Partner with Alter Domus to make every secondary count

Secondaries are increasingly proving to be vital financial vehicles for both asset managers and asset owners, especially during times of economic uncertainty.

So whether you’re an LP seeking to generate liquidity, or a GP looking setting up continuation funds and reduce the administrative burden, Alter Domus are ready to help our clients make every secondary count.

We’ve combined deeply experienced and dedicated secondaries teams with the latest 3rd generation fund administration technology to help our clients capitalize on their opportunity and deal with any complexity or volume.

Our vertically integrated model enables us provide support and bespoke solutions for the entire value chain and across our extensive range of services, from depositary to AIFM and accounting. Contact us here to discuss your secondaries strategies with our team.

Capitalizing on the secondaries opportunity

Secondary transactions rebounded in 2023 to the second highest on record. With 2024 set to continue this trend, it’s vital that GPs and LPs select the right administrator for their funds. Watch the video to see what differentiates Alter Domus as a partner for your secondaries strategies.

5 trends shaping private markets secondaries in 2024

The data shows that amid the macro-economic headwinds that buffeted private markets in 2023, the secondaries space managed to deliver year-on-year growth across most key metrics. And, after a bumper year of fundraising, 2024 looks set for secondaries growth. In our latest article we highlight 5 key themes for the year ahead.

For private equity, necessity is the mother of invention

In this interview from Private Equity International’s Debt Finance issue, Tim Toska, Group Sector Head of Private Equity, outlines how ingenuity is helping LPs overcome liquidity issues in a sluggish market. This includes using GP-led secondaries to release liquidity from long-held assets and turning to NAV financing.

Keeping the lifeblood of capital flowing: the undervalued role of the secondaries market

Amid the rise of alternative assets over the last two decades, the number of investment opportunities available to both limited partners and general partners has grown. One such vehicle – the secondaries market – is attracting increasing amounts of attention and fundraising.

Tim Toska, Global Sector Head of Private Equity at Alter Domus, and Brian Mooney, Managing Director and Co-Head of GP-led Secondaries at Portfolio Advisors discuss how GP-led deals are emerging as a strong exit option, the impact of supply/demand dynamics on pricing, the importance of transparency and preparation for sponsors, and the role of technology and data analytics in the process.

Goldman Sachs $15bn to buy stakes in private equity funds

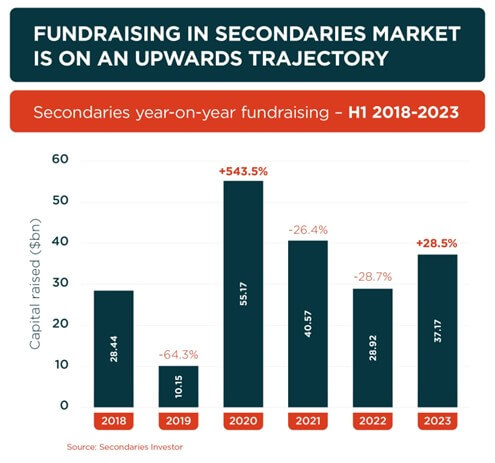

The Financial Times reported that Goldman Sachs will be investing large parts of a new $15bn fund in the PE secondaries market piqued our interest. Secondaries really do appear to be on an upward trajectory right now.

What are some of the most practical applications of artificial intelligence in the funds industry? Get the answer to this question and more by joining James McEvoy and Conor O’Callaghan on 30 November as they attend the Irish Funds UK Symposium in London. The conference will also cover the ELTIF 2.0 and its implications, as well as the UK Overseas Funds Regime.

Keen to find out how Alter Domus is using AI to augment fund servicing, and how we can support your strategy amid ongoing regulatory change? Get in touch with our team today!

Discover how the latest ELTIF regulations are poised to reshape Luxembourg’s private markets by joining Alan Dundon, Dirk Sanden, and Sebastien Collard at the ALFI’s Private Assets Conference in Luxembourg from November 28-29. The event will also delve into recent advancements in private asset servicing and tech solutions for fund reporting.

Engage with our team at the conference to explore how to future-proof your fund and leverage emerging market opportunities with our tailored solutions.

Key contacts

Alan Dundon

Luxembourg

Director, Sales & Relationship Management

Sébastien Collard

Luxembourg

Co-Head of Relationship Management Europe

Dirk Sanden

Luxembourg

Director, Sales & Relationship Management

More events

No related content found.

Conference

Digital Challenges in AI and Automation

When

7 November

Organizer

EY & Pega

Venue

EY Luxembourg 35E Av. John F. Kennedy 1855 Luxembourg

How are firms like Alter Domus putting cutting-edge AI automaton to work? Find out at EY and Pega’s joint event at EY Luxembourg on 7 November. Alter Domus’ Danilo McGarry will be speaking about AI, lessons learned, challenges, and his experience with AI at Alter Domus in a lively panel discussion.

If you’re keen to hear more about state of the art in automation and the power of AI from a panel of leading experts, be sure to register for the hybrid event, which is also being held online.

