News

The dust has settled on SuperReturn, the conference at which the world’s leading asset managers, investors and fund administrators gather annually to opine on the state of the industry. Now back from both hosting and attending panel sessions and giving keynote speeches in Amsterdam, Alter Domus leading lights Bruno Bagnouls, Patrick McCullagh and Tim Trott outlined some of the key themes and discussion points from the event in an Alter Domus roundtable interview.

Bruno Bagnouls: Gentlemen, that was an intense three days of debate and discussion at SuperReturn and alternative markets seem set for an interesting ride in 2024. Tim, let’s start with you. Here at Alter Domus it’s vital that, as a leading fund administrator, we keep a watchful eye on what’s happening on the regulatory front. You attended one of the lead sessions on this topic – what were your big takeaways?

Tim Trott: Well, we live in a time of constantly shifting sands on the regulatory front, and there were several issues that are generating some market apprehension and uncertainty. Firstly, Article 8 of the Sustainable Finance Regulation Disclosure mandate. Now, Article 8 refers to funds promoting environmental and social objectives which take more into account than just sustainability risks as required by Article 6. However, part of the issue is that Article 8 funds don’t have ESG objectives or core objectives. And there is market concern that this lack of backbone to the regulation and with SFDR could lead to what’s referred to as greenwashing on top of generating extra costs for that fund.

Secondly, on the challenging acronyms front, the incoming Alternative Investment Fund Managers Directive 2 was discussed as you’d expect. Otherwise known as AIFMD II, it was highlighted how AIFMD II’s control of cross-border marketing for funds is squeezing mid-market managers out of Europe, disincentivizing new players and, at the very least, increasing the administrative burden for market participants.

Bruno: Broadly speaking, Tim, ESG considerations do look set to become an ever more intrinsic part of raising, investing, and administering capital as time moves on. Moving on, Patrick, we listened in to the rather lively panel session on choosing a home to domicile your fund – what were the main insights?

Patrick McCullagh: This is, quite understandably, always a hot-button topic in the industry, Bruno. To stretch the metaphor, whether your fund is a bungalow or a palace, where you lay the foundations can make a huge difference. Key points to note were that from a jurisdictional perspective, Luxembourg remains an incredibly attractive EU option, not only for tax reasons, but because it has the largest cross-border funds distribution. It does also seem that Brexit has been somewhat of a boon for Lux, with more fund business migrating there. On the downside, issues were raised around appropriate infrastructure investment regarding banks and law firms, with Guernsey being flagged as comparatively better equipped in this area. Elsewhere in Europe, Switzerland was highlighted as a challenging place to domicile.

Beyond the EU, we have all of course been following the fall-out from the ‘black-listing’ of the Caymans, and how this has also pushed some US players towards Lux. That said, the panel outlined that for most, the risks associated with the Caymans are acceptable. Investors are still comfortable with the familiar and see the black-listing as likely to be short-term. There are also a lot of investment strategies that involve certain risk thresholds in industry or jurisdictions, especially emerging markets where other well documented risks make it almost irrelevant.

Bruno: And of course, many of these issues highlight just why it’s important to have fund administrators that have both local and cross jurisdictional expertise. Sticking with funds, Tim, day two of SuperReturn kicked off a look at fundraising trends. What was the general sentiment?

Tim: There are some clear challenges in this area, Bruno. While Covid was obviously terrible for the planet at large, fundraising was generally easier in that period. In this current period, fundraising is taking a lot longer, partly I’m sure because of the ongoing uncertainty that high interest rates and inflation caused. However, funds are both getting bigger generally with fewer smaller players entering the market. No matter their complexity, investors certainly aren’t being turned away at the door as that need for capital is swelling.

Patrick: Just to add to more weight to Tim’s point there, I attended a session on the evolving role of CFOs and it was acknowledged that fundraising would continue to be trickier for the foreseeable future.

