacting needs of their specific organization.

Interested in finding out how we can help you achieve a new level of data sophistication? Get in touch today to speak with a member of our Sales Team.

Co-sourcing, lift-outs help fund managers thrive amid change

Business as usual may have a nice ring to it, but for alternative investment fund managers, there’s really no such thing as “usual.”

Sandra Legrand

Regional Executive Europe & Asia Pacific

The market’s always in flux, regulatory requirements can seem like moving targets, and investor demands for more information, more transparency, and more timely reporting can stress even the best in-house staff and systems. And that’s not even to mention the effect growth, spin-offs, mergers, and acquisitions have on daily operations.

Trying to keep up with it all can drain resources and shift the focus away from strategy and returns, which is why so many fund managers are outsourcing administrative responsibilities to reduce day-to-day burdens.

Yet even outsourcing is evolving. Long gone are the days of task-oriented, commoditized relationships with multiple providers, each furnishing different ancillary services. They’ve been replaced by deep partnerships with asset class specialists — experts who can provide all the jurisdictional, operational, and systems support a fund manager needs across the globe.

And while that’s a highly successful model, still another concept is emerging, driven by the need for real-time data. It’s called co-sourcing, and it’s a hybrid way for fund managers and administrators to work together.

Co-sourcing ensures data control

Co-sourcing exists at the intersection of insourcing and outsourcing. Under the co-sourcing model, the administrator handles the day-to-day back- and middle-office operational activities while the fund manager retains ownership and control of their in-house technology and data solutions. That reduces the back-and-forth of information between the administrator and fund manager, meaning the fund manager can access the data in real time to speed decision-making and respond more quickly to investor requests. The administrator can also retrieve the information required to perform stakeholder management functions, but data confidentiality, integrity, and security remain firmly in the hands of the fund manager.

Lift-outs: Lower expenses, same trusted talent

As fund managers grow their investment franchises, meeting data demands can become increasingly challenging, to the point where it takes nearly continuous reinvestment in technology and in-house operations just to stay even. But making non-stop capital expenditures isn’t always feasible or attractive, and neither is shouldering rising human resource costs.

As an alternative, some administrators will conduct a “lift-out” of the fund manager’s operational teams, making them their own employees. Although the staff now fall under the administrator’s overhead, they remain completely dedicated to the fund and its activities. In other words, there’s no loss of talent or attention, but the cost center changes, and the fund manager is freed from the complexity of managing a back or middle office.

Staying a step ahead

Choosing the right fund administrator is a decision no one takes lightly; there’s just too much at stake. But ultimately, a good administrator will provide white-glove service; add value to the portfolio, risk management, and investor teams; and constantly upgrade their technology.

Most of all, they’ll be innovators who know how to stay ahead of the market and the industry, making the concept of “business as usual” not so unusual in the end.

Whether transacting on the secondaries market or adapting to new regulations, having access to the right expertise, data and analytics capabilities will help investors keep pace with change, says Alter Domus CEO Doug Hart

Doug Hart

Chief Executive Officer

How robust is the LP-led secondaries market right now?

The secondaries market is more robust than we have ever seen it. Capital raises are up – there was a 30 percent jump in secondaries fundraising in the first half of this year, versus 2022. On a relative basis, the jump is even more pronounced, seeing as the overall fundraising market for private equity is pretty flat.

Secondaries had always been a single-digit percentage of the overall marketplace, but now we are seeing it move into the low double digits. Furthermore, LPs are now leading the majority of secondaries deals, which is quite different to the situation we have seen in the past few years.

This is a logical result from the market dynamics that are playing out. In a prolonged low fundraising marketplace, we are seeing concentrations build within LP portfolios due to fewer new funds being launched. Distributions have also slowed in the last 12-18 months, so there is a significant change in the return perspective – we are going from more of an IRR-led model, to a distributed to paid-in capital or a return on capital model.

Generally, this is a space LPs want to be in, while ensuring they have proper asset allocation across secondaries and are not overly exposed. In addition, they want to be relevant players in the marketplace.

Can the secondaries market retain momentum as the broader market rebounds?

This year we’ve seen major market players raising capital for massive, multi-billion-dollar secondaries-specific funds, with many longer-term forecasts indicating that the market will continue to grow and become a bigger piece of the private equity landscape. The volume of actual secondaries transactions may be influenced by what happens with the inflationary environment and interest rates, which have caused headwinds for private equity over the last 18 months.