Key contacts

Danilo McGarry

United Kingdom

Head of Digital Transformation

More events

No related content found.

News

Alter Domus appoints Michael Janiszewski as Chief Operating Officer and Group Executive Board Member

Alter Domus, a leading provider of tech-enabled fund administration, private debt, and corporate services for the alternative investment industry, has appointed Michael Janiszewski as its new Chief Operating Officer.

In this role, Michael will report to Doug Hart, Alter Domus Chief Executive Officer, and will also join Alter Domus’ Group Executive Board.

Michael brings significant executive experience in leading the operations of global organizations. His successful 20+ year track record spans business & strategy development, business transformation, operational excellence, and digital innovation. Mike joins Alter Domus from BNY Mellon’s Securities Services and Digital business, where he served as Chief Operating Officer.

Alter Domus CEO Doug Hart said: “We’re excited to combine Michael’s expansive background with Alter Domus’ industry leading private markets services platform. Our aligned vision of the future of alternative investment operations will accelerate the Company’s client experience initiatives day-one.”

Following his appointment, Michael Janiszewski, Alter Domus Chief Operating Officer, said: “I am proud to join Alter Domus and am excited by the bright future ahead of our organization. I am looking forward to partnering with the talented and experienced group of executive leaders on our Group Executive Board, as well as the talented professionals across Alter Domus.”

Michael holds a BA in Electrical Engineering and a Certificate in Applications of Computing from Princeton University, and an MBA in Finance, Accounting, Strategy, and Entrepreneurship from the University of Chicago Booth School of Business.

Liquidity constraints are behind a great deal of innovation in the debt finance market, says Tim Toska, Global Sector Head for Private Equity at Alter Domus

Tim Toska

Global Sector Head, Private Equity

What challenges are private equity managers currently facing around liquidity and funding?

The difficult dealmaking environment is really steering all the liquidity issues that managers are facing right now. The fact that dealmaking has significantly slowed down over the last 12 to 18 months – and the same is true for fundraising in the last six to nine months – is creating a bit of a challenge.

We still see managers observing the availability of follow-on investments or quality assets; the economy hasn’t stopped and there are plenty of opportunities. However, LPs have slowed down their commitments because of a lack of liquidity, and that has created constraints. Institutional investors still believe in private equity, but they have been impacted by both a slowdown in distributions and the denominator effect. As a consequence, their own liquidity has become more correlated with other asset classes – this creates challenges for them.

For a long time, constrained private equity managers relied on subscription line financing, but in the wake of the regional banking crisis in the US at the start of this year there are now fewer lenders and slightly higher rates in that space. LPs are questioning the use of those facilities, which were always a bit of a short-term solution.

What financing options are PE funds embracing?

We have seen a growing number of clients looking to GP-led secondaries as an interesting solution to the current challenges. This is taking place at both ends of the spectrum: GP-leds are being used as a means of providing liquidity to LPs, as well as a route to new funding for some of the assets in their portfolios.

In most of these deals, we are talking about high-quality assets that might have been in the portfolio for a while, have been performing well, and the GP believes there is more value to be extracted. A GP-led secondaries deal offers an opportunity to release liquidity to LPs that have been in the fund for some time so that they can continue to invest and re-up into the next fund.

In terms of other financing options, we still see sub lines being used a lot, while NAV financing solutions are also picking up steam. Those tools have been out there for many years, but they are receiving increased attention in the current climate. However, they are not without complexity.

From a lender perspective, the NAV financing market has started to evolve, with a wave of key players leaving legacy banks to join asset managers that are creating dedicated NAV financing funds. Those individuals really understand the asset class and are able to increase that velocity of distributions back to LPs so they can re-up with existing managers.

The other issue here is the slowdown in exits, with the tide having shifted significantly in the last three or four years. LPs have turned their focus from IRRs to distributions, and while they understand that it is not always in the manager’s control to decide when to sell, at least with NAV financing they can achieve some predictability of cashflow. What’s more, this is not necessarily just for right now: we don’t see NAV financing going away, but rather becoming a much more commonly used liquidity tool for managers.

How would you describe the current health of the PE secondaries space?

The PE secondaries space is very healthy, both for GP-led and LP-led deals. Last year, GP-leds considerably outpaced LP-led transactions. That had more to do with the exit markets as managers didn’t want to be forced to sell when rolling LPs could see more runway. A lot of LPs chose to go into those deals because they weren’t experiencing quite the same liquidity crunch as we saw going into 2023. Today, GP-leds are still getting done for high-quality assets.

On the other side of the equation, LP-led deals have picked up in 2023. Those deals are not trading at major discounts – they are right around NAV, or maybe at 80 or 90 percent – and there is a healthy volume of activity.

Immediately after the global financial crisis, we saw LP-leds trading at 20 or 30 cents to the dollar, and at that point we started to see the use of deferrals. Then portfolios started to mark to par, and sub lines came back into use.