Tim: Industry data and insights company Preqin also hosted an outlook session on alternative markets and they forecast growth to slow globally in terms of assets under management, as well as highlighting an apparent disconnect between fund targets and actual funds. It’ll be interesting to see what happens when shifts start occurring at the macro-economic level.

Shifting from fundraising to existing funds, one other point that jumped out at me at the CFO session was the comment that the implementation of IT and digitalization in general being much harder for larger or more vintage funds.

Bruno: Tim, that’s a nice segue into the fact that Patrick hosted a ‘Let’s talk tech’ panel at the event. Investment in and use of technology seems to be in everyone’s minds and plans right now.

Patrick: 100% right, Bruno. I’d say that we really are now at the beginning of what we at Alter Domus would call the third generation of fund operations, with technology coming to fore. Automation, AI and machine learning are certainly going to have a somewhat seismic impact on the industry, as will the end-to-end digitization of workflows.

From a back-office perspective, it doesn’t matter if it’s data collection, data processing, or data distribution, the days of throwing ever larger number of bodies at a problem – and using blunt, legacy tools like Excel – are going the way of the Dodo. It always comes back to a question of scale: the ability to grow your business, grow the number of funds and accurately administer that fund, monitor that fund’s performance, and derive investment insight from that fund data is increasingly going to come down to the smart integration and application of best-in-class technologies. Everyone on my panel agreed that standardized, comparable, accurate data that can be swiftly deployed downstream to the analytical arms of a business is vital.

Tim: Of course, the other factor driving this is the increasing demands of investors. Their reporting demands are growing, as is their need to understand the infrastructure of an asset management house being the third parties that they engage with and technology solutions used throughout the structure before they consider partnering.

Patrick: Absolutely. And this is also where administrators like Alter Domus are taking a leading role in the development of new technologies for fund administration, data extraction, portfolio monitoring and beyond. This helps insulate managers from steep tech development costs, risks, the time to market needed to do it themselves, or to retro fit new technology to ‘legacy’ operations. The future really is now.

Luxembourg

Director, Alliances and Partnerships EMEA

United Kingdom

Managing Director, Sales, Europe & United States

United Kingdom

Director – Head of Corporate Services – United Kingdom

News

Artificial intelligence and machine learning have the potential to be game changers for private credit and fund administrators. Alter Domus’ Head of Automation and AI, Davendra Patel told PDI’s “Future of Private Debt” report, boosting everything from deal sourcing to ESG reporting.

Although early adopters are seeing the benefits of integrating artificial intelligence and machine learning into their fund management workflows, the game-changing potential of the tools remains largely untapped in private credit — but probably not for long, according to experts who spoke recently with PDI for their recently published “Future of Private Debt” report.

The group included Davendra Patel, Head of Automation and AI at Alter Domus.

The sector is gradually embracing AI and machine learning for good reason: the technology can help with investment strategy and back- and middle-office functions alike, everything from deal sourcing and due diligence to investor and ESG reporting.

One of AI’s strengths is its ability to discern patterns from thousands of data points, and to do it in a fraction of the time it would take a team of people to do it, and without the risk of human bias. Of course, it takes human judgment to draw a final, well-considered decision out of the data, but AI can improve the confidence around it.

Alter Domus spent four years creating its own AI systems, including a proprietary version of ChatGPT. According to Patel, the company’s in-house capabilities, which have been deployed across Alter Domus’ entire business, help clients simplify and automate complex processes.

Among other things, Alter Domus automation reads emails, removes attachments, and automatically classifies, extracts, and summarizes the information. Clients have access to real time insights — something investors have been clamoring for. What’s more, Alter Domus’ proprietary tools mitigate the security risks often associated with off-the-shelf digital solutions.

Europe

Head of AI & Automation

Conference

Uncover the latest trends and developments in the securitization industry by joining our team at IMN’s ABS EAST Conference in Miami from October 23-25. Our team looks forward to meeting you at the Alter Domus sponsored conference to discuss leveraged loan and CLO markets, non-bank lending, ESG frameworks, and many other topics shaping structured finance. Our attendees include:

Attend the conference to gain exclusive insights from Tim Ruxton and Greg Myers during their panel sessions.