But there are two other factors to consider here, the first being that a secondaries play isn’t the blunt tool of its earlier years, when it was just used to generate short-term liquidity. This is a market and a strategy that have really come to maturation, and LPs are increasingly using what’s now a very nuanced instrument to actively help manage the composition of their portfolios.

Secondly, the increase in secondaries volumes and activity is attracting a lot of talent in the marketplace today – there’s been huge industry investment in standing up dedicated, specialist secondaries teams. From an Alter Domus fund administration perspective, some of the best individuals in our teams are moving into this space to continue to take on demand and support onboarding requirements for secondaries, which involve more reporting, and more detail than ever before.

What this all indicates is there’s now a very defined ecosystem around the secondaries market, and we are unlikely to see all that talent and creativity suddenly shift away from it – secondaries will likely continue to play a vital role in LPs’ strategic investment plans.

How do you see this ecosystem around secondaries evolving?

There is more demand on reporting and more demand on LP transfer process efficiency. In the past, the somewhat bespoke nature of secondaries allowed for much longer timelines for investor onboarding. Today, those timelines are truncated to the point where processes are advanced quickly to meet the timelines for the new marketplace velocity.

One aspect of that, as we look at the ecosystem’s evolution, is that there are new participants coming into the marketplace around data and analytics. There is a body of data now and more standardization. This ecosystem is allowing data and analytics, tracking, forecasting and modeling to become much more advanced. Investors can come in and have confidence to position their portfolios in an allocation structure that is more nuanced, or more advanced, than in a marketplace without data and analytics capabilities.

Turning to private markets more broadly, what are the main regulatory changes that LPs and GPs should be aware of in the next year?

The biggest change in Europe is the new European Long-Term Investment Funds Regulation (ELTIF 2.0), which comes into force in January 2024. This is going to expand the permissible investments that can be brought into a portfolio. There will be a lot less prescription in the regulation, which means there is more scope for creativity in how a portfolio is constructed. It will be interesting to see how that plays out.

The big headline that we are focused on is the democratization of closed-end vehicles. A lot of private market assets historically have not been open to retail investors, and ELTIF 2.0 will address that. Almost overnight, we will see retail investors have an entry point into private markets.

The US market, meanwhile, has historically been less regulated. There are more opportunities for high-net-worth individuals and retail investors to invest in private market funds. But the US Securities and Exchange Commission recently decided to strengthen regulation of private fund advisers, largely because it wants to protect retail investors. It is going to require a lot more disclosure, reporting and real-time assessment of the investors coming into the portfolio and the portfolio’s ability to provide sufficient liquidity and information to that investor.

There are various opinions on these rules, and they are being challenged quite vigorously in the courts. From our perspective, we are excited by the opportunity to open up private markets to a large channel of new investors. We are tracking the situation closely and are prepared to be on the forefront to ensure those investors come into an information-rich environment.

What are the challenges to supporting clients across both Europe and the US, given the complexities of the regulatory environments?

Very few firms have the size and the scale to support a complex, complete understanding of both markets. The regulatory environments and the reporting requirements are both complex, and the complexity is doubled if you need to pivot between the two. Most of our clients are naturally more familiar with their home region and look for support from service providers like us when they operate in other jurisdictions.

We have always had the ethos of being where our clients need us to be. The key thing is to find the right talent in different markets who have knowledge of the local regulations and expertise in operating in the private markets.

The search for new capital and the emergence of hybrid funds

In the second article of a four-part series on raising capital in Europe, we explore the factors that have been driving the emergence of hybrid funds. Insights come from Antonis Anastasiou, Group Head of Product Development, and Conor O’Callaghan, Head of AIFM Ireland.

The alternatives landscape is changing. While once reserved for institutional investors, pension funds and high-net-worth individuals, it is now opening its doors through the democratisation of alternative funds. A coming together of worlds so to speak, which are combining and innovating to create a hybrid world of liquid and illiquid funds, which are both now open to individual investors.

