Analysis

Rising operational complexity, lean teams, and expanding investment mandates are driving wealth managers and family offices to consider outsourced fund administration.

As a COO or CFO of a wealth manager, multi-family office, or OCIO, you carry a responsibility that extends well beyond numbers. You’re not just managing books—you’re safeguarding a family’s legacy, ensuring operational resilience, and giving principals the confidence that their capital is stewarded with precision. That mandate has only grown more complex.

Expanding into direct deals, private credit, real estate, and cross-border structures means you’re expected to deliver institutional-grade reporting, governance, and controls—often with lean teams and finite resources. It’s a balancing act: meeting rising operational demands while protecting the office’s agility and focus. This is exactly where an outsourced fund administration model becomes invaluable.

Outsourcing isn’t about relinquishing control—it’s about fortifying your operational backbone so that you can focus on higher-value work. A trusted fund administrator brings:

For COOs and CFOs of wealth managers and multi-family offices, partnering with Alter Domus means strengthening your operational backbone without losing control. Our model is built to meet the rising demands of complex investment offices while safeguarding the agility and stewardship your principals expect.

As a COO or CFO, you sit at the heart of your company’s success. You’re tasked with ensuring both operational excellence and strategic foresight. We see what your peers are doing and understand which processes work.

In today’s complex landscape, outsourcing fund administration services is not about giving up responsibility—it’s about giving yourself the tools, expertise, and confidence to meet the family’s needs today and for generations to come.

Analysis

The vital role of attentive fund administration services in minimizing stress, addressing auditor inquiries, and safeguarding operational efficiency during audit season.

For asset managers, audit season is more than a routine compliance exercise—it is a critical period where operational precision, regulatory adherence, and investor transparency are all under the microscope. Even well-run funds can feel pressure during this time: schedules tighten, audit teams request detailed reconciliations, and reporting must be flawless across multiple fund structures and geographies.

For managers working with fund administrators who take a tech-first, low-touch approach, these challenges are magnified. While technology can streamline reporting and data aggregation, it cannot on its own replace proactive, hands-on guidance. Additionally, administrators with low or varying service quality may struggle to scale up or adapt to clients’ changing needs, further complicating the audit process.

The most common stress points exacerbated by a lack of high-touch support include:

A high-touch fund administration model mitigates these risks. Dedicated teams with deep operational knowledge and experience across fund structures:

Ultimately, the difference between a stressful audit and a smoothly managed one comes down to the support model. Technology is essential, but human expertise, proactive guidance, and a relationship-driven approach ensure accuracy, efficiency, and peace of mind.

At Alter Domus, we combine leading-edge operational platforms with white-glove service. By integrating technology with hands-on support, we help asset managers navigate audit season confidently reducing risk, freeing internal resources, and delivering the reliability that investors and auditors demand.

Analysis

Explore how tech is reshaping fund administration through automation, APIs, and smart ops. Discover what GPs and COOs should prioritize in 2025.

The investment landscape has shifted dramatically, with fund administrators facing rising investor expectations, regulatory complexity, and market volatility. Traditional approaches no longer suffice.

Investors now demand greater transparency, faster reporting, stronger security, and lower fees—making technology the key differentiator between administrators that thrive and those that fall behind.

Most wealth managers already rely on digital platforms—94% of firms with $500M+ in assets and 61% of smaller firms use fintech to improve client engagement and efficiency.1 The question is no longer whether to adopt new technology, but how quickly and effectively it can be deployed to transform operations.

The journey from manual processes to intelligent automation represents perhaps the most significant shift in fund administration technology. Historically, fund administrators relied heavily on spreadsheets and manual data entry—approaches that were not only time-consuming but prone to human error.

Modern fund administration technology has evolved to replace these outdated methods with integrated systems that automate routine tasks. Advanced platforms now handle everything from NAV calculations to investor communications with minimal human intervention. This transition eliminates the bottlenecks associated with manual processing while dramatically reducing error rates and improving overall efficiency.

Document management has traditionally been one of the most labor-intensive aspects of fund administration. The digitization of workflows and document handling represents a quantum leap forward, enabling administrators to process, store, and retrieve critical information with unprecedented speed and accuracy.

The benefits extend beyond mere efficiency. Digital workflows create audit trails that enhance compliance and security while reducing the risk of document loss or unauthorized access. For fund managers and investors alike, this translates to greater confidence in the integrity of administrative processes.

Application Programming Interfaces (APIs) have revolutionized how fund administration systems interact with each other and with external platforms. By enabling seamless data exchange between previously siloed systems, APIs create a connected ecosystem that supports real-time information sharing and processing.

This connectivity allows fund administrators to integrate with banking platforms, trading systems, and investor portals, creating a unified experience for all stakeholders. Rather than waiting for batch processing or manual reconciliations, information flows continuously between systems, enabling near-instantaneous updates and reporting.

The power of RNFs becomes clear when comparing SCR requirements. Consider two scenarios:

Perhaps the most tangible benefit of fund administration technology is the transformation of investor reporting. Traditional reporting cycles often stretched over weeks, with manual data collection and verification creating significant delays. Today’s technology-enabled administrators can compress these timelines dramatically, delivering accurate reports in days or even hours. 81% of clients using fintech platforms in 2025 report higher satisfaction from greater transparency and easier access to investment data.1

This acceleration doesn’t come at the expense of quality. In fact, automated data processing and validation actually enhance accuracy by eliminating human errors and ensuring consistent application of accounting principles. Whether you’re a venture capital fund administration or managing traditional vehicles, digital tools compress reporting cycles from weeks to hours.

Traditional fund administration models faced inherent limitations when it came to scaling operations. Adding new funds or investors typically requires proportional increases in staffing and resources, creating operational challenges and cost pressures during periods of growth.

Modern fund administration technology breaks this linear relationship between growth and resource requirements. Cloud-based fund administration services can scale elastically as you grow—from managing a single fund in-house to migrating fund admin activities to a third-party platform. This enables administrators to support fund managers through growth phases without service disruptions or quality compromises.

The regulatory landscape for investment funds continues to grow more complex, with new requirements emerging across jurisdictions. Fund administration technology has evolved to address this challenge through automated compliance monitoring and regulatory reporting capabilities.

Advanced systems now use regulatory rules engines to continuously monitor transactions and positions, flagging potential compliance issues early for proactive remediation. This reduces risk and workload for operations teams, replacing manual tracking and sampling with automated, comprehensive monitoring.

The contrast between traditional and technology-enabled fund administration is clearest in operational bottlenecks. In conventional models, tasks like month-end reconciliations, NAV calculations, and investor distributions often create backlogs demanding all-hands-on-deck efforts.

Tech-enabled administrators remove these bottlenecks through automation. Reconciliations that once took days now finish in hours or minutes, with only exceptions flagged for review. NAV runs on set schedules with little manual input, and distributions flow through straight-through processes.