Greg Myers will be moderating the “CLO Manager Perspectives” panel on October 24th at 4PM EST, while Tim Ruxton will speak on the “Leveraged Loan Market” panel on October 23 at 2PM EST.

Be sure to connect with our team ahead of the conference to learn more about Alter Domus’ range of structured finance solutions.

United States

Head of Sales & Relationship Management North America

United States

Managing Director, Sales, North America

United States

Global Sector Head, Debt Capital Markets

United States

Managing Director, Sales, North America

North America

Managing Director, Sales, North America

North America

Managing Director, Sales at Alter Domus North America

No related content found.

News

Considering the transformational possibilities of artificial intelligence on fund operations —the right applications can do everything from reduce costs to help generate new revenue — it may come as a surprise that only 14% of fund executives surveyed by information service Private Funds CFO have implemented AI technology into their portfolio companies. Perhaps more startling is that more than half of respondents said they had no plans to adopt AI in the next year.

For Alter Domus Head of AI and Automation Davendra Patel, that looks like a missed opportunity, especially with areas such as risk management, due diligence, and performance tracking ripe for AI integration.

In a recent interview with Private Funds CFO, Patel said that in the current economic climate, AI is a pivotal tool for gaining a competitive advantage. That’s a view his own company has taken to heart: Alter Domus has created its own versions of ChatGPT and integrated generative AI to automate data from various sources, providing real-time information and insights to clients.

Patel, who has 30 years of experience in IT, acknowledges the potential security risks around AI, including the threat of shared information becoming leaked information. By developing proprietary tools, Alter Domus has optimized data safety. In addition, in-house experts continuously monitor the Alter Domus system for vulnerabilities and breaches.

“We focus on regular reviews, audits, and ethical considerations to ensure AI’s responsible and safe deployment,” Patel told Private Funds CFO.

“It’s essential to balance AI’s potential with practicality, focusing on both immediate gains and long-term benefits.”

Read the full article here.

Europe

Head of AI & Automation

Analysis

Calm after the storm

After more than 36 years of existence, the London Interbank Offered Rate (LIBOR) was discontinued in July 2023 in favor of alternative references rates, such as SOFR (Secured Overnight Financing Rate). As mentioned in previous Alter Domus reports, we discussed the need to migrate away from LIBOR and provided updates on the transition as the cessation date grew closer.

Now that LIBOR is no longer published, we report on the impact it continues to have, albeit declining, in the U.S private debt market and address any lingering considerations.

Announcement of LIBOR’s future discontinuation in 2017 posed an intimidating feat, like an impending storm, as LIBOR was pegged to almost all contracts accounting for billions of dollars of debt. Six years later, though, market participants made it through the storm quite successfully.

Overall, the LIBOR transition was, as the AARC[1] puts it, “smooth and uneventful.”[2] Much of the success is attributed to the careful planning and coordination between agents, like Alter Domus. borrowers, lenders and financial regulators.

Moreover, as the June 30,2023 deadline approached, there was a predictable uptick in credit agreement amendments and triggering of existing ones. As reported by the LevFin Insights, amendments spiked in June, nearly totaling 300, representing almost 3 times the amount of amendments in May and April[3].