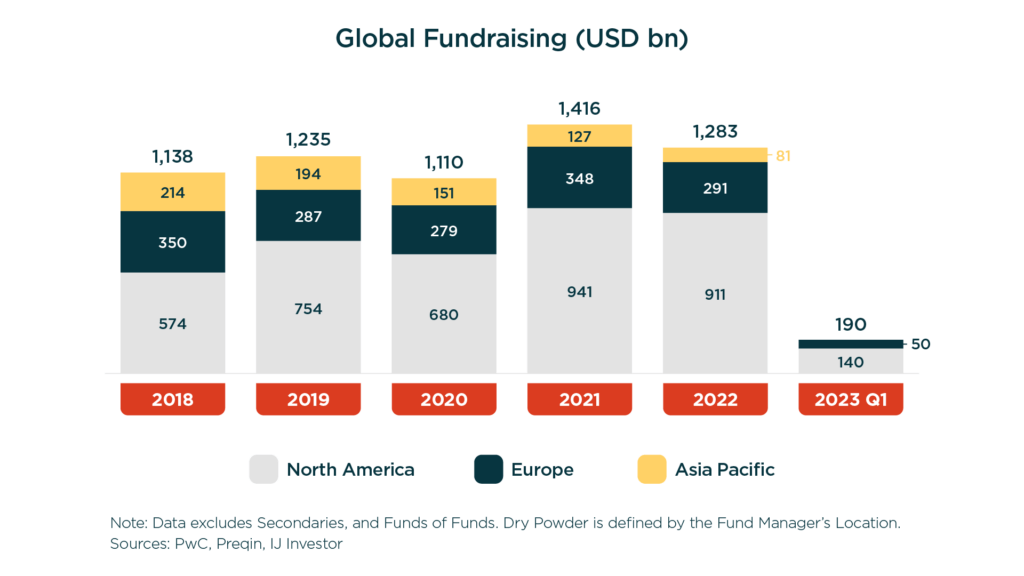

There are a number of trends and drivers in the market that have been behind the emergence of these hybrid funds. Firstly, monetary tightening is resulting in institutional money pulling back from the market. Private asset AUM continues to grow, however traditional LPs are reducing new commitments with global fundraising declining by c. 10% in 2022, followed by further declines so far in 2023 – GPs have been forced to pursue alternative sources of capital to support fundraising.

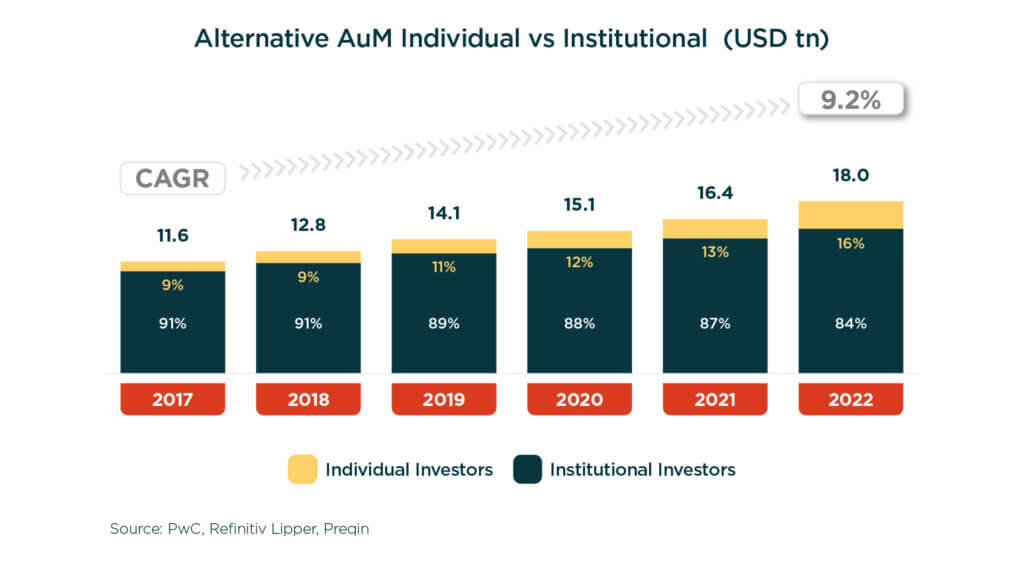

At the same time, a new demographic of investor is seeking to gain access to such markets. While private asset funds have long been used by institutional investors, due to regulatory restrictions, private individuals have been limited in their ability to allocate funds to the asset class. As this portion of the market is becoming more sophisticated and educated, individuals’ appetite for private asset funds is growing as they recognize that gives them more options to build a more diversified portfolio. While allocations by this investor group accounted for 9% of Alternative AUM in 2017, that climbed to 16% in 2022, a 165% increase in AUM.

Hybrid funds have the traditional alternative fund strategies, while also incorporating open-end fund features and accepting individual investors, with the goal of bridging the gap between individual investors and private assets. Within the industry, that’s often described as the ‘democratization’ of alternative funds, with Bain forecasting that individual wealth allocated to alternative investments will increase 12% annually over the next decade while institutional capital will grow by 8% annually over the same period. We have seen how large managers are directing their funds towards retail clients, with Blackstone expanding retail capital from $200 billion to $500 billion, while KKR are looking to raise up to 50 per cent of their new capital from private wealth and Apollo are looking to raise $50 billion in retail capital from 2022-26.