This shift goes beyond speed—it reshapes fund administration. Instead of routine data processing, teams now focus on exception handling, client relationships, and value-added analysis.

Traditional fund administration relied on separate systems for accounting, investor services, compliance, and reporting, leading to integration issues, data inconsistencies, and poor user experiences.

Modern platforms take an integrated approach, spanning all functions to ensure data consistency, streamline workflows, and deliver a cohesive experience. With all data stored in a single ecosystem, administrators can produce comprehensive reports and analytics without the transformation challenges of fragmented systems.

When selecting a fund administrator, prioritize technology infrastructure. Leading partners invest in enterprise-grade platforms that combine reliability, flexibility, and strong security.

Mature infrastructure ensures uptime, processing power, disaster recovery, and robust change management to prevent disruptions. Flexible platforms support diverse fund types, complex structures, and a wide range of asset classes, including alternatives.

Security is critical amid rising cyber threats. Top administrators deploy encryption, multi-factor authentication, access controls, and continuous monitoring, while maintaining SOC 2 and ISO 27001 compliance.

As investment strategies grow more sophisticated, fund structures have become increasingly complex. When considering In-house vs third-party fund administration, look for providers whose platforms already support complex structures like master-feeder and venture capital fund administration.

These systems also scale to diverse investor needs, managing varied fee arrangements, tax treatments, reporting requirements, and side letters, ensuring all investor-specific provisions are accurately implemented and documented.

The technological revolution in fund administration represents both a challenge and an opportunity for investment managers. Those who partner with technology-forward administrators gain significant advantages in operational efficiency, investor satisfaction, and regulatory compliance.

As we look toward the future, tech like AI and machine learning will continue to enhance automation capabilities, while blockchain[1] and distributed ledger technologies may fundamentally transform transaction processing and verification. Data analytics will grow more sophisticated, providing deeper insights into portfolio performance and investor behavior.

For fund managers navigating this evolving landscape, the choice of a fund administration service provider has never been more consequential. By selecting providers with robust, flexible technology platforms and demonstrated commitment to innovation, they can ensure that their administrative capabilities remain aligned with their strategic ambitions—today and into the future.

Disclaimer: THIS MATERIAL IS PROVIDED FOR GENERAL INFORMATION ONLY, DOES NOT CONSTITUTE INVESTMENT ADVICE, AND PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Analysis

Co-sourcing is increasingly being seen as a viable operational model by asset managers. In this article, we break down the fundamentals of co-sourcing, and outline the factors driving its adoption.

How do private markets firms scale operations while maintaining control? It’s a challenge facing CFOs, COOs, and fund controllers as the industry grows in scale and sophistication.

Over the past decade, private capital has become a mainstream asset class, with managers handling larger, more complex portfolios across diverse jurisdictions. The introduction of new fund structures—like continuation vehicles and co-investments—has expanded the toolkit for general partners (GPs) but also intensified operational demands amid rising regulatory pressures and limited partner (LP) expectations.

A 2024 Private Markets Insight Report by Allvue Systems reveals that 84% of private capital firms plan to re-evaluate their operating models within the next 12–18 months, with modular co-sourcing as a key focus. Similarly, 88% of managers at the Fund Operator Summit Europe are exploring outsourcing or co-sourcing in operational areas, particularly in reporting and support functions. Here, we explore the driving forces behind the growing adoption of co-sourcing.

1. Complexity outpaces legacy models

Firms manage more funds, across more jurisdictions, for increasingly diverse investors. Co-sourcing provides the flexibility and transparency needed to navigate this complexity.

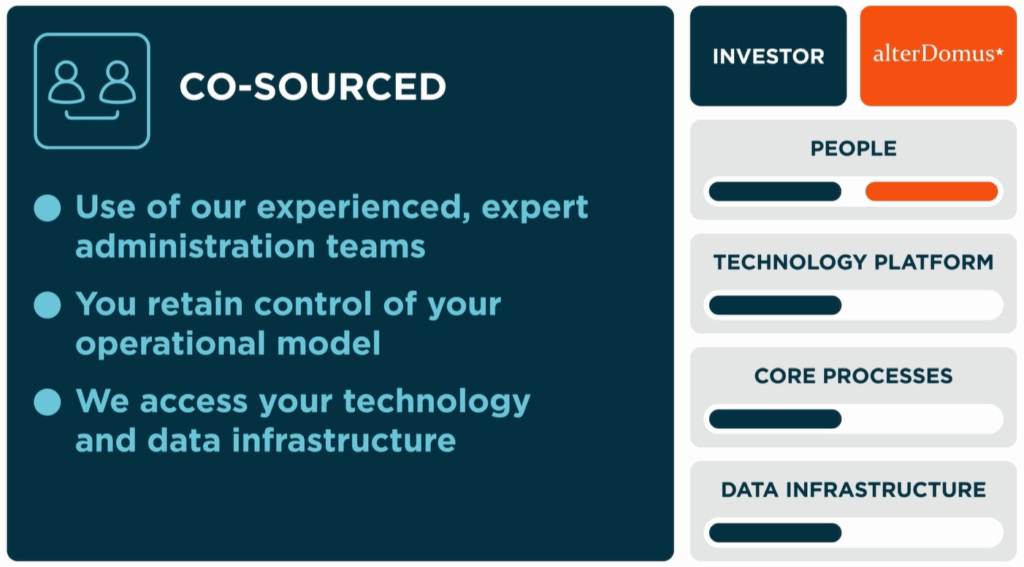

2. Control without Overhead

Managers want to own their data, systems, and client relationships—without carrying the full operational load. Co-sourcing allows firms to retain oversight while shifting execution to trusted partners.

3. Scalable without compromise

As strategies multiply and reporting timelines tighten, operational needs fluctuate. Co-sourcing provides institutional-grade support that flexes with demand, without overcommitting to permanent hires.

4. Enhanced governance and risk management

Regulators demand clear accountability on vendor oversight and operational continuity. Co-sourcing provides transparency into workflows, responsibilities, and data flows, strengthening governance.

5. Rising regulatory burden

SEC Form PF updates, AIFMD filings, ESG disclosures, and tax transparency rules require greater frequency and granularity in reporting. Co-sourcing ensures consistency and accuracy across jurisdictions.

6. Growing LP expectations

Investors want richer insights into performance, fees, and portfolio exposures—delivered faster. Co-sourcing gives managers the back-office strength to meet these expectations while retaining control of the client narrative.

7. Data and platform ownership

Unlike traditional outsourcing, co-sourcing ensures managers keep ownership of their platforms and data, while partners integrate into existing systems to maintain continuity and reduce transition risks.