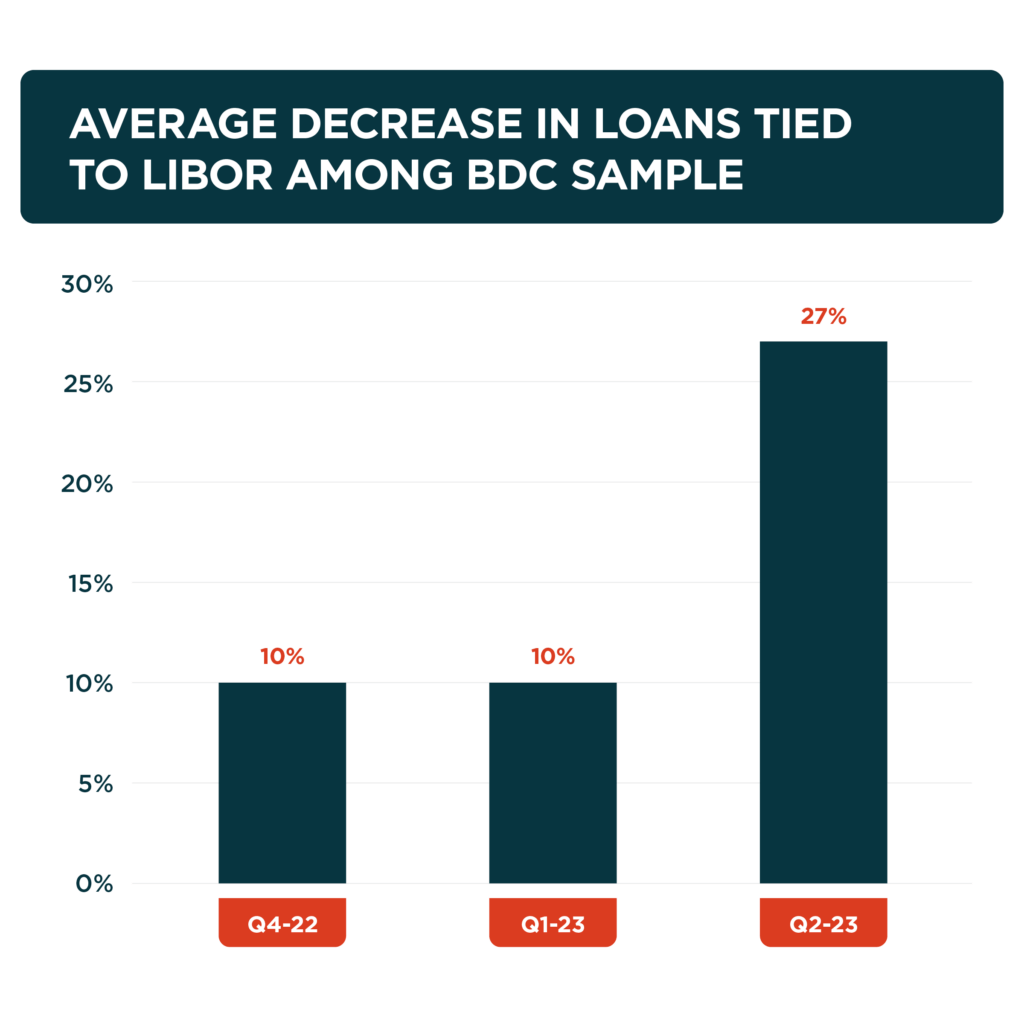

The same can be inferred with respect to the direct lending space, as we turn to publicly available BDC (Business Development Companies) data as a proxy. From a sample of 13 BDC’s registered with the SEC, representing over $33bn in portfolio valuations or about a quarter of the publicly traded BDC market, we observe from the 2023Q2 SEC filings that the average decrease in loans tied to LIBOR jumped to 27% during 2023Q2 from 10% in 2023Q1.