New regulations pulling in the same direction as the market

Regulation is at the forefront of the market’s needs and is allowing the market to deliver these types of products to individual investors at the very time it’s looking to do so.

In the UK, the Financial Conduct Authority has developed the open-ended Long-Term Asset Funds, or LTAFs, while in the US the term ‘accredited investors’ has been defined, enabling sophisticated investors who have a reduced need for protection to invest in alternative products. In Europe, welcomed enhancements to the European Long-Term Investment Fund, or ELTIF, came into effect in January this year, replacing the existing ELTIF regime. We will be exploring ELTIF 2.0 in greater detail in the next two articles in the series.

Now is the time to take advantage

This new regulatory landscape is providing a toolbox for managers, enabling them to develop products and expertise for the retail network. At Alter Domus, we are already working with managers to capitalize on these developments while overcoming the challenges that come with it, which we will be looking at in the fourth and final article.

We’re delighted to be returning as an exhibitor sponsor at the forthcoming Opal’s CLO Summit in Dana Point, California, from 3 – 5 December 2023.

With lower funding costs in the third quarter, the CLO market has been busy in Q4 – although still behind on previous years. Against this backdrop, the summit’s agenda will focus on the most up-to-date techniques for maximizing returns and mitigating risk in the rapidly growing field of asset-backed finance.

Hosted by Opal Group, the CLO Summit is a prestigious educational forum that brings together a diverse range of industry professionals, including investors, issuers, underwriters, rating agencies, lawyers, and accountants. This event provides an open forum for discussing concerns related to collateralized loan obligations and exploring the latest developments in this market segment.

Kennedy Glasscock, Lora Peloquin, Greg Myers, John Coviello and Jackson Carneiro will be representing our capital markets team. Please get in touch if you’re interested in scheduling a meeting with them.

Key contacts

Greg Myers

United States

Global Sector Head, Debt Capital Markets

Lora Peloquin

United States

Managing Director, Sales, North America

More events

No related content found.

News

Testing the market: Pre-marketing – a compelling solution to capital raising in the EU

In the first article in a four-part series on raising capital in Europe, we look at why non-EU fund managers should be exploring pre-marketing along with other upcoming regulatory changes shifting the alternative landscape, namely ELTIF 2.0 and the democratization of alternative funds. Insights come from Antonis Anastasiou, Group Head of Product Development, and Conor O’Callaghan, Head of AIFM Ireland.

There seems to be a misconception among non-EU alternative fund managers that Europe is a complex and closed market for raising fresh capital.

Those managers are being advised that reverse solicitation is no longer an option following the August 2021 changes to the AIFMD Marketing Rules. This is rightly so in our opinion, as it should never have been considered a marketing strategy in the first place. That being said, the knock-on effect is that they are no longer actively considering raising capital in Europe.

What is clear to us is that such managers aren’t being fully made aware that there are other marketing solutions for their funds. ‘If reverse solicitation is no longer an option,’ they say to us, ‘why would I spend the time and effort to try raise capital in Europe?’

The immediate answer we give to that question: pre-marketing.

Once we raise the subject of pre-marketing – and how it is a far more cost-efficient and timely way of engaging with prospective investors before launching a fund – we sense that managers become very interested. It’s at that point that they often start to reconsider what opportunities there may be across Europe.

Clarity for fund managers: the rules about pre-marketing

The current EU rules around the pre-marketing of alternative investment funds have been live since August 2021. Previously, what constituted pre-marketing – which was sometimes known as ‘soft marketing’ – hadn’t been universally defined across the EU member states. Different rules in different jurisdictions meant the process was considerably more complex, with fund managers often needing legal advice about what was allowed in each country.

Much of that complexity has been removed. The introduction of harmonized, EU-wide, pre-marketing rules has provided greater clarity for fund managers who are looking to navigate this market and need to understand what preliminary promotional activities are permitted before establishing a fund.

What is permitted: the definition of pre-marketing in Europe

Across all EU member states, pre-marketing is defined as the provision of information on investment ideas and strategies, as well as the track record of the manager. That information is provided by, the authorised representative, to investors in the EU to test their interest in a fund that has not yet been established or has been established but has not at this stage been notified for active marketing. To comply with the rules, pre-marketing must not include information that could amount to an offer or a placement to the investor.