8. Talent scarcity

Specialist skills in fund operations—such as waterfall calculations or jurisdiction-specific compliance—remain hard to source. Between 2020 and 2022, the U.S. lost more than 300,000 accounting professionals. Co-sourcing provides immediate access to expertise without lengthy recruitment cycles.

To address these challenges, many fund managers are shifting towards a hybrid co-sourcing approach, allowing them to retain control over their systems and client experience while leveraging specialist partners for precise execution.

Co-sourcing with Alter Domus offers General Partners a tailored approach that combines internal oversight with the executional strength of a specialist partner.

Our consultative model allows you to define the scope of support that best fits your unique operational needs, whether it’s fund accounting, capital activity, or regulatory reporting.

By maintaining system continuity and establishing strong governance, we empower your internal teams to focus on strategy while we handle execution efficiently.

Experience the benefits of enhanced operational resilience, regulatory readiness, and access to deep industry expertise.

Contact us today to explore how co-sourcing can elevate your business.

"*" indicates required fields

Analysis

Alter Domus understands that every General Partner has unique operational needs, which is why we offer tailored co-sourcing strategies to enhance efficiency and maintain control. Our expertise allows clients to focus on strategic growth while we manage execution and ensure regulatory compliance.

In the dynamic landscape of private markets, every General Partner (GP) has unique operational needs and preferences. At Alter Domus, we understand that a one-size-fits-all model simply doesn’t work. Instead, we adopt a consultative approach, collaborating with each client to define a co-sourcing strategy that aligns with their specific requirements.

Whether it’s supporting a single process like Form PF reporting or managing full fund accounting cycles within the client’s infrastructure, our flexibility ensures that we meet diverse operational contexts.

Here are some examples of how we empower GPs through customized services and expertise:

By partnering with us, internal GP teams can concentrate on oversight and strategy, while our dedicated professionals manage execution within a clearly defined control framework.

Transitioning to a co-sourcing model doesn’t mean overhauling existing systems or starting from scratch. With years of implementation experience, we guide clients through a structured transition focused on clarity, integration, and flexibility.

Through our extensive work with clients, we’ve identified three key building blocks essential for unlocking the full potential of a co-sourced operating model:

1. Define the right scope: We pinpoint operational areas under pressure, such as:

2. Maintain System Continuity: Clients keep their platforms while we securely integrate into their ecosystem, ensuring a single source of truth and avoiding fragmentation.

3. Establish Strong Governance: We align with each client’s compliance and oversight model, ensuring clear roles, documentation, and audit trails. Managers retain ultimate responsibility, while our teams execute defined workflows according to agreed service-level agreements (SLAs).

| Benefit | How it Helps |

|---|---|

| Internal Oversight | Control over systems, data, policies, and approval processes remains in-house |

| External Execution | Alter Domus executes defined tasks at scale, with speed, accuracy, and rigor |

| Data Ownership | Clients maintain full ownership of their infrastructure and data environment |

| Regulatory Readiness | Respond to changing rules with agile support and specialist knowledge. |

| Investor Responsiveness | Meet LP reporting demands faster and more consistently. |

| Operational Scalability | Expand or contract support without internal hiring constraints. |

| Access to Talent | Tap into deep experience across private equity, private credit, and real assets |

For private markets managers, operational resilience transcends mere business continuity; it’s about forging systems and partnerships that can adapt and thrive in an increasingly complex environment. Co-sourcing provides the perfect balance: the stability of internal oversight combined with the executional strength of a specialist partner.

At Alter Domus, we view co-sourcing as a strategic decision rather than just a service model. It empowers asset managers to focus on what truly matters: creating value for investors, meeting regulatory expectations, and growing with confidence.

If you’re reevaluating your operating model or exploring how co-sourcing could enhance your structure, we’re here to assist. Alter Domus has extensive experience supporting transitions of all sizes and complexities—whether you’re managing a single strategy or adding new strategies.

Our consultative model allows you to define the scope of support that best fits your unique operational needs, whether it’s fund accounting, capital activity, or regulatory reporting.

By maintaining system continuity and establishing strong governance, we empower your internal teams to focus on strategy while we handle execution efficiently.

Experience the benefits of enhanced operational resilience, regulatory readiness, and access to deep industry expertise.

Contact us today to explore how co-sourcing can elevate your business.

"*" indicates required fields

Analysis

Securitisation vehicles are powerful tools that enhance liquidity, optimize risk management, and streamline capital structures. We explore how understanding their complexities can equip you to unlock financial opportunities and stay ahead in today’s evolving markets.

Securitisation has become an indispensable tool for institutions, asset managers, and asset owners. This sophisticated financial instrument offers a powerful trifecta: effective risk management, enhanced liquidity, and streamlined capital structures.

For those contemplating the incorporation of a securitisation vehicle, a comprehensive grasp of this intricate yet potentially lucrative process is crucial. By mastering its complexities, you’ll gain the confidence to navigate challenges adeptly and fully harness the myriad benefits securitisation offers, positioning yourself at the forefront of modern financial strategy.

Securitisation is the process of pooling various types of financial assets, such as loans, mortgages, or receivables, and converting them into marketable securities. These securities are then sold to investors, allowing the originators to free up capital and manage risk more effectively. The cash flows generated from the underlying assets are used to pay interest and principal to the investors.

During 2017 and 2018, the European Union set up rules for securitisations. The goal was to bring the EU securitisation market back to life while also addressing worries about risky practices that had threatened stability after the global financial crisis of 2008. Since it entered into force in 2019-2020, the framework has strengthened investor protection, transparency, and financial stability.1

The European Commission has recently taken steps to revitalize the EU’s securitisation framework to make it simpler, more effective, and supportive of economic growth. These initiatives are part of the savings and investments union strategy, which focuses on improving the way the EU financial system works to boost investment and economic growth across Europe.

Benefits of Securitisation

By converting illiquid assets into tradable securities, institutions and originators can access capital markets and improve their liquidity position. This transformation allows entities to free up resources that can be used for further lending to EU citizens and enterprises.

Securitisation allows for the transfer of risk from the originator to investors, which can help in managing credit risk and regulatory capital requirements. The main goal is to enable banks and other financial institutions to use the loans and debts they grant or hold, pool them together, and turn them into different types of securities that investors can purchase.

Securitisation can lead to lower funding costs compared to traditional financing methods, as it often allows for better pricing based on the risk profile of the underlying assets. Recent EU reforms aim to simplify unnecessarily burdensome requirements and reduce costs to encourage more securitisation activity.

By tapping into the capital markets, institutions can diversify their funding sources and reduce reliance on bank financing. This diversification is particularly important in today’s volatile economic environment.

In some jurisdictions, securitisation can provide regulatory capital relief, allowing institutions to optimize their balance sheets. The European Commission’s recent proposals have estimated a reduction in capital requirements by one-third for senior securitisation tranches, which should encourage new issuances in member states where activity has been limited.