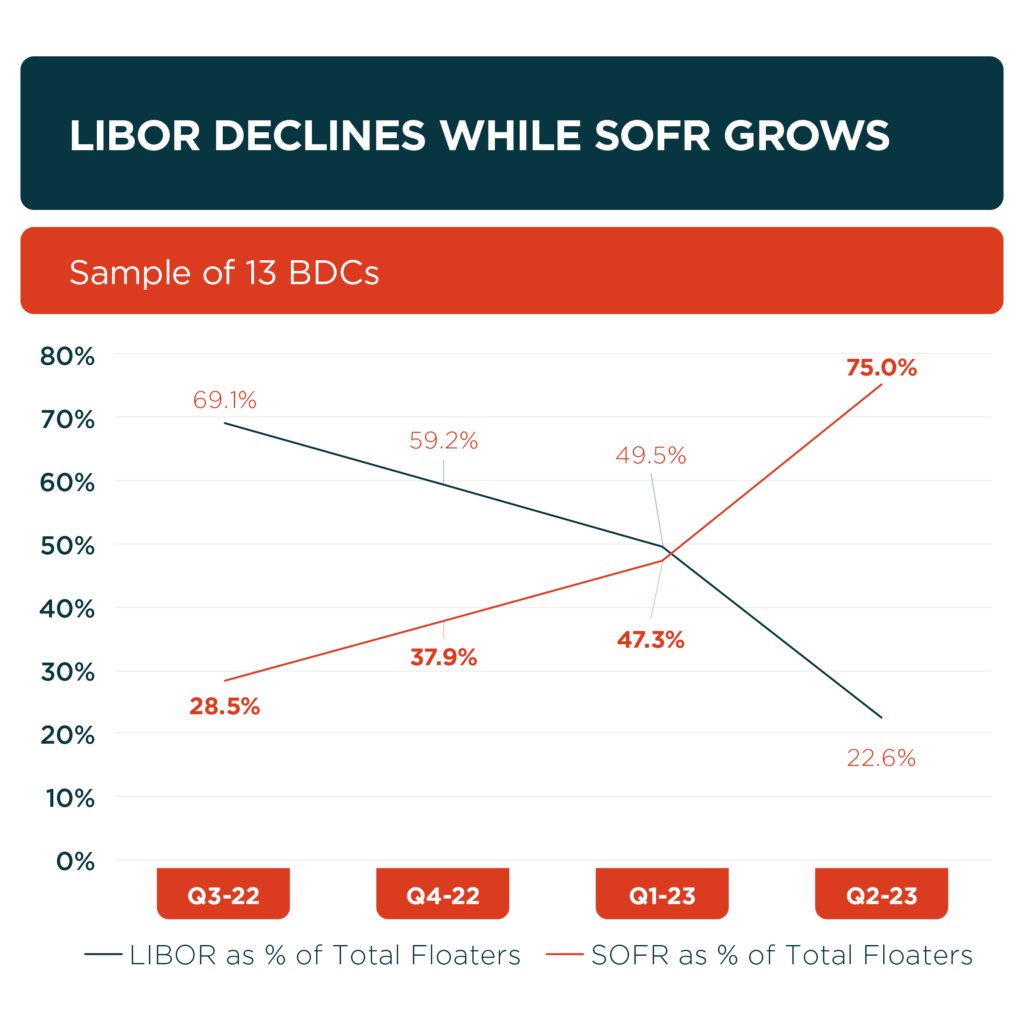

The graph and table that follow clearly illustrate the declining relevance of LIBOR and rising relevance of SOFR in the last four quarters – with SOFR beginning to equal and surpass LIBOR in Q1’23. Over the past 9 months, SOFR-pegged loans have gone from 28.5% of total floating loans to 75% for the loans in the underlying sample portfolios.

LIBOR Declines While SOFR Grows (sample of 13 BDCs)

Count of Floating-Rate Investments – Sample of 13 BDCs over the past 4 quarters

| Base Rate | Q3’22 | Q4’22 | Q1’23 | Q2’23 |

|---|---|---|---|---|

| LIBOR-based floaters | 1,232 | 1,117 | 986 | 454 |

| Non-LIBOR-based floaters | 550 | 769 | 1,005 | 1,555 |

| Total Floaters | 1,782 | 1,886 | 1,991 | 2,009 |

| LIBOR as a % of Total Floaters | 69.1% | 59.2% | 49.5% | 22.6% |

| SOFR-based floaters | 507 | 715 | 942 | 1507 |

| SOFR as a % of Non-LIBOR | 92.2% | 93.0% | 93.7% | 96.9% |

| SOFR as % of Total Floaters | 28.5% | 37.9% | 47.3% | 75.0% |

We’ve currently discussed the recent increased migration efforts that led to a successful migration away from LIBOR, but does that mean all loans refer to an alternative rate? Not quite. Currently, in the same BDC sample as of the end of 2023Q2, 75% of loans reference SOFR.