To engage into pre-marketing discussions with potential investors, alternative managers simply need to select an AIFM they would like to work with. In-turn the AIFM files a notification with their local regulator on behalf of the manager. The notification details the intent to launch a fund and their wish to initiate discussions with potential investors in the countries listed in the notification (passporting rights).

Cost efficient and faster: why fund managers are using pre-marketing

Fund managers are finding that with pre-marketing, the previous cost barriers to initiate discussions and test the market – which could run into hundreds of thousands of Euros – are no longer there. They’re able to gauge investor interest first before incurring the expense of launching the fund.

Pre-marketing is also faster. Previously, managers had to first go through the process of establishing the fund or vehicle. Then they had to appoint service providers including the AIFM, who in turn had to notify the regulator in each of the countries in which they wanted to commence marketing. Obtaining regulatory approval from all the relevant authorities could take up to an additional 21 days following launch of the fund.

Under the current rules, that’s no longer necessary. A Pre-marketing arrangement takes just a couple of weeks to set up. All that is needed is the submission of notification to the relevant regulator, but it does not require formal approval. Once activated you’re able to test the appetite for your strategy with investors across Europe. Once you’re confident to proceed and you feel you have sufficient interest, you can go ahead and establish your fund. This could also be a process which can run in parallel with pre-marketing.

Further regulatory enhancements and the emergence of ELTIF 2.0

Any fund manager who is considering raising capital in Europe should be aware that pre-marketing is only permitted when approaching professional or well-informed investors. When used in conjunction with the passporting rights that come with a pre-marketing arrangement, a manager can register in one EU member state, to pre-market across all member states, and now reach a broader range of potential investors while minimizing initial outlay. Pre-marketing and marketing passport rights will also apply to the new adaptation of the existing European Long Term Investment Fund regime, known as ELTIF 2.0, when it comes into effect in January next year. These enhancements to ELTIF 2.0 will also open access to a retail network eligible to invest in ELTIF 2.0 funds.

A new market of private individuals and wealth managers, comes at a time when there has been a decline in commitments from traditional LPs and institutional investors to GPs and managers.

Over the remaining three articles in this four-part series, we will take you through the new adaptations of the ELTIF 2.0 framework. We will also cover key considerations you may wish to address when looking to raise capital in Europe and how we are preparing to serve our clients as the fundraising landscape in Europe evolves.

In the dynamic landscape of fund administration, co-sourcing emerges as a strategic solution to meeting increasing investor demands for precision and real-time data.

Jessica Mead

Regional Executive North America

With the number of fund administrator firms growing by 10% since 2018, how can companies stand out in an increasingly crowded market to provide added value to their clients?

For Jessica Mead, Regional Executive North America at Alter Domus, the answer lies in successfully blending technology with human expertise, with co-sourcing an increasingly popular way to marry the two.

Jessica shared her thoughts during a service provider webinar Oct. 25 sponsored by investment data company Preqin, where she joined panelists Peter Naismith, a partner in law firm Schulte Roth & Zabel, and Meera Savjani, Fund CFO at Arrow Capital.

Co-sourcing model: integrating expertise and technology

While information has always been key to strategic decision-making, Jessica said that GPs are under increased pressure from their investors to provide more precise and transparent data, and to do it in real-time. Service providers who can meet those demands are going to be more successful, she believes, and co-sourcing may be a way to get there.

In the co-sourcing model, the GP maintains ownership of their in-house IT system and data while their service provider works in the environment alongside other departments. Co-sourcing helps GPs meet the shortened reporting timelines requested by investors yet maintain, or even improve, data accuracy.

It can also improve standardization, Jessica said.

“While LPs’ demands can make standardized reporting difficult to achieve, co-sourcing with an experienced service provider means GPs can still achieve industry best practice standards while meeting customized reporting demands,” Jessica explained.

As well as technological expertise, co-sourcing offers another important and complementary client benefit – systems and sectoral expertise. Marrying technology with this expertise, as well as finding the right culture fit, is at the heart of the co-sourcing concept.

In response to Preqin’s claim that AI is being included in due diligence questionnaires for fund administration services, Jessica said she hasn’t seen much of that so far. She noted that Alter Domus is already ahead of the trend by developing tools in-house across the company’s suite of services to streamline some of the more repetitive functions. She also noted that, by automating more and more areas of fund admin, firms will not only need to provide that data output in real time to clients, they will also need to offer value-added expertise to stand out from the pack.

Finally, looking ahead to 2024, Jessica predicted there will be further consolidation in both the service provider and the manager space.