Today, we are seeing another pick up in the use of deferrals, where a seller and buyer agree a price and then agree to defer some of that purchase price out a few years. Maybe a buyer is willing to pay closer to par on the valuation of the portfolio in that instance and the seller is willing to wait in exchange for a higher purchase price. For some selling LPs, the result is enough liquidity to bridge the gap they are facing thanks to a lack of distributions. It doesn’t work for everyone, however, with some sellers preferring to accept a purchase price at 80 percent of NAV for cash upfront.

What challenges do managers face when tapping the GP-led market?

One of the biggest challenges is understanding and meeting the expectations of LPs. Most GPs are rolling more carry into a continuation vehicle and taking a bigger stake, because there is much more focus on alignment in these deals. LPs want to see managers putting more skin in the game.

Another issue is the SEC is putting a lot more regulatory focus on these deals, introducing a regulatory process around third-party valuations, for example. And, of course, the economics will be a little more friendly to the LP base in a continuation vehicle, which managers can find challenging.

Finally, there are the issues associated with convincing LPs that this is the right decision, which requires managers to be ready with the data on the portfolio company and with a plan of where they see things going. The transparency is something that most managers have caught up with, but the volume and frequency of data required from the portfolio is nevertheless a challenge.

The good news is that there is capital available for these transactions and there are LPs that want to cash out, which means there is appetite on both sides.

What new trends do you expect to feature in the debt finance market over the next year or two?

We are seeing growing sophistication in the NAV financing market, shifting from a focus on lending from banks towards other funders with more liquidity. No doubt over time we will see more use cases, and an industry that started out as pretty vanilla will attract more expert professionals.

We are also seeing a lot of clients struggling to achieve anything meaningful with capital call facilities because the banks are hesitant. Over time, we expect less reliance among PE managers on traditional bank lenders and more use of the tools being created by a new wave of asset managers who are combining private equity and credit market expertise.

How can firms leverage the advantages of virtual and in-person meetings for better client outcomes? Find out on 9 November during the Financial Times webinar: Optimising Client Interactions in the Finance Sector.

The event is focused on the virtual and in-person interactions within the financial sector, and aims to highlight the respective pros and cons of digital engagement in client relationships and workplace productivity. Alter Domus’ Danilo McGarry, with his deep expertise in digital transformation and data, will be sharing his insights on how digitalization is changing how the industry interacts with its clients and stakeholders. Don’t miss it!

From 8-9 November, our very own Angela Summonte will be attending ALFI’s Roadshow to Switzerland, taking place in both Zurich and Geneva. The event will cover key subjects concerning both the Luxembourg and Swiss fund communities, including hot topics like AIFMD and UCITSD. Be sure to contact Angela in advance if you’ll also be attending!

Key contacts

Angela Summonte

Luxembourg

Group Director, Key Accounts

More events

No related content found.

News

5 things you can do now to prepare for the new SEC regulations

When the SEC voted on August 23rd this year to adopt and finalize new rules and amendments under the Investment Advisers Act of 1940 (the “Advisers Act”), the full implications for private fund managers crystalized. With these wide-ranging measures starting to come into effect any day now, the timeline to comply means you cannot afford to be complacent.

Here are some key areas of the Final Rules that each private fund advisor will be responsible for, regardless of whether they are registered with the SEC or not:

Quarterly Statement Rule 211(h)(1)-2

Audit Rule 206(4)-10

Compliance Rule 206(4)-7(b)

Adviser-Led Secondaries Rule 211(h)(2)-1

Preferential Treatment Rule 211(h)(2)-2

Restricted Activities Rule 211(h)(2)-3

With these rules in mind, here are five key things private fund advisors should be considering and preparing for now:

Become familiar with the required updates needed for private fund quarterly and annual audit reporting including required issuance dates, governing documents, policies, and procedures.

Consider any grandfathering clauses that may affect your requirements under the Restricted Activities Rule and Preferential Treatment Rule with respect to already existing agreements.

Start to work through how to incorporate additional transparency around private fund fees and expenses, including calculations and cross-reference to organizational documents, performance, and potential conflicts of interest.

Review preferential treatments currently in place for certain investors in a private fund or a similar pool of assets and become familiar with the disclosure requirements, or cessation, of the same, for current and prospective investors.

Assess the adoption dates for the new rules.

No one-size-fits-all approach

The nature and complexity of these reforms mean that firms need to take a proactive and individual approach to their compliance – there is no cookie-cutter solution.

With that in mind, here at Alter Domus, we are cognizant of the amount time and collaboration our clients will require across their own organization and across third party service providers, like ourselves.

The new requirements will have significant impacts on the timing and level of detail and disclosures required for quarterly and annual financial reporting, and as such, please get in touch with us to discuss our plans for preparation. Contact us below.

We are proudly sponsoring Private Funds CFO Network’s Europe Forum in London from November 14th to 15th. Andy Clark and Catherine Kavanagh from our team will be there, so please make sure to say hello. And don’t miss Patrick McCullagh moderating a debate discussing the pros and cons of outsourcing on November 14th at 4:30pm. The panel will delve into the aspects of operations, reporting, and workflows.

Get in touch today to connect with the team at the forum.