The European securitisation market operates under the EU Securitisation Regulation (EUSR), introduced in January 2019 as part of a comprehensive regulatory response to the Global Financial Crisis.

The Securitisation Regulation amendments aim to reduce operational burdens by simplifying transparency requirements, with plans to cut reporting fields by at least 35%. The revisions introduce more proportionate, principle-based due diligence processes, eliminating redundant verification steps when the selling party is EU-based and supervised.

Notably, the requirement for Simple, Transparent and Standardised (STS) securitisations has been modified to consider pools containing 70% SME loans as homogeneous, facilitating cross-border transactions and enhancing SME financing opportunities.2

Selecting the appropriate jurisdiction for your securitisation vehicle is a critical strategic decision that impacts regulatory compliance, tax efficiency, and operational flexibility. Several European jurisdictions offer competitive frameworks for securitisation vehicles, each with distinct advantages depending on your specific transaction objectives.

The optimal jurisdiction ultimately depends on multiple factors: the location and type of underlying assets, your investor base, anticipated transaction complexity, and specific business objectives. Regulatory changes, such as the EU Securitisation Regulation, have created a more harmonized framework across Europe, though important jurisdictional nuances remain that can significantly impact transaction efficiency.

Decide on the structure of the securitisation vehicle. Common structures includes:

These structures are designed to isolate financial risk and facilitate the issuance of securities. You can choose a bankruptcy-remote structure with a Dutch Stichting or a Jersey Trust, which are most commonly used, or incorporate a vehicle using an entity in your group.

You’ve made the strategic decision to incorporate a securitisation vehicle—now it’s time to navigate the complex legal and tax landscape that comes with it. Have you considered how different jurisdictional choices might impact your bottom line?

Legal and tax considerations aren’t just compliance checkboxes. They’re powerful levers that can dramatically enhance your securitisation structure’s efficiency. Engaging specialized advisors early in your planning process to avoid costly restructuring later.

By strategically selecting your jurisdiction and structure based on your specific assets and investor profile, you can create a tax-efficient vehicle that maximizes returns while maintaining full compliance.

Servicing and Management

Establish a reliable servicing and management framework for the transaction. Effective management and administration of the vehicle by an experienced partner is critical to ensure the correct execution of the transaction.

As the legislative changes removed restrictions on leverage and the nature of the securities permitted as collateral, the SV can now enter into a facility with a credit institution. This is required to acquire the full amount of the contemplated investments, providing greater certainty to the market.

Incorporating a securitisation vehicle represents a strategic opportunity for financial institutions and asset managers seeking to optimize their capital structures, enhance liquidity, and manage risk effectively. The European securitisation market, with its evolving regulatory framework, offers sophisticated mechanisms to achieve these objectives when properly structured.

Partnering with an experienced service provider gives you access to specialized knowledge from structuring and incorporation to efficient implementation and execution to vehicle liquidation.

This collaboration enables you to navigate jurisdictional complexities with confidence, ensure regulatory compliance across borders, and optimize your structure for maximum efficiency and investor appeal. Such expertise has become not merely beneficial but essential for institutions seeking to leverage the full potential of securitisation.

Securitisation is complex and you shouldn’t have to manage it alone. At Alter Domus, we simplify the process with end-to-end expertise, from transaction closing through administration and up to liquidation. With us as your partner, you can focus on strategy and investors while we take care of execution.

Contact us today to learn about how you can unlock of the full potential of securitisation with Alter Domus.

Analysis

Private equity fund structure, at its simplest, uses the limited-partnership model (LPs). This foundational structure defines the roles, responsibilities, and risk profiles of the fund participants.

Within this model, General Partners (GPs) manage the fund and make investment decisions, while LPs contribute the majority of the capital and benefit from limited liability.

At the core of a private equity fund is the limited partnership agreement (LPA), which formalizes the relationship between the GP and LPs. Private-equity funds are typically limited partnerships. GPs commit 2–5% of capital, source and manage deals, and earn fees plus carried interest. The rest is provided by LPs, pension plans, endowments, sovereign funds, and affluent individuals, who receive long-term returns in exchange for limited liability.

Effective private equity fund structuring aligns tax, regulatory, and investor-type considerations by layering feeder, parallel, and co-investment vehicles around a master fund.

A tiered setup lets managers match structures to investor needs. An umbrella (master) fund holds the assets. Feeder funds pool money from specific groups—say, U.S. tax-paying investors or EU institutions—and invest in the master. Co-investment vehicles sit alongside the main fund, so LPs can back single deals, usually at reduced or zero fees.

To serve cross-border investors, managers often run parallel funds in low-tax hubs like Cayman or Luxembourg. These vehicles invest in lockstep with the on-shore fund, so every LP gets identical exposure and performance.

A private equity fund progresses through clearly defined phases. Understanding where a fund sits in its lifecycle helps LPs gauge liquidity expectations, risk exposure, and near-term cash-flow demands.

Over roughly 6–18 months, the GP markets the fund and collects binding commitments. A first close occurs when the target is soft-circled; later closes hit the hard cap. Capital stays with LPs until called, preserving their liquidity.

Most funds last 10 years, with two optional one-year extensions. These extra years give the GP time to exit tough assets. The final phase sees residual holdings sold, audits wrapped up, clawbacks settled, and a last distribution made.

Grasping where a fund sits in this timeline helps LPs match expected calls and payouts to their liquidity plans and risk appetite.

Private equity funds use a pledge-and-draw model—LPs commit capital up front but only wire funds when the GP issues a capital call. This keeps LP cash productive until needed and ensures a disciplined funding process.

Private equity funds use a pledge-and-draw model—LPs commit capital up front but only wire funds when the GP issues a capital call. This keeps LP cash productive until needed and ensures a disciplined funding process.

At closing, each investor signs a subscription agreement—say for €25 million—to be drawn over about five years. The GP issues capital calls only when cash is needed, with every draw taken pro rata from unfunded commitments. LPAs back this with default penalties such as interest charges, dilution, or forced sale of the commitment.

Calls usually arrive by secure email 10–15 business days before funds are due and outline the amount, purpose, and remaining commitment. Many managers provide rolling cash-flow forecasts or cap annual drawdowns to help investors plan liquidity.

Early exit proceeds can be “recycled” during the first few years—often up to 100% of paid-in capital—so the GP can reinvest without raising new money. Recycled amounts are tracked separately, charged fees only once, and after the investment period, any further reinvestment needs LP consent.

Most funds charge an average of 1.74% of committed capital during the investment period. Performance fees remain the classic 20% carry above an 8% preferred return, though first-time or niche managers may discount headline rates to win anchor investors.