With regards to the leveraged loans and the CLO market, the results are similar, as 76% of loans reference SOFR (as of August), per LSTA.[4] The reason why these numbers are not 100% is due to contracts that were opened prior to the June 30,2023 deadline that still refer to a LIBOR reference rate.

Since most contracts are 3-months, we should expect to see a considerable amount of loans automatically migrating to SOFR (via the LIBOR act or through the triggering of an amendment). We will continue to track this migration as it nears completion.

Overall, it appears that the transition has gone quite smoothly, thanks to years of thoughtful preparation. Loans that are currently tied to LIBOR will eventually point to an alternative rate once the contracts next renew – post June 30.

The AARC, which was tasked to determine the proper alternative rates to transition to, will slowly[5] wind down its work, emphasizing that the SOFR should be deemed the best option as the alternative rate given its robust tie to the transaction-heavy treasury market.

Going forward, we will keep readers updated on the status of the remaining loans that still reference LIBOR and hope to look past the migration with a greater sense of triumph.

Sample of BDCs in our study:

| Audax Credit BDC Inc. |

|---|

| BlackRock Private Credit Fund |

| BlackRock TCP Capital Corp. |

| Capital Southwest Corp. |

| CION Investment Corp. |

| Fidus Investment Corp. |

| Great Elm Capital Corp. |

| Oaktree Strategic Credit Fund |

| Oaktree Specialty Lending Corp |

| Blue Owl Capital Corp. |

| Oxford Square Capital Corp. |

| PennantPark Floating Rate Capital Ltd. |

| Prospect Capital Corp. |

[1] Alternative Reference Rates Committee

[2] https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2023/ARRC-Readout-July-31-2023-Meeting

[3] https://www.lsta.org/news-resources/libor-transition-one-two-last-hurrahs/

[4] https://www.lsta.org/news-resources/libor-cessation-t1-month/

[5] https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2023/ARRC-Readout-July-31-2023-Meeting

News

Steve Krieger explores emerging managers’ challenges when developing portfolio operations teams from scratch while simultaneously fundraising and sourcing deals.

Steve Krieger

Head of Key Client Partnerships

We understand that for first-time funds and emerging managers in particular, developing a portfolio operations team from scratch, while simultaneously fundraising, sourcing deals and facing into macro-economic headwinds, is a big challenge.

The latest ‘Operational Excellence’ report from PEI explores how businesses are meeting this challenge; including hiring experienced value-creation professionals, innovating around existing value-creation levers and using new technologies and finally working with the right partners to access specialist functional or industry expertise.

Steve Krieger, our Head of Key Client Partnerships, delves into the importance of quality over quantity and how working with the right partners can create a truly value-creating operations team from day one.

He contends that:

Contact Steve to hear more about our operations expertise and you can access the broader PEI “Operational Excellence” report here.

Please select a contact

Conference

We’re proudly sponsoring the 9th International Funds Summit & Expo in Cyprus on October 23 and 24.

The summit brings together investment fund professionals from around the world to discuss the evolving regulatory and increasingly competitive landscape in the global asset management sector and much more.

On Day 2, Evdokia will moderate the panel discussion “The Future of Funds Administration”, where experts will explore how the future of fund administration is posing unique regulatory challenges, especially in smaller jurisdictions.

Meet our team at our Alter Domus booth and discover how our solutions can meet your needs.

Cyprus

Country Executive Cyprus

Cyprus

Head of Operations at Alter Domus Cyprus

No related content found.