Deal fees earned from portfolio companies usually offset 100% of the management fee. Organizational costs are capped (often 1% of commitments), while broken-deal expenses, subscription-line interest, and compliance outlays are also borne by the fund but within budget limits. The true cost to LPs is the net figure after these offsets and caps—not the headline “2 and 20.”

Carried interest is the GP’s share of profits, typically earned after LPs receive a minimum return. The distribution waterfall outlines how proceeds flow from investments to LPs and the GP.

First, LPs get their preferred return. Next comes a short “catch-up” stage where proceeds flow to the GP until its share of profits equals the agreed carry rate. After that, any remaining gains are split 80% to LPs and 20% to the GP.

A deal-by-deal waterfall pays carry on each successful exit, letting the GP collect early but creating higher clawback risk if later deals underperform. A whole-of-fund waterfall waits until the entire portfolio clears the hurdle, delaying GP payouts but giving LPs stronger downside protection.

If early distributions give the GP more carry than it ultimately deserves, a clawback clause forces repayment, usually within 90 days of final liquidation. To avoid messy give-backs, LPAs often escrow some percentage of each carry payment until the last asset is sold, and the results are final.

Understanding these mechanics helps investors gauge when they will see cash returns and how well their interests stay aligned with the GP throughout the fund’s life.

Co‑investments let managers tackle deals too big for the main fund alone, spread risk, and give select LPs a closer look at underwriting. They’re in demand: a 2025 Adams Street survey shows 88% of LPs plan to boost co‑invest budgets.

Most follow‑on money flows through a Special-Purpose Vehicle (SPV) that buys the same shares on the same terms as the flagship fund; investors wire cash within about ten days of notice. Some firms also raise small “sidecar” pools for future deals. Offers go out pro rata to interested LPs, with any leftover capacity filled first‑come, first‑served.

Because LPs assume single‑asset risk, economics are lighter—often no base fee and only 1% management, 10–12% carry versus the standard 2% and 20%. Control stays with the GP, but co‑investors receive richer reporting, and any potential conflict with the main fund must clear the LP advisory committee review.

Secondary deal volume hit $162 billion in 2024, a record, with GP‑led transactions accounting for nearly half. Activity continues in 2025: Neuberger Berman closed a $4 billion GP‑led fund in June, quadrupling the size of its 2020 predecessor.

Continuation funds follow a four‑step process: GPs select strong‑performing assets, obtain an independent valuation and Limited-partner advisory committee (LPAC) approval, run a competitive bidding process, and offer LPs the choice to cash out or roll into the new vehicle. The structure includes capped leverage and a reset waterfall.

Properly executed, a continuation fund can boost near‑term distributions in the selling vehicle, give the GP more time to grow value, and let rolling investors avoid an untimely sale. Mismanaged, it can double‑charge fees or skew track‑record optics.

The key is transparent pricing, recycled carry that reflects genuine performance, and clear disclosure so every party can judge whether staying in—or stepping out—makes economic sense.

Investing in a private equity fund starts with a subscription agreement, where LPs commit capital and confirm eligibility. The Limited Partnership Agreement (LPA) is the core contract outlining the fund’s rules, covering fees, investment limits, governance rights, and removal provisions. Understanding both documents is essential before committing.

Key‑man clauses protect LPs by suspending new investments if certain senior managers leave the fund. This ensures continuity in leadership. Private equity managers also have fiduciary duties—they must act in the best interest of LPs. In the U.S., the SEC enforces these duties. In the EU and UK, regulations like AIFMD and FCA rules ensure similar oversight and transparency.

Private equity funds must comply with regional regulations:

Regulations evolve, so GPs must update LPs and adapt fund operations accordingly.

Navigating private equity challenges—from opaque fee structures to evolving regulations—requires careful review before committing. LPs typically ask the GP how often capital will be called, whether fees fall after the investment period, and when carry is paid. Clarify what happens if key managers leave, how conflicts with co‑investments or continuation funds are handled, and how the firm stays ahead of shifting rules such as AIFMD II or new SEC guidance.

A robust fund pairs plain‑language documents with economics that reward true, portfolio‑wide performance. Fees taper as assets are sold, carry triggers only after LPs recoup capital plus the hurdle, and any recycling or secondary deals are fully disclosed and LPAC‑reviewed. Consistent, data‑rich reporting and a proactive compliance culture keep interests aligned from first close to final liquidation.

Looking to navigate private equity with confidence? Explore our private equity fund solutions to plan for predictable cash flows, fair economics, and long-term alignment.

Analysis

In a market where venture capital firms are navigating heightened deal investment and fundraising uncertainty, managers are ramping up back-office capability to counterbalance front office risk.

Alter Domus reviews how venture CFOs and COOs are building smarter back offices to support the growth and long-term strategic objectives of their firms.

Tim Toska

Group Sector Head, Private Equity

Venture capital firms are facing the most challenging deal and fundraising backdrop in more than a decade. Investment in operational infrastructure is helping managers to navigate it.

In the first half of 2025 global venture fundraising came in at just US$41.6 billion, according to Venture Capital Journal (VCJ), down from US$60 billion over the same period in 2025 and the lowest first half total in eight years. Venture capital investment volume, meanwhile, fell to a record quarterly low of 7,551 deals in Q1 2025, according to KPMG, with the second quarter not much better as a challenging investment backdrop persisted.

A scarcity of LP allocations and transaction flow has thrown venture capital deployment and fundraising schedules out of kilter and intensified competition between managers for capital and deal flow. In the face of these headwinds, operational excellence is becoming point of difference for managers in a competitive market.

A factor in fundraising

For venture firm CFOs and COOs, the growing importance of the back-office as a differentiator when competing for LP capital is a game changer.

Historically the primary predictor of fundraising success was front office excellence and track record, and the ability of managers to identify and execute on the best deal targets and maximize investor returns. The back office was a necessary but primarily administrative function.

This has been a catalyst for the traditional siloes between the back office and front office breaking down. Operational infrastructure is now a key enabler of front office success, with the CFO and COO setting this interface and participating in the implementation of technology and service provider support to build out of centralized operational processes and data infrastructure that underpin core front office functions.

Indeed, due to the increasing sophistication of the LP base, LPs are paying closer attention to back-office capability when deciding which managers to allocate limited capital resources to. According to Private Funds CFOs 2025 Insights Survey, 36 percent of respondents said LPs were paying closer attention to operational and infrastructure capabilities – up from 22 percent a year earlier.

A robust operating model is seen as a risk mitigator for LPs when selecting managers, as LPs require the managers they back to have the right people, processes and technologies in place to support strong governance and protect firms against downside risk. Alter Domus has noted a steady increase in due diligence requests from investors and prospective investors. These have involved calls, questionnaires and onsite visits to fund administrators.

A sound operational model is also a key enabler for managers to scale as they stay on top of ever-changing fund structures, co-investment, SPVs, continuation vehicles and special account fund structures.

The venture ecosystem hasn’t been isolated from trends reshaping the wider private markets space, where a wider mix of investors, with varying returns objectives and tax and regulatory obligations, comprise a manager’s core LP base. This includes servicing a potentially growing base of non-institutional investors allocating to venture strategies through semi-liquid and interval structures, which require the management of liquidity sleeves and the more regular publication of net asset value (NAV) marks. Venture managers have been pioneers in development of evergreen and permanent fund structures. Blue chip venture managers, including Sequoia and Thrive Capital, are among the venture firms to have launched permanent capital funds with indefinite fund lives. Some of these funds can hold public stocks, a natural fit for early venture investors in what are now some of the world’s largest companies.

In a market where liquidity is at a premium (distributions as proportion of private markets NAV well to 11 percent in 2024, the lowest percentage in a decade, according to Bain & Co analysis, LPs are also placing premium on managers with the back-office capability to manage capital calls and distributions with maximum efficiency.

Cash-constrained LPs will not want to face capital calls too early or have cash locked up unnecessarily because of a premature call. LPs will also note which managers can expedite timelines for distributions. With distributed-to-paid-in (DPI) now almost as important as IRR for LPs when backing managers, the way firms handle cash management processes, capital calls and distributions, has been elevated from relatively low value, administrative work to a key differentiator for LPs.

The speed of capital calls can also present a venture firm as more attractive in competitive deal auctions and funding rounds. In a deal environment that is low volume and more competitive, having an efficient cash management model (opening accounts, issuing capital calls, funding deals) that doesn’t create a bottleneck or pose as a risk area can make the difference in winning or losing a deal.

Venture regulatory and reporting demands are also intensifying. In addition to meeting LP expectations for more frequent and granular reporting on fund and portfolio company performance, venture firms are also having to steer through regulatory change, with the next iteration of the EU’s Alternative Investment Fund Managers Directive – AIFMD II – applying from April 2026, and the US Securities and Exchange Commission (SEC) issuing record levels of financial penalties in the 2024 fiscal year. With data privacy regulation and environmental, social and governance (ESG) compliance also on the venture manager to do list, the regulatory and reporting ask of venture firms has never been more demanding.

The challenge of scaling the back-office

For the venture CFO and COO, who are responsible for laying the foundations and strategic direction of their franchises, an innovative approach to overhauling old expectations of how a firm’s venture back office looks and operates has become necessary to put firms on the right trajectory.

Keeping up with the expanding expectations of the venture capital back-office presents significant cost challenges and complexity for managers, and it is the responsibility of the CFOs and COOs to lead the organizational transformation required to keep their firms in tune with changing market dynamics.

Venture firms have long-operated as nimble, efficient partner-led organizations focused predominantly on deal execution and fundraising. Back-office requirements were relatively light touch and could be handled by small, inhouse teams.

In the current market, CFOs and COOs are under the pressure to determine the best course of action; continue with the in-house model and invest in hiring and growing the team, along with implementing technology to manage increasing operational workload; or partner with service providers.

Exploring the options: insourcing vs outsourcing

Historically venture managers have been slower to adopt an outsourced model than other asset classes. Venture structures have been relatively straightforward to administer, especially for emerging managers where structures may be simple and the volume of investors per fund small enough to manage effectively inhouse. For many of the smaller VCs, cost sensitivity has been another factor for insourcing.

There is also a sensitivity around confidentiality. Several venture deals will be confidential, which has led to some nervousness about sharing too much information with third-party service providers.

The insourcing model, however, does present challenges that venture CFOs and COOs have to consider.

To keep up with increasing complexity, investor expectations and regulatory demands, back-office teams are leaning more and more on technology, software, process automation and AI tools. Advances in technology will also be led by many of the companies that venture managers have invested in and are familiar with. As a result, venture managers will be more familiar and comfortable with automation, AI and new technology, and will find technology more valuable and easier to implement.

The private markets industry has already embarked on this technology trajectory, with an industry survey led by Alter Domus and Deloitte recording that well over half of managers are already utilizing digitization and automation in daily operations, and that almost 63 percent anticipate that AI and GenAI will have a significant impact on the alternative investment industry. The survey found that respondents saw streamlining operational processes, enhancing decision-making capabilities, and increasing portfolio performance areas where digitization and tech-adoption should focus.

Keeping pace with tech adoption, upgrading and transitioning legacy technology platforms, and training and recruiting back-office teams that are fit for purpose, however, requires significant upfront capital expenditure that can prove overwhelming for venture managers – especially if this investment would otherwise have been directed into core front office dealmaking resources and recruitment.

According to VCJ, the average venture fund in H1 2025 closed at US$124.5 million, the lowest average recorded in six years. With smaller funds and fee income than other private markets strategies, such as buyouts or private credit, venture firms will often lack the budgets to add to inhouse teams, invest in new technology platforms and retain back-office staff who are being stretched as reporting and regulatory workflows increase.

Outsourcing presents a solution to these capital expenditure and tech-adoption bottlenecks.

Outsourcing fund administration specialists service thousands of managers and funds, across multiple asset classes and geographies, and are thus able to achieve economies scale that enable them to deliver high-value fund accounting, fund administration and investor services as significantly lower costs than an individual venture manager in isolation.

Fund administrators will also be engaging with regulatory and technology developments, on behalf of clients, on a daily basis and have the scale to deploy dedicated teams with deep expertise in these areas to support venture clients.

Outsourcing providers can also advise venture managers on the software and technology platforms best matched to a manager’s deal strategy and investor base, and leverage relationships with technology vendors to roll-out bespoke solutions at competitive price points that can be benchmarked by LPs.

Fund administrators can also provide venture clients with access to proprietary and automation tools that are fit for purpose, allowing managers to reinvest in other aspects of their business. Alter Domus, for example, has invested significant capital in data analytics and workflow automation, which clients can use to drive efficiencies across the back-office. Clients using these tools have reported efficiency gains of between 10 percent and 20 percent.

The evolution outsourcing

The fund administration industry, however, has recognized some of the challenges presented by “old-fashioned” outsourcing arrangements and has tailored services that allow venture managers to retain the ready access to data and institutional knowledge that an insourced model provides, at the same time as unlocking the cost-efficiencies and scale that an outsourced model can offer.

Fund administrators can now provide co-sourcing operating models where data is held in a cloud environment, rather than behind an administrator firewall, and can be accessed by both manager and fund administrator as required.

For CFOs and COOs this removes the friction points of going back and forth to an administrator when fielding LP information requests, but still gives the manager the back-office scalability and cost advantages of an outsourced model.

In addition, co-sourcing makes it easier to switch administrators if a manager chooses to, as the manager retains control of the platform and software its back-office data is running on.