Conference

Alter Domus is proudly sponsoring LSTA’s Annual Conference in New York on October 12. Connect with our team at the conference to learn how evolving risk assessments and new technologies are reshaping loan markets. Our attendees at the event include:

Interested in discovering how our expertise and systems can bring clarity to your loan portfolio? Come and meet us at out booth!

United States

Global Sector Head, Debt Capital Markets

United States

Head of Loan Trade Settlement, North America

United States

Managing Director, Sales, North America

Luxembourg

Product Strategy Director

No related content found.

News

Speaking with Preqin as part of their Services Providers Report, Jessica Mead, Regional Executive, North America offers her perspective on the changing ways firms are looking to work with their administrators

Jessica Mead

Regional Executive, North America

Your operating model and managed services provider need to be able to accommodate your future growth plans. If you are considering moving into new jurisdictions, asset classes or strategies, they need to be able to flex accordingly to support that next step for your company. Crucially in today’s data-driven environment, you also want to think about your data and technology needs. Investors are demanding real-time access to information and transparency. Do you want to take on the cost and responsibility of building and maintaining the capability to provide that in-house? Many asset managers are engaged in M&A activity, which is a logical moment for a fundamental rethink of your operating model.

The need to access data is driving change – for the better in our view. We’re moving away from a commoditized and transactional type of model towards operationally integrated partnerships, where there’s transparency and access to data in real-time. We’re also seeing some consolidation and rationalization of partnerships. Where perhaps a manager might have had multiple fund administrator partnerships in the past, now they might have one or two deeply embedded partnerships that can cover all the jurisdictional and sector specialisms they need globally.

Essentially, co-sourcing is an operating model where the manager maintains an in-house data and technology stack that their administrator has access to and can create and modify primary data elements. It’s a hybrid model between fully outsourced and fully insourced. The benefit it offers managers is that it allows total control and ownership of their data and real-time access to it, while tapping into the asset class and systems specialists, and talent acquisition capabilities of a fund administrator, all while reducing manager level overheads.

That partly depends on whether, as a manger, you have the scale and appetite to reinvest in your own technology and in-house operations or not. There are considerable advantages to partnering with a provider who constantly upgrades their technology platforms and can provide a long-term career path to valuable internal resources. There are also the economies of scale and best practices that a global administrator can offer, without being distracted by the challenges of maintaining a back office. We’ve seen great success for both clients and personnel as we’ve created a playbook to successfully assist with these types of full lift-out transitions.

Ultimately a good administrator is focused on white-glove levels of service and forming a deep partnership with their clients, which will include customizable solutions and specific asset-class expertise that meets specific needs. An administrator should be viewed as a critical member of the team, who when leveraged correctly delivers significant value-add to portfolio, risk management, and investor teams. Critically, you need to have confidence that they are technologically innovative, as well as culturally a good fit for your organization.

This article was originally published in Preqin's Service Provider Report.

United States

Global Head, Private Credit

News

Private equity firms looking to launch their first debt fund are in for a series of challenges if they don’t have the operational infrastructure to administer it, warns Greg Myers

Greg Myers

Global Sector Head, Debt Capital Markets

First, there’s the legacy effects of a long-term zero interest rate environment, and the proliferation of dividend distributions from a lot of LBOs, especially from the sponsor finance community, or private credit funds. They were done when rates were low – one floor or two for reference rates – and now it’s ticking up to the five range.

And with these legacy spreads and the current reference rates, some of these companies can’t afford that debt service as part of their operating model. That’s starting to trigger a lot of the EBITDA covenants within their underlying credit and lending agreements.

So we’ve seen a lot of our traditional private credit lenders and opportunistic managers launching special situations and credit opportunity funds, where they can step in, restructure the debt, and maybe put it on non-accrual or non-cash pay for a period of time to work these deals out. There was a bump in these funds being formed at the beginning of covid, with the assumption the pandemic would create a boom in distressed situations for the then pending economic distress.