Lastly, another outsourcing model that growing managers have found compelling is the “lift out”. This involves a number of the manager’s incumbent team leaving and becoming employees of the fund administrator, while continuing to support the same funds they covered in-house. Institutional knowledge isn’t lost, and the manager retains continuity of the team servicing the funds, while putting in place a more scalable and cost-effective operational model for the future.

Building partnerships

As the venture capital ecosystem faces an operational inflection point, where operational infrastructure evolving from a back-office matter to strategic differentiator, working with a tech-enabled fund administration provider can help venture managers to level up their back-office capability without drawing resources and senior partner attention from the core business of raising and deploying capital and delivering returns to LPs.

Relationships between managers and outsourcers, however, are deepening and becoming more sophisticated, to best meet manager requirements.

A fund administrator is no longer just providing arms-length services and basic support, but serving as long-term partner to managers as their operational requirements develop and change.

Managers will now turn to their fund administrators for advice on the optimum operational model for their organization and support on how to execute business transformation, manage data migration and implement new systems. Fund administrators will also advise on the technology and software that best dovetails with a manager’s operational model and keep managers up to date on regulatory and compliance requirements.

A fund administrator like Alter Domus can provide genuine strategic value to venture capital CFOs and COOs as they navigate the shifting industry backdrop, serving not just as provider of basic support functions, but as an important partner and counsel.

Analysis

Venture capital investment has grown strongly through the first quarter of 2025, despite a volatile macro-economic backdrop. AI investment has been the primary engine of the asset class’s resilience, but other sector themes have also driven deal flow.

Tim ToskaGroup Sector Head, Private Equity

In the face of volatile stock markets, tariff uncertainty and sustained elevated interest rates venture capital investment has proven remarkably resilient. In the first three months of 2025 global venture investment reached a 10 quarter high of US$126.3 billion and up 53 percent year-on-year from US$82.3 billion in Q1 2024, according to KPMG figures.

Investment in AI and machine learning technology funding rounds has been the single biggest driver of venture capital investment resilience, accounting for close to 60 percent of combined venture deal value in Q1 2025, according to Pitchbook.

But while the importance of AI to the health for the venture deal ecosystem in the current market is undeniable, but behind the AI-driven headlines, other sectors are also generating and interest and deal flow.

Alter Domus reviews five key sectors attracting investment from venture capital managers:

1. AI and machine learning:

Without the contribution of AI funding round activity, overall venture capital funding round investment figures would have come in much weaker.

AI has been a hot ticket for investors, with the long-term growth trajectory and application of AI technologies supporting robust valuations and investor appetite for exposure to fast-growing AI start-ups with proven technologies.

The US AI space has been particularly active, with OpenAI, the developer of ChatGPT, closing the largest private tech in history with a US$40 billion funding round that valued the business at US$300 billion. In other US AI deals large-language model (LLM) competitor Anthropic raised US$4.5 billion across two closings and AI-powered augmented reality company Infinite Reality raised a US$3 billion round to lock in a US$12.5 billion valuation.

AI investment activity also corner-stoned the European venture market, although the focus was more on AI-industrial applications as opposed to the LLM deals that led the US market. Healthcare-led AI companies such as Neko Health and Cera landed funding rounds of US$260 million and US$150 million respectively.

AI also animated Asian venture capital, with the release of Chinese LLM AI company DeepSeek, which can operate with less computing power than other models, opening up AI to a wider pool of users and driving Asian technology giants Alibaba and Tencent to launch their own AI-offerings.

2. Healthtech and biotech:

The healthtech and biotech segment also showed positive investment growth, rising by 30.4 percent in Q1 2025 to reach US$3.5 billion from 185 transactions.

Investment in health and biotech has benefitted from overlaps with the red-hot AI sector, with numerous large funding rounds secured by businesses straddling both segments, such as the abovementioned deals involving preventative healthcare group Neko Health and in-home care platform CERA.

But while AI shaped investment in healthtech and biotech, other sector verticals have also managed to progress funding rounds. Windward Bio, for example, a clinical stage drug developer, landed a US$200 million Series A funding round, while FIRE1, a medical devices developer focused on heart failure care, landed a US$120 million round.

Other funding rounds – for companies spanning a range of therapeutic drug research, digital health technology and scanning and drug delivery areas – have also progressed, illustrates the sustained interest in the healthcare space from venture capital investors.

3. Cleantech

Despite policy shifts in the US on energy transition and environmental, social and governance (ESG), cleantech and climate-focused assets have continued to attract interest from investors.

Even as the policy focus on energy transition shifts, venture capital investors around the world have continued to bank on the long-term requirement for diversified energy sources, energy security and decarbonization in all modern economies.

In the US, X Energy, a developer of small, modular nuclear technology, raised US$700 million in an upsized Series C funding round, while Helion, a fusion reactor business, raised US$425 million in a Series F round.

Outside of the US, Chinese cleantech group SE Environmental secured a US$688 million round, while German real estate energy management company Reneo and Australian vertical farming group, Stacked Farm, closed rounds of US$624 million and US$150 million respectively.

4. Defencetech

Escalating conflict in Eastern Europe and the Middle East, coupled with a shift to satellite-, autonomous- and AI-powered defense system has supported a strong growth in defencetech venture investment, with CB Insights forecasting that at the current run rate defencetech investing will reach US$6 billion by end of 2025 – a 62 percent increase on 2023 levels.

In Europe funding round highlights have included sizeable funding rounds for Defence AI software company Helsing and drone manufacturer, Tekever. The US generated even bigger defensetech deals – including a $600 million raise by autonomous naval defense technology group Saronic Technologies, a $240 million raise for aerospace-focused ShieldAI, and a $250 million raise by anti-drone systems developer Epirus.

5. Fintech

The fintech sector has been focused on the exits and realizations of existing assets, but investment opportunities have continued to emerge, with CB Insights tracking an 18 percent quarter-on-quarter increase in fintech funding to US£10.3 billion for Q1 2025.

A rally in investment in crypto and blockchain assets, including large rounds such as the US$2 billion deal for Maltese crypto exchange Binance, contributed to the increase in fintech investment, with a number of crypto assets also testing out markets for exits.

Outside of the crypto and blockchain space, Mexican buy-now-pay-later (BNPL) platform Plata secured a US$160 million round to achieve unicorn status, while Israeli fintech services provider Raypd landed a US$500 million round to support its acquisition of PayU.

Other areas to watch:

In addition to the core investment themes listed above, venture managers have also kept tracking longer-term investment trends. These are other investment themes to watch:

6. Quantum computing:

Quantum computing – an advanced form of computing based on the principles of quantum mechanics – has the potential to solve calculations and complex problems that current computing systems can’t deliver.

The sector is still relatively nascent, but venture managers are moving actively to build exposure to the sector, with quantum computing groups raising more than US$1.25 billion in Q1 2025 – more than double the year-on-year comparison.

As the sector moves into the commercial domain, and is not solely used in a research and development context, more commercial applications and investment opportunities are opening up.

7. Graphene:

Graphene – a feather-light but incredibly strong substance with huge potential across the construction, manufacturing and industrials sectors – is expected to grow at a compound annual growth rate (CAGR) of 35.1 percent between 2024 and 2030 and become a US$1.61 billion market, according to Grand View Research.

Compared to other venture verticals, funding rounds are still relatively small, but with demand for the substance expected to increase across the energy storage, aerospace and car-making industries, this is an area venture firms are going to be paying ever closer attention to.

8. Synthetic biology:

Synthetic biology – a science applying engineering principles to living systems – has the potential to transform the availability of personalized medicine and food production and is forecast to grow at a compound annual growth rate (CAGR) of 23.2 percent between 2025 and 2035, according to Vantage Market Research.

Venture capital players have invested steadily in synthetic biology research, but commercial applications are still some way off and transitioning the sector from one receiving steady private sector capital flows at seed level, into a sector the presents an attractive risk-reward proposition for venture investors deploying scale-up levels of capital is still some way off.

9. Robotics:

Venture investment in robotics has cooled since 2021, when funding rounds totaled US$14.7 billion versus around US$7.5 billion last year, according to Dealmaker reports.

The sector, however, has continued to attract sizeable, albeit concentrated funding rounds, as companies combine physical robotics capability with AI tools.

Physical Intelligence, for example, a start-up that develops “brains” for robots secured a US$2 billion valuation when closing its recent US$400 million funding round.

In another notable deal Apptronik, a humanoid robotics company based in Texas, closed a Series A funding round at US$350 million. The company is building intelligent robots that can be deployed in the manufacturing, health care and social care sectors, among others.

Analysis

Headline venture capital investment figures point to an asset class in rude health, but in reality, the picture is more complex. Alter Domus reviews the drivers behind strong investment levels and why some parts of the venture market and performing better than others.

Tim Toska

Group Sector Head, Private Equity

At first glance, the global venture capital market appears to be booming.

Venture capital investment in Q1 2025 climbed to a 10-quarter high of $126.3 billion, rising from $118.7 billion in the previous three months, according to KPMG; some 35 Unicorn assets (start-ups valued at US$1 billion or more) were formed through the quarter, the second highest quarterly total since 2023, according to Pitchbook, and generative AI platform OpenAI landed a record setting US$40 billion funding round at the end of March.

These headline numbers, however, do not tell the full story. Overall venture investment may appear strong, but the asset class has not escaped the fallout from elevated inflation and interest rates, stock market volatility and global trade uncertainty.

Investment value is up, but venture capital deal volume is down. In Q1 2025 only 7,551 deals crossed the line, down from 8,801 deals in the previous quarter and a record quarterly low, according to KPMG. Meanwhile, a Bain & Co analysis shows a 23 percent year-on-year decline in venture capital fundraising, with Pitchbook recording a year-on-year decline in venture capital exit value, which totaled US$322.8 billion in 2024 versus US$331.2 billion in 2023.

A two-tier market

The gap between robust investment activity on the one hand, and falling fundraising and exit value on the other, reflects the emergence of a two-tier venture market that is bifurcating by sector and size.

Perhaps the starkest contrast to emerge is the widening disparity between the red-hot levels of deal activity involving AI-linked companies and start-ups in other sectors.

Indeed, close to a third of total funding round activity in Q1 2025 was generated by the mega OpenAI funding round, with large-language model AI start-up Anthropic another heavyweight contributor to headline numbers, landing a US$4.5 billion funding round raise. Other companies with specific AI-linked capabilities, including KoBold Metals, a developer of AI-powered mining exploration tools, and AI healthcare company Cera, were among the other high-profile performers.

The dominance of AI and machine learning has been such that it accounted for 57.9 percent of combined venture deal value – an all-time record share of the market, according to Pitchbook.

There have been a few other bright spots in the market, most notably in European defense-focused groups, with the Nato Innovation Fund and Dealroom recording a 24 percent rise in investment in European startups focused on developing defense and defense-related technology. Drone maker Tekever and defense software company Helsing have been among the big winners, as European governments and business ramp up defense spending in response to the ongoing Ukraine war.

Investors and dealmakers appear to be doubling down on select segments of the market, upping investment in these areas while putting investment in other areas on hold until macro-economic uncertainty abates. This is one of the main reasons for falling investment volume at time of rising investment value.

Fundraising falters

Macro-economic volatility has also impacted venture capital in a similar way to the buyout space, with volatility making it increasingly difficult to exit portfolio companies at attractive pricing, which then limits the distributions managers are able to make LPs, who in turn have to put the brakes on supporting new fundraising until managers start returning more cash to investors.

This dynamic has shaped what has been a tough fundraising market – which is expected to remain challenging in the near-term as a much anticipated “exit window” is pushed back yet again.

Venture dealmaker had entered 2025 with quite confidence that the year ahead would herald an improving environment for exits, with IPO markets (a crucial exit channel for venture-backed assets) set to reopen as inflation pressures eased and interest rates assumed a downward trajectory.

Escalating trade tension and tariff uncertainty, coupled ongoing conflict in Ukraine and the Middle East, and associated stock market volatility, however, have pushed back any optimism for a wave of exits back to the second half of 2025 at least, or even into 2026.

Venture-backed companies that have test the IPO waters have struggled to land successful listings at stable prices, while other venture portfolio assets that had been gearing up for big-ticket IPOs have delayed their prospective listings due to market uncertainty.

Exiting via funding rounds involving larger venture firms has also been testing, with Pitchbook noting that in the US – the world’s largest venture ecosystem – more than a quarter of funding rounds in Q1 2025 were flat or down rounds (where a start-up raises money at a lower valuation than in previous funding rounds).

There are signs that trade tariff dislocation may be abating, and stock markets have recovered losses from earlier in the year, laying a firmer foundation for potential exits through the second half of 2025. Markets, however, are still choppy, and it will take time for managers to build the necessary comfort to put companies on an exit pathway.

Opportunities ahead… but uncertainty lingers

Through this period of dislocation, opportunities to invest in high-quality, high-growth venture assets will continue to emerge. AI will more than likely continue to dominate deal activity, although defense and cybersecurity startups will also be high on dealmaker target lists.

Other sectors will also present compelling investment opportunity, although in smaller volumes, with cleantech and fintech the sectors outside of AI and defense that dealmakers are keeping an eye on.

Until there is a sense of wide macro-economic stability, however, the bifurcation theme that has shaped the venture investment during the last 12 months will continue to set the tone for market activity through the rest of 2025.