However, due to all the government stimulus, that boom was delayed. But with the prolonged increase in rates, even with the continued economic performance, a lot of these managers are expecting that boom to commence. There are also situations like the collapse of Silicon Valley Bank that suggests there will be interesting portfolios coming to market, priced to be offloaded quickly and able to be worked out at significant returns to investors.

Traditional asset-based lending is typically lending where there’s a lag time between when corporate borrowers need to finance their commercial operations and bridge the period of time that their customers are paying them for the product that’s been delivered.

Up until recently, that’s been the world of a money center bank, or a super-regional money center bank that have these facilities where they will make those loans, monitor those loans and pledged collateral, and keep that relationship with a borrower. But given the ultra-sensitivity of those super-regional bank market events, those are really good loans to shed because they have high market value, without the bank to reserve against them.

So we’ve seen a number of those portfolios come to market where it’s private capital that will take on those asset based loan (ABL facilities) on behalf of the borrowers at a pretty good rate from the original bank lender.

And then there’s the role of the traditional investment bank on providing portfolio leverage, which we now see large insurers and actual funds coming in to replace them, despite all the compliance issues and strict rules around what’s applicable, what’s admissible, and substitution rights if a particular asset goes wrong. This is now becoming the realm of large insurers, since they have a more permanent capital base, one that isn’t based on deposits.

We’ve had a few clients entering into lending or refinancing arrangements, and they really liked the term loan and the borrower. The borrower then brings up the fact that they also have this ABL and would like to have the same provider for both.

So the manager decided to meet that market need, and as a result, we ended up exploring what we could do to service them, and licensed a product dedicated to the ABL space that provides transparency to the lender, the borrower and us though the operating infrastructure.

When I speak with PE managers that are used to underwriting and investing in a portfolio company and valuing their portfolio once every quarter, they’re in for a very different level of activity in the credit space. The same underwriting process and the ongoing valuations occur, but additionally the bank debt pays at a minimum quarterly, and the rate resets typically quarterly. There are amortisation payments. Loans are typically originating below par. So they’ve got non-cash income that they need to recognise.

These deals get amended constantly, so there could be different compliance rules under the credit agreements. Furthermore, the maturities get extended, the size of the deal could move up and down, and all this requires a great deal of monitoring of the underlying borrower. And they need a system that will address and support all those things.

They have to decide who will be the administrative agent on the credit, whether it’s done internally, or outsourced completely.

Then there’s SEC oversight around the custody of investor assets. How are they going to build an infrastructure where they’re not co-mingling investor monies across multiple funds or different borrowers and everything else required to withstand the scrutiny of the SEC? And that’s just on the legal and operational side of things.

As a result, our clients invest a lot of resources on attorneys, compliance experts and our services because we have the appropriate systems for the agent components, the loan administration, which is tracking and ticking and tying all the cashflows, positions, rate resets, amortisation schedules, and then ultimately the fund accounting and investor reporting. Because a direct result of this growth in private credit is there is a dearth of people that know how to do credit accounting because it is very different than PE, or fund-of-funds accounting.

This ends up producing a massive amount of data to monitor and manage. The front office wants credit monitoring. The middle office needs to monitor the compliance with the credit agreements. And then the back office needs the data to produce the reports and everything else. There are big ticket systems available that cost millions to implement or off-the-shelf systems that support various functions for credit managers.

There are much lower cost solutions for data warehouses where they can build report writing software on top of the warehouse – these become a kind of integral hub for the spokes that go out to address reporting requirements. And then there are other inexpensive add-ons that can offer portfolio view technology as well.

Most clients want that data in-house, but it’s a daunting task to build internally. This is why we’re confident that outsourcing will continue to offer a compelling value proposition for the GPs looking to make the most of this particular moment in the credit markets.

This article was originally published in PDI's US Report.

United States

Global Sector Head, Debt Capital